Malaysia’s e-invoicing mandate has reshaped how businesses handle their billing and tax compliance obligations. For companies that process hundreds or even thousands of small transactions every day, think retail outlets, petrol stations, food and beverage chains, or e-commerce sellers submitting an individual e-invoice for every single sale is simply not practical. That is precisely where the consolidated e-invoice framework steps in, offering a compliant, streamlined alternative that keeps administrative burdens manageable while still satisfying the Inland Revenue Board of Malaysia’s (LHDN/IRBM) reporting requirements.

Whether you are a small business owner trying to understand your obligations or a finance manager overseeing multi-branch operations, getting to grips with how consolidated e-invoicing works is essential.

This guide covers everything you need to know from definitions and eligibility conditions to submission timelines, required data fields, sector-specific restrictions, and how modern ERP platforms can automate the entire process. If you are still building your foundational understanding of Malaysia’s broader e-invoice rollout, our detailed overview of e-invoicing in Malaysia is a great place to start before diving deeper here.

Key Takeaways

|

What Is a Consolidated E-Invoice?

A consolidated e-invoice is a single digital report that bundles a month’s worth of small sales like coffee or groceries into one submission for the tax office (IRBM). It’s important to note that this does not replace the regular receipts you give to customers at the counter. Instead, it acts as a behind-the-scenes tool that lets the government track total revenue without needing to identify every individual buyer.

This process is legally backed by IRBM guidelines to keep high-volume businesses like retail and e-commerce running smoothly. The tax authorities recognize that creating an individual e-invoice for every tiny transaction would be an operational nightmare. By using this method, you stay compliant while keeping your daily business operations fast and efficient.

Consolidated E-Invoice vs Individual E-Invoice, What’s the Difference?

Understanding how consolidated e-invoices differ from individual e-invoices is critical before deciding which route to take. The table below summarises the key distinctions:

| Aspect | Individual E-Invoice | Consolidated E-Invoice |

| Buyer identification | Named buyer with TIN and registration details | Buyer details generally not included (General Public) |

| Submission frequency | Per transaction, in real time or near real time | Once per month, covering the prior calendar month |

| Submission deadline | Within 72 hours of the transaction | Within 7 days after the end of the calendar month |

| Suitable for | B2B and B2G transactions; high-value B2C | B2C transactions where buyers do not request an individual e-invoice |

| Transaction value threshold | Mandatory for transactions ≥ RM10,000 from 1 Jan 2026 | Typically used for lower-value, high-frequency transactions |

| Buyer consent/request | Buyer may specifically request for record-keeping or tax deduction purposes | Issued only when buyer does not request an individual e-invoice |

In practical terms, if a registered business buys goods from you for RM50,000 and needs the e-invoice to claim input tax credits or expense deductions, you must issue an individual e-invoice. If a walk-in retail customer buys RM45 worth of merchandise and has no need for a formal e-invoice, that sale can flow into your monthly consolidated e-invoice instead.

When Should You Issue a Consolidated E-Invoice?

Not every business and not every transaction qualifies for the consolidated e-invoice route. IRBM has set out specific conditions that determine when a supplier is permitted and in some cases required to use this method. Understanding the eligibility framework will help you avoid compliance pitfalls and make the right call at the point of sale.

B2C Transactions (Buyer Does Not Require an E-Invoice)

In these situations, the supplier issues a normal receipt at the point of sale which satisfies the buyer’s immediate needs and then captures that transaction data internally. At the end of the month, all such unattributed receipts are aggregated and submitted as a single consolidated e-invoice to IRBM. This approach works well for retailers, petrol stations, fast-food chains, pharmacies, online marketplaces serving end consumers, taxi and ride-hailing operators, and many other consumer-facing businesses.

It is worth noting that if a B2C buyer specifically requests an individual e-invoice perhaps because they are self-employed and want to claim a business expense deduction,the supplier is obligated to issue one upon request. Once an individual e-invoice has been issued for a transaction, that same transaction cannot also be included in the consolidated e-invoice for the month.

During the Relaxation Period (Grace Period)

The IRBM’s phased e-invoicing rollout includes a grace period that allows businesses to issue standard receipts without the need for immediate, real-time validation. During this time, companies remain compliant by submitting monthly consolidated e-invoices to report all transactions at an aggregate level.

