Inventory valuation methods determine how a business assigns a monetary value to unsold stock at the end of each accounting period. This single decision shapes reported profits, tax liabilities, and the accuracy of every financial statement a company produces.

For Australian businesses, choosing the right method is not just an internal accounting preference. It affects your compliance with the Australian Taxation Office (ATO), adherence to IFRS, and the credibility of every financial report submitted to stakeholders.

Each method produces a different Cost of Goods Sold figure, which flows directly into gross profit and taxable income. Financial controllers who understand these differences are better equipped to protect margins, plan pricing accurately, and meet their regulatory obligations.

Key Takeaways

Inventory valuation methods assign a cost to unsold stock and determine how much is expensed as COGS each reporting period.

Inventory valuation methods matters because they supports ATO compliance, accurate COGS reporting, and informed pricing decisions for Australian businesses.

The four main inventory valuation methods are FIFO, WAC, Specific Identification, and LIFO, each suited to different business types and stock volumes.

Implementing inventory valuation methods requires a full audit, method selection aligned with AASB 102, and software to automate calculations and landed cost capture.

What Is Inventory Valuation?

Inventory valuation methods are standardized accounting techniques used to assign a cost to the goods a business holds at the end of a reporting period. The value assigned to unsold inventory appears on the balance sheet as a current asset.

The chosen method also determines how much cost is transferred to the income statement as the Cost of Goods Sold (COGS). Since COGS is deducted from revenue to calculate gross profit, the method has a direct impact on reported earnings.

Inventory rarely stays at a fixed cost throughout the year. Prices shift due to inflation, supplier changes, import duties, and freight costs, making a consistent and systematic valuation method essential for accurate reporting.

In Australia, inventory valuation must comply with AASB 102, the local accounting standard aligned with IFRS. The ATO also requires businesses to value trading stock consistently at the end of each income year.

The true value of inventory extends beyond the purchase price alone. Landed costs, including freight, import duties, and transit insurance, must also be included when calculating the full cost of stock on hand.

"Selecting the right inventory valuation method is one of the most consequential decisions a finance team makes. It touches every figure on your financial statements, from COGS to taxable income."

Why Inventory Valuation Matters for Businesses

The method a business uses within an Australian stock management system affects financial reporting, tax, and pricing decisions. It shapes your financial reporting, tax obligations, pricing accuracy, and how management interprets business performance.

1. Accurate Financial Reporting

Inventory is typically one of the largest current assets on a business’s balance sheet. Consequently, overstating or understating its value distorts your total assets, retained earnings, and key financial ratios used by stakeholders.

Ratios like the current ratio and quick ratio depend on accurate asset figures. Misvalued inventory can mislead creditors, investors, and board members who are assessing the company’s liquidity and financial position.

2. Tax Compliance Requirements

The ATO requires businesses to compare the value of trading stock at the start and end of each income year. If the closing value exceeds the opening value, the difference is treated as assessable income.

The ATO permits businesses to value trading stock at cost price, market selling value, or replacement value. Using a non-compliant method can result in tax penalties, audits, and the need to restate prior financial filings.

3. Cost of Goods Sold (COGS) Accuracy

COGS is calculated using this formula: Beginning Inventory plus Purchases minus Ending Inventory. The valuation method applied to ending inventory directly controls the COGS figure and therefore the gross profit reported.

A higher ending inventory value produces a lower COGS and higher reported profit. A lower ending inventory value does the opposite, reducing your reported profit and taxable income.

4. Informed Pricing and Profit Decisions

Accurate inventory valuation gives management reliable data when setting product prices and reviewing profit margins. Without it, pricing decisions may be based on outdated or misleading cost figures.

In periods of inflation, some methods can make margins look stronger than they actually are. Relying on these inflated figures may underprice future stock and face cash flow shortfalls when replenishing at higher costs.

Key Inventory Valuation Methods

The accounting profession has developed several standardized inventory valuation methods, each based on different assumptions about how costs flow through a business. Understanding the mechanics and limitations of each method is essential for you before selecting the right approach.

Australian businesses are required to choose a method that complies with AASB 102 and ATO guidelines. This generally limits the practical options to FIFO, Weighted Average Cost, and Specific Identification.

1. First In, First Out (FIFO)

FIFO assumes that the oldest stock purchased is the first to be sold. The costs assigned to the earliest inventory batches are transferred to COGS, while the most recent purchase costs remain on the balance sheet as ending inventory.

