What’s stopping the banking industry from achieving seamless digital transformation? While many financial institutions have adopted new technologies, keeping up with customer expectations, compliance, and security remains a complex task.

This is especially relevant to the banking industry in Malaysia, where over 90% of the population is already financially included. With such a high level of accessibility, banks must do more than offer services, they need to deliver consistent, digitized experiences.

From outdated infrastructure to intense fintech competition, the pressure to evolve is mounting. Without the right strategy, banks risk losing relevance in a rapidly shifting market.

Want to know how industry leaders are handling these challenges successfully? This article explores the top 10 issues banks face today, along with practical strategies to overcome them.

Key Takeaways

|

Top 10 Pressing Challenges Faced by the Banking Industry

The banking industry is continuously developing, with both traditional and technological challenges. From client expectations to regulatory complications, obstacles are building up like a tambak. Here’s a deeper look at the major concerns that banks face today.

1. Understanding customer expectations

Modern banking customers expect far more than just secure transactions. With the growing dominance of digital banking solutions, they want services that are personalized, convenient, and intuitive. From mobile apps to chat-based support, customers increasingly prefer digital interactions that are fast and frictionless.

This evolving demand means that banks must not only deliver seamless experiences but also anticipate what their users need. To meet these rising expectations in the banking industry, financial institutions should:

- Prioritize strong mobile security while enhancing usability to build digital trust.

- Combine the efficiency of tech-driven banking with personalized service models, such as hybrid banking that blends in-person and digital experiences.

- Utilize AI in banking industry settings to enhance customer profiling and provide proactive service recommendations.

2. Regulatory compliance

Staying compliant with Malaysia’s evolving regulatory landscape remains a major hurdle for banks. From Bank Negara Malaysia’s risk management frameworks to international standards like Basel III, compliance has become increasingly demanding and resource-heavy.

Manual workflows can’t keep up with strict timelines or complex reporting. Many institutions now rely on smarter financial management systems that help reduce the risk of human error and improve regulatory accuracy.

To stay compliant without slowing down operations, banks should:

- Invest in smart technology: Use tools that make gathering, analyzing, and reporting data easier. A solid accounting software setup can help you stay on top of requirements without scrambling for last-minute fixes.

- Stay updated on regulations: Regularly review Bank Negara Malaysia (BNM) updates and international standards to stay ahead of regulatory changes. Proactive planning helps banks adapt smoothly, avoiding last-minute compliance issues.

- Partner with experts: If managing everything in-house feels overwhelming, working with compliance consultants or legal advisors can give you peace of mind and a clear direction.

3. Security breaches

The growth of digital banking in Malaysia has introduced sophisticated cyber threats. Phishing scams and malware attacks targeting banks have increased in frequency and severity. Without advanced security measures, financial institutions risk losing customer data and trust.

Here are proven methods for stronger protection:

- Address Verification Service (AVS): AVS compares the billing address provided during a transaction with the one on record at the issuing bank. This helps flag suspicious activities and prevents fraud.

- End-to-End Encryption (E2EE): Data is encrypted at every point between the sender and receiver, safeguarding mobile payments and online transfers.

- Biometric Authentication: Facial recognition, iris scans, or fingerprints offer secure verification methods that are far more difficult to replicate than traditional PINs.

- Location-Based Authentication: Sometimes called geolocation identification, this method confirms a user’s identity by checking their physical location. Banks can use it to send transaction notifications or verify if the customer is near where the transaction occurs.

- Out-of-Band Authentication (OOBA): OOBA relies on two separate channels, such as sending a one-time code through SMS, email, or voice calls. The customer must enter this code to verify their identity, adding an extra layer of protection.

- Risk-Based Authentication (RBA): Also called adaptive authentication, RBA adjusts security based on the risk level of each transaction. Higher-risk activities may require stricter verification to ensure safety.

These tactics are crucial for securing technology in banking industry operations, particularly as digital adoption continues to increase.

4. Improving the mobile experience

With more users preferring mobile banking over in-branch visits, outdated or clunky apps can lead to customer churn. A seamless user experience (UX) is critical. Otherwise, customers won’t hesitate to switch.

To keep your customer going, focus on:

- Intuitive interfaces: Keep improving mobile banking apps for effortless navigation, especially for widely used tools like Touch ‘n Go eWallet or Boost. Ensure these third-party apps integrate flawlessly with your platform while delivering a user experience that matches or surpasses their convenience.

- Interactive video banking: Introduce video banking services to blend the personal touch of in-branch interactions with the ease of digital accessibility.

5. Rising expectations of digitized experiences

Today’s banking customers expect fast, convenient digital services. Millennials and Gen Z favor mobile platforms, while older generations appreciate face-to-face interactions. As preferences evolve, financial institutions must merge digital efficiency with human connection to maintain loyalty and competitiveness.

To address both ends of the spectrum:

- Install self-service kiosks in branches so customers can handle simple tasks independently or connect with advisors virtually.