This transitional approach is especially vital for smaller businesses entering the mandate in later phases. It provides a practical bridge, enabling them to meet LHDN reporting obligations while maintaining their existing billing infrastructure and buyer-facing processes largely unchanged.

It is important for businesses to track when their applicable relaxation period ends, as the requirements tighten considerably once the grace period lapses. Businesses that rely on consolidated e-invoices as a temporary workaround need to have a clear migration plan toward full real-time e-invoicing where applicable.

Understanding the broader tax obligations including how the expanded tax scope impacts your invoicing duties can help you plan more effectively

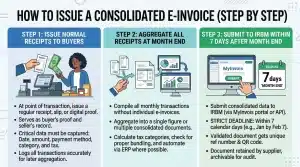

How to Issue a Consolidated E-Invoice (Step by Step)

The practical process of issuing a consolidated e-invoice involves three clear stages. While the underlying logic is straightforward, executing it correctly especially at scale requires disciplined data capture throughout the month. Here is a step-by-step breakdown.

Step 1 — Issue a Normal Receipt to the Buyer

At the point of every transaction, the seller continues to issue a regular receipt, cash register slip, or digital proof of payment to the buyer. This receipt does not need to carry any LHDN QR code or validation reference. It simply serves as the buyer’s proof of purchase and the seller’s transaction record for internal accounting purposes.

What is critical at this stage is that the business captures sufficient transaction data internally date, amount, payment method, product or service category, and any applicable tax so that these records can be accurately aggregated later. A business using a point-of-sale (POS) system should ensure that the system is configured to log all transactions in a format that can be exported and processed at month end. Gaps in transaction records at this stage will create headaches during the aggregation and submission steps.

Step 2 — Aggregate All Receipts at Month End

At the close of each calendar month, the business compiles all transactions that were issued normal receipts during that month, specifically those where the buyer did not request or receive an individual e-invoice. These are aggregated into a single consolidated figure or, depending on the business structure, into multiple consolidated e-invoices (for example, one per branch or one per business activity type).

The aggregation step requires the business to calculate totals for each relevant tax category (taxable, exempt, zero-rated, and so on), confirm that no individual transaction above the relevant threshold is being improperly bundled into the consolidated document, and prepare the data in a format compatible with the MyInvois portal. Businesses with sophisticated ERP systems can often automate this step, pulling transaction data directly from their POS or sales management modules and generating the consolidated e-invoice data set without manual intervention.

Step 3 — Submit to LHDN Within 7 Days After Month End

Once the consolidated data has been prepared, the supplier must submit the consolidated e-invoice to IRBM through the MyInvois portal either directly via the web interface or through an integrated API connection. The submission deadline is strictly within 7 calendar days after the end of the relevant calendar month. For example, all consolidated e-invoices covering January transactions must be submitted by February 7.

Upon submission, MyInvois will validate the document and, if compliant, return a validated e-invoice with a unique document reference number and a QR code. Unlike individual e-invoices, the validated consolidated e-invoice is not typically shared with the buyers it is a tax reporting document retained by the supplier and accessible by IRBM. The supplier should archive the validated consolidated e-invoice along with the underlying transaction records for audit purposes.

Required Details in a Consolidated E-Invoice

A consolidated e-invoice must contain specific data fields to be accepted by the MyInvois system. Missing or incorrect information will result in rejection, which means the supplier must correct and resubmit before the deadline. Below is a breakdown of the key data elements required.

Buyer Details

One of the defining characteristics of a consolidated e-invoice is that it does not carry the specific details of each individual buyer whose transaction is included. Instead, the buyer field is populated with generic placeholder information indicating that the document covers transactions made by members of the general public or unidentified buyers.

IRBM’s guidelines specify that the following placeholder values should be used in the buyer identification fields:

- Buyer’s Name: General Public (or equivalent)

- Buyer’s TIN: EI00000000010 (the standard placeholder TIN for consolidated e-invoices)

- Buyer’s Registration/Identification Number: Not applicable or a specified placeholder

- Buyer’s Address: Not applicable or a standardised placeholder

This approach allows IRBM to process the document as a valid e-invoice while acknowledging that the underlying transactions involve anonymous or unidentified retail buyers. It also protects consumer privacy, as individual buyers’ personal details are not captured or transmitted to the tax authority through this mechanism.