This method aligns with how most businesses physically manage their stock, particularly where perishable or time-sensitive goods are involved. It is widely accepted under both IFRS and ATO guidelines for Australian statutory reporting.

For example, if a business buys 100 units at $50 in January and 100 units at $60 in February, then sells 100 units, FIFO assigns the $50 batch cost to COGS. The remaining 100 units are valued at $60 each on the balance sheet.

During inflation, FIFO produces a lower COGS and higher gross profit, which increases the company’s tax liability in the short term. However, the balance sheet reflects more current and accurate inventory values.

2. Last In, First Out (LIFO)

LIFO assumes that the most recently purchased stock is the first to be sold. This means the latest, higher costs are expensed to COGS first, which reduces reported profit during periods of inflation.

Australian businesses should note that LIFO is not permitted under IFRS or accepted by the ATO for statutory reporting. It is covered here for reference, as it remains in use in some international jurisdictions such as the United States.

3. Weighted Average Cost (WAC)

WAC calculates a single average cost per unit across all inventory batches and applies it uniformly to both COGS and ending inventory. Hence, it smooths out price fluctuations and stabilizes reported margins over the accounting period.

The formula is straightforward: divide the total cost of goods available for sale by the total number of units available. Using the same example above, ($5,000 + $6,000) / 200 units = $55 per unit applied to both COGS and ending inventory.

WAC is best suited for businesses dealing in high-volume, identical products that are difficult to separate by purchase batch. Fortunately, it is accepted under IFRS and by the ATO for Australian tax reporting.

4. Specific Identification Method

This method tracks the exact purchase cost of each individual item in inventory. When an item is sold, its specific historical cost is transferred directly to COGS with no averaging or assumptions applied.

It is most practical for businesses selling unique, high-value items such as vehicles, custom machinery, or fine jewelry. Each item must carry a unique identifier such as a serial number or Vehicle Identification Number (VIN).

The method provides the most accurate match between actual costs and actual sales revenue. However, the administrative effort required makes it impractical for businesses managing high-volume, low-cost inventory.

Noted. The Across Industries H2 must always contain H3s, one per industry covered. Here is the corrected section:

Inventory Valuation Methods Across Industries

No single inventory valuation method suits every business equally. The right choice depends on the nature of the product, the volume of stock, and the physical practicalities of how goods move through the supply chain.

- Retail and Fast-Moving Consumer Goods

FIFO is the standard choice for supermarkets, grocers, and FMCG businesses. These operations must sell oldest stock first to prevent spoilage and product expiry, so aligning the financial method with the physical flow of goods produces accurate and consistent reporting.

- Manufacturing and Heavy Machinery

Manufacturers of bespoke or high-value products, such as commercial vehicles or industrial equipment, rely on the Specific Identification method. Each unit carries a unique serial number or VIN, making it practical to track the exact cost of every item through production and sale.

- Mining, Agriculture, and Bulk Commodities

Australian mining and agricultural businesses extract or harvest commodities that are immediately mixed into existing stockpiles, making batch-level tracking impossible. WAC is the most logical and compliant choice, smoothing out the price volatility common in global commodity markets.

- Wholesale Distribution

Wholesale distributors managing large volumes of identical products benefit from WAC’s ability to stabilize COGS across fluctuating supplier prices. It also reduces the administrative burden of tracking individual batch costs at high transaction volumes.

How to Implement an Inventory Valuation System

Transitioning to a new inventory valuation method is a significant operational and financial undertaking. It requires cross-departmental coordination, updated systems, and clear procedures to ensure compliance from the first day of implementation.