- Equip financial advisors with AI tools and digital training so they can deliver personalized, tech-enhanced service that builds trust.

6. Outdated applications

Many banks claim to embrace digital transformation, but outdated systems often remain at the core. Legacy tools and disconnected platforms slow operations and limit growth. In a digital-first world, modernizing tech is critical to stay competitive.

- Use banking software like cloud-based reconciliation tools to streamline processes and reduce operational costs.

- Leverage AI in banking industry to automate tasks, offer personalized services, and enhance overall customer experience.

- Utilize cloud analytics for better insights into customer behavior, leading to smarter and faster decision-making.

- Stay open to innovation by monitoring trends like blockchain, which could unlock long-term value in banking technology.

If you’re ready to upgrade from outdated systems and unlock the benefits of cloud-based software, AI, and real-time analytics, click the pricing scheme banner below to explore HashMicro’s solutions.

7. Fintech competition

Fintech firms are rapidly transforming the financial landscape with innovations like peer-to-peer apps and crypto solutions. Their speed and accessibility are reshaping customer expectations and forcing banks to rethink their traditional strategies.

To remain competitive:

- Collaborate with fintechs: Explore partnerships or support fintech initiatives to benefit from their cutting-edge technologies and innovations.

- Focus on specialized services: Stand out by offering personalized options, like in-depth financial planning, that fintech companies typically don’t provide.

8. Changing business models

As compliance and capital expenditure rise, banks are under pressure to evolve their business models. Factors like low interest rates, shrinking ROE, and tighter trading margins continue to strain profitability while shareholder expectations stay high.

Here’s how banks are adapting to these pressures:

- Developing new competitive services: Creating innovative offerings to attract and retain customers.

- Reassessing business lines: Shifting focus to areas with stronger growth or profitability potential.

- Enhancing operational efficiency: Finding ways to reduce costs and improve overall productivity.

- Embracing flexibility: Structuring the organization to adapt to market changes and new demands quickly.

9. Internal Change

Adopting technology in banking industry operations demands a shift in roles and mindset.. As banks digitize, frontline employees must move beyond transactions to offer personalized, consultative support.

To support this transformation:

- Train employees for versatile roles: The “universal banker” model is becoming increasingly common, combining traditional teller duties with advanced financial skills to provide more comprehensive financial advice.

- Prioritize digital skills: Hire staff with digital expertise and provide regular training to ensure employees are prepared to support both face-to-face and digital customer interactions.

10. Customer Expectations and Competition

Customers now expect fast, seamless, and personalized banking experiences across all channels. As more digital-only banks and fintechs enter the scene, traditional institutions must work harder to retain customer loyalty and stay relevant in a saturated market.

Banks face tougher competition as more players, including fintech and digital-only banks, enter the scene. These competitors are agile and often more aligned with what younger, digital-native customers expect. In turn, this raises the bar for the customer experience industry-wide.

How to stay ahead:

- Highlight human expertise: Offer personalized financial advice that digital-only banks can’t match.

- Design omnichannel strategies: Provide consistent service, whether customers interact via mobile apps, web portals, or physical branches.

Empower Your Banking Industry Expertise with HashMicro Accounting Software

The banking industry is a serious business. Your expertise is, and always will be, at the heart of every strategic decision. But with HashMicro Accounting Software, you can make those decisions faster, more securely, and with far less manual work.

Trusted by 2,000+ companies, including the renowned Bank of China, HashMicro provides a user-friendly, intuitive system. Malaysian financial institutions can adopt it easily, with no need for extensive training. It is ISO-certified and LHDN-compliant, aligning with Malaysia’s financial regulatory standards for smooth and secure operations.

To make it even better, HashMicro introduces Hashy AI, an intelligent assistant designed to help you generate real-time reports, detect financial anomalies, and offer smart recommendations. With AI-powered insights, you can forecast more accurately and respond quickly to changes in your financial landscape.

HashMicro’s Accounting Software is packed with features that help tackle key banking challenges efficiently:

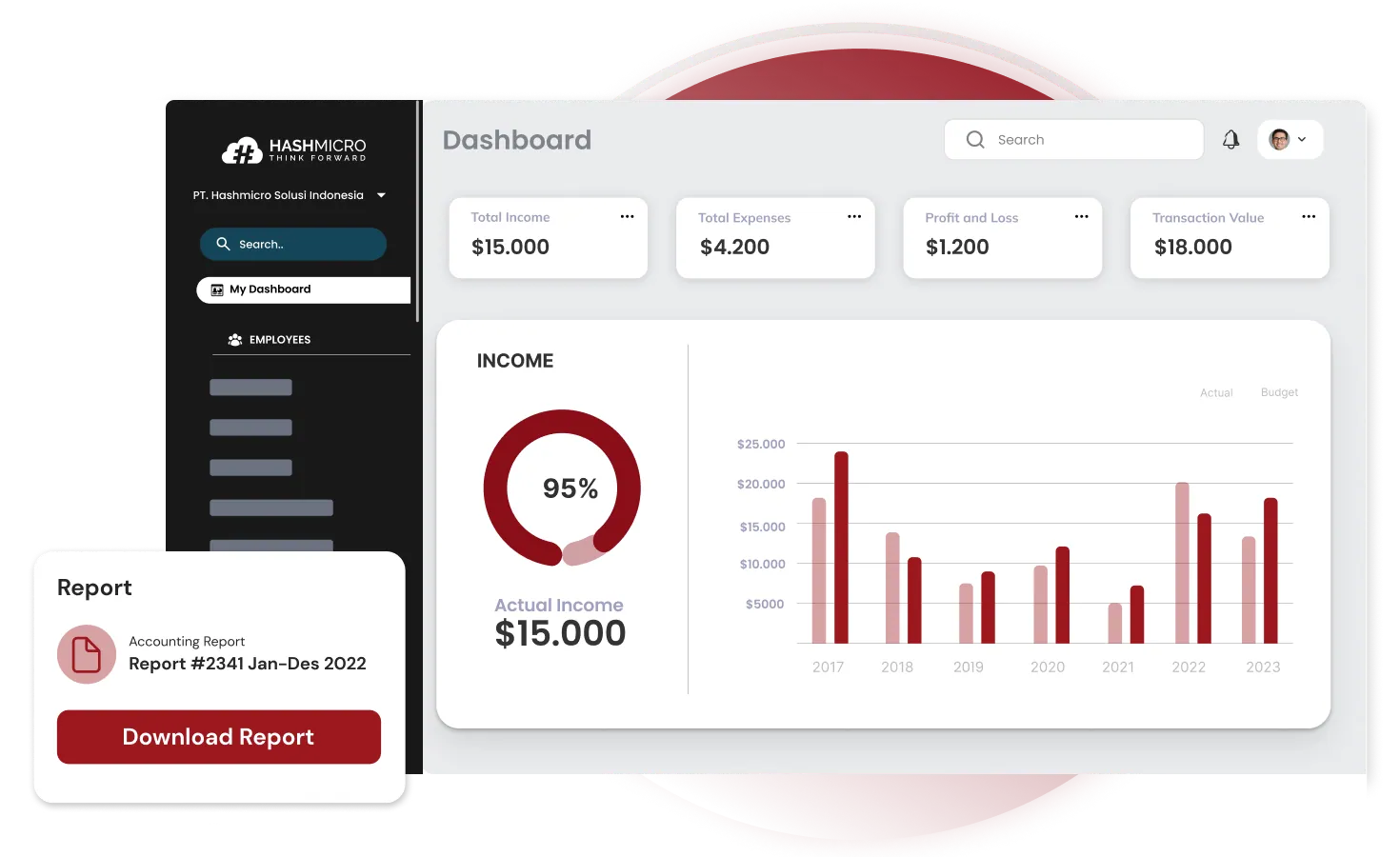

- Real-Time Financial Dashboard: Access live insights into cash flow, income, and expenses, all in one place.

- Cash Flow Forecasting Simplified: Plan ahead confidently by predicting your cash flow needs with precision.

- Quick and Secure Bank Reconciliation: Eliminate errors and save time with automated transaction matching.

- Accruals and Amortization Automation: Streamline complex calculations while ensuring compliance with accounting standards.

- Instant Financial Reports: Generate essential reports like balance sheets and income statements in seconds.

- Seamless System Integration: Connect easily with tools like Inventory, CRM, and Purchasing to unify workflows and improve service.

Conclusion

The banking industry in Malaysia is undergoing rapid transformation, shaped by evolving customer preferences, tighter regulations, and the urgent need for digital innovation. To stay ahead, banks must adopt smarter strategies and tools that boost operational resilience and customer satisfaction.

HashMicro Accounting Software, as part of a comprehensive ERP software, is designed to help Malaysian financial institutions simplify financial reporting, enhance compliance, and optimize workflows. With ISO certification, LHDN-ready standards, and the intelligent Hashy AI assistant, it enables banks to operate more efficiently and make informed decisions with ease.

Looking to streamline your banking operations and stay future-ready? Book a free demo today and experience how HashMicro empowers your financial team to focus on what truly matters—growth, innovation, and stronger client relationships.

FAQ About the Banking Industry

-

How does AI integration in banking software affect customer service delivery?

AI allows banks to provide more personalized and responsive services. Features like chatbots, fraud detection, and smart financial advice enhance engagement and reduce human error, leading to faster resolution of customer inquiries.

-

What are the first steps a bank should take before digital transformation?

Start with a digital readiness assessment, identifying which departments rely heavily on manual processes. Prioritize systems with the most customer interaction and ensure staff are trained for digital adoption.

-

How often should a bank upgrade or audit its existing accounting or ERP software?

A review should be done annually, with upgrades considered every 2–3 years, or when major compliance or customer experience improvements are required.

-

What risks come with adopting new fintech tools in traditional banking settings?

Data migration errors, temporary workflow disruptions, and a lack of employee training. These can be mitigated with proper implementation planning and vendor support.