Product/Service Description

Consolidated e-invoices do not require a line-by-line itemization of every product sold. Instead, suppliers provide a general description of their business activity such as “Food and beverage services” along with the relevant IRBM classification codes. This approach simplifies reporting while clearly identifying the nature of the transactions for tax purposes.

Each line item should represent a logical grouping of similar transactions, with the quantity field typically reflecting the total number of receipts. The unit price and line totals must show the aggregated value for that group, while all applicable taxes and levies are correctly calculated and declared per category to maintain compliance.

Aggregation Methods

IRBM accepts different aggregation approaches depending on the nature of the business. The two primary methods are:

- Single-line aggregation: All transactions for the month are rolled up into a single line item with one total amount. This is the simplest approach and works well for businesses with homogeneous transaction types.

- Multi-line aggregation by tax category: Transactions are grouped by tax treatment for example, standard-rated, zero-rated, and exempt and presented as separate line items with individual sub-totals. This is more common for businesses selling a mix of taxable and non-taxable goods or services.

While the IRBM allows flexibility in segmenting consolidated e-invoices by product category or business unit, the total declared value must strictly match the summary of all qualifying receipts issued during the month. Maintaining a consistent aggregation methodology is vital for internal audits, as clearly documented records are essential should any discrepancies arise. Ultimately, this is where robust tax invoice management practices ensure a strong and efficient compliance posture.

Restrictions and Limitations

While consolidated e-invoicing is a valuable compliance tool, it does not apply universally. IRBM has imposed specific restrictions on its use both in terms of transaction value thresholds and industry sectors. Businesses that incorrectly classify transactions under the consolidated route when individual e-invoices are required risk penalties and potential audit exposure.

Transactions Above RM10,000 Must Have Individual E-Invoices (From 1 Jan 2026)

Effective 1 January 2026, B2C transactions exceeding RM10,000 must be issued as individual e-invoices rather than being consolidated at month-end. This threshold ensures specific buyer attribution for high-value items like luxury goods or major services, reflecting their significant tax importance to the IRBM.

To comply, businesses must automate POS filters to flag these high-value sales and trigger the correct individual workflow. This also requires training front-line staff to smoothly collect buyer TIN or identification details, as manual tracking in high-volume environments is highly prone to errors.

Sectors Prohibited from Issuing Consolidated E-Invoices

As of September 2026, the IRBM (LHDN) has ruled that certain businesses cannot use “bulk” or consolidated e-invoices. This means if you are in one of these industries, you must issue a separate, individual e-invoice for every single sale, even if the customer doesn’t ask for one.

The main sectors affected by this rule include:

-

Electricity & Telecommunications: Every bill must be an individual e-invoice.

-

Banks & Insurance: Financial institutions under BNM have their own strict individual rules.

-

Aviation, Healthcare, & Education: These industries must follow special guidelines that prioritize individual reporting.

Because there is no grace period for these specific industries, you must have your systems ready for real-time reporting immediately. It is important to stay updated, as the government may add more sectors to this list as the e-invoicing framework evolves.

MyInvois System Technical Limits

Beyond the eligibility rules, the MyInvois portal has specific technical limits that businesses must manage. Large retailers with thousands of transactions may need to split their monthly data into multiple documents to avoid hitting file size limits. Additionally, all automated submissions must use JSON or XML formats that match the latest government specifications.

To ensure a successful submission, the system runs automatic checks against official tax and industry codes. If your data uses an outdated code, the entire document will be rejected. Here are the key technical points to remember:

-

Split Large Files: High-volume businesses must monitor file size limits to avoid rejection.

-

Format Matters: Only JSON and XML are supported for automated API submissions.

-

7-Day Correction Window: Rejections must be fixed and resubmitted within one week.

-

Ongoing Updates: Your system must stay updated with the latest IRBM software versions

How Smart Systems Help Manage Consolidated E-Invoices

For businesses managing high sales volumes or multiple branches, manual processes are not only unsustainable but also prone to costly errors. Transitioning to integrated business management software is the most effective way to ensure accuracy and add measurable value to your compliance workflow.

ERP auto-aggregation replaces manual POS data sorting with real-time transaction tracking. The system automatically tags tax categories, flags transactions over RM10,000 and generates month-end reports with a single click. This streamlines compliance while eliminating the transcription errors inherent in manual processes.

MyInvois API integration automates submissions directly to the IRBM portal, eliminating the need for manual file formatting or uploads. The system handles real-time data exchange and stores validated reference numbers for a complete audit trail. Therefore, choosing among the best e-invoicing software solutions available in Malaysia with genuine MyInvois API certification is a critical factor in your vendor selection process.

Multi-branch consolidation distinguishes enterprise-grade ERPs from basic tools, especially for large retail chains. These systems can segregate transaction data from dozens of outlets to generate either branch-specific or centralized national e-invoices under a single parent TIN. This flexibility allows businesses to structure their monthly submissions in full alignment with IRBM guidance and their own operational needs.

By transforming mandatory reporting into actionable operational intelligence, a well-structured e-invoicing process provides a competitive edge that businesses can only secure by proactively mapping their technology against IRBM guidelines today to prevent the high costs of emergency upgrades under compliance pressure.

Conclusion

The consolidated e-invoice framework represents one of the most practically significant concessions IRBM has built into Malaysia’s e-invoicing mandate. For businesses operating in high-volume, consumer-facing environments, it provides a workable compliance pathway that acknowledges the operational reality of retail and service industries without compromising the tax authority’s need for visibility over transaction revenues.

To summarise the key points every business needs to keep in mind:

- Consolidated e-invoices cover B2C transactions where buyers do not request individual e-invoices, and are also used during applicable relaxation periods.

- Submission is required within 7 days of the end of each calendar month via the MyInvois portal.

- From 1 January 2026, any single transaction above RM10,000 must be issued as an individual e-invoice, even in B2C contexts.

- Certain sectors including electricity providers and telecommunications companies are prohibited from using consolidated e-invoices as of 1 January 2026.

- Required data fields include specific placeholder buyer information, product/service descriptions, aggregated line items, and correctly classified tax amounts.

- Automated ERP systems with MyInvois API integration significantly reduce compliance risk and administrative burden, especially for multi-branch operations.

A consolidated e-invoice isn’t just a list; it’s a specific digital file that summarizes many receipts into one. The challenge isn’t just sending the data, it’s the ‘digital handshake’ with the MyInvois portal every 7 days. If your POS or ERP system doesn’t automatically aggregate these receipts into the correct LHDN format, you’ll spend hours every month manually fixing data that should have been automated.

Staying ahead of these changes through regular engagement with official LHDN communications, coordination with your tax advisor, and investment in compliant technology infrastructure is the surest path to sustainable, penalty-free compliance.

FAQ About Consolidated E-Invoice

-

Can I issue consolidated e-invoices for B2B transactions?

Generally, no. B2B transactions require individual e-invoices with the buyer’s TIN and registration details so they can claim tax credits or deductions. Consolidated e-invoices are strictly for B2C sales where the buyer does not need formal tax documentation.

-

What happens after the relaxation period ends?

You must do a transition to real-time individual e-invoicing (within 72 hours) for all transactions that do not qualify for consolidation. While consolidated e-invoices remain an option for eligible B2C sales, they can no longer be used as a blanket substitute for your entire billing process.

-

Can each branch issue its own consolidated e-invoice?

Yes. IRBM allows businesses to consolidate at either the branch or entity level, provided all submissions are made under the correct legal TIN. The most important factor is ensuring every qualifying transaction is captured and none are omitted, regardless of the branch structure.

-

What if I miss the 7-day submission deadline for a consolidated e-invoice?

Missing the deadline is a compliance breach subject to penalties. If this happens, submit the document immediately and consult a tax advisor regarding voluntary disclosure. To avoid future risks, using an automated system with built-in reminders is highly recommended.

-

Do I need to share the consolidated e-invoice with my customers?

No. It is a reporting document for the IRBM, not a buyer-facing one. Customers should rely on their standard receipts or proof of purchase issued at the point of sale. You simply retain the validated consolidated document for your own audit and record-keeping.