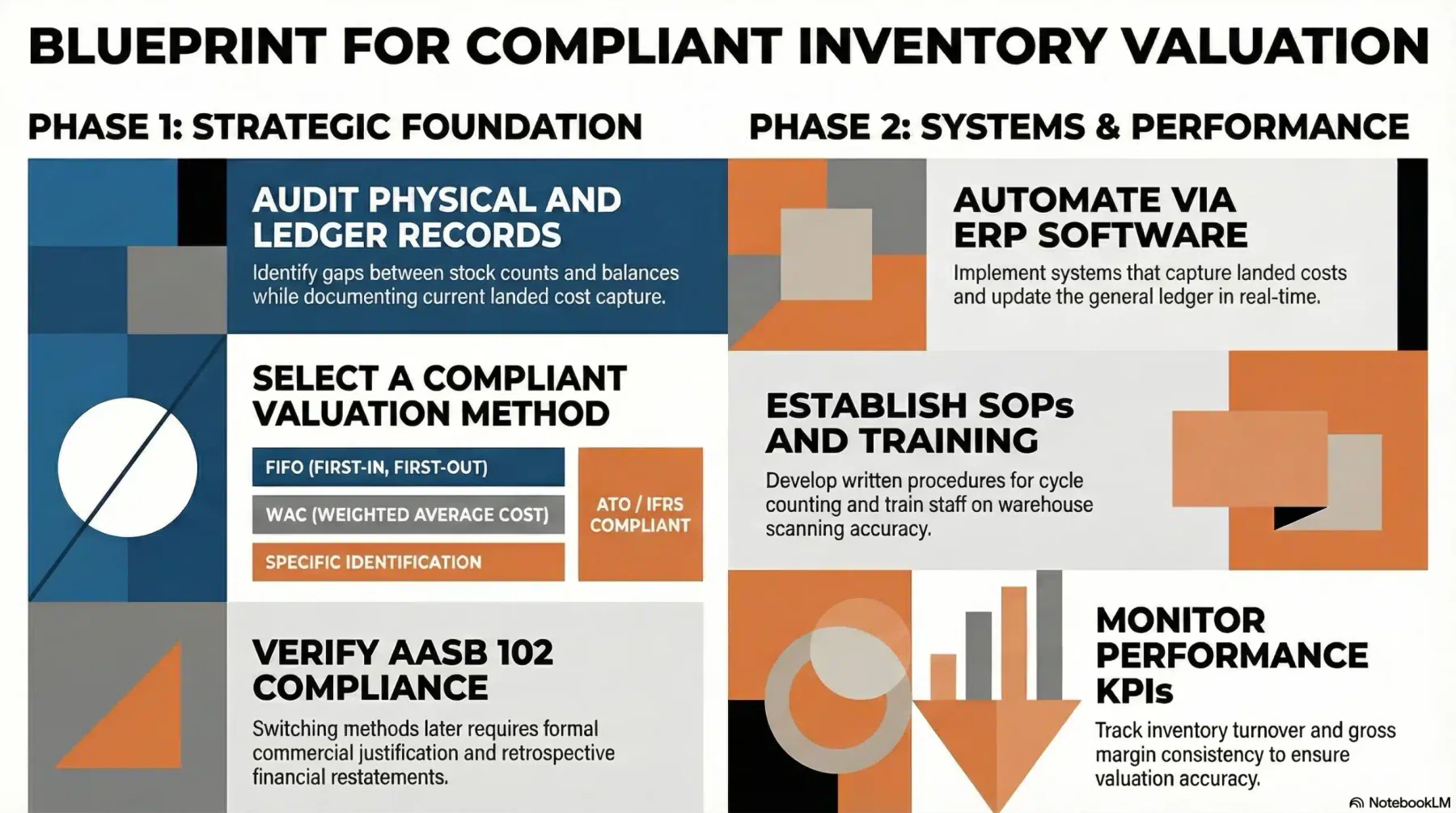

Step 1 — Audit Your Inventory and Records

Begin by conducting a full audit of your current stock, accounting records, and warehouse processes. Identify any gaps between physical counts and ledger balances, and document how landed costs are currently captured and recorded.

Step 2 — Choose the Right Method

Work with your CFO and external auditors to select the method that best suits your product type, volume, and financial reporting requirements. Australian businesses must choose from FIFO, WAC, or Specific Identification to remain ATO and IFRS compliant.

Confirm that the chosen method complies with AASB 102 before making any changes. Switching methods after the fact requires formal commercial justification and retrospective restatement of prior period financial statements.

Step 3 — Deploy ERP or Inventory Software

Manual spreadsheets cannot reliably support the demands of modern inventory valuation at scale. Implement a stock inventory solution that applies your chosen method and updates the general ledger in real time as stock moves.

The system should capture landed costs, including freight and import duties, and factor them into each unit’s total cost. Automating these calculations reduces human error and ensures consistent application across every transaction.

Step 4 — Establish Standard Operating Procedures

Develop SOPs for receiving goods, recording costs, and conducting cycle counts using ABC classification to prioritise high-value inventory. Cycle counting involves auditing a rotating subset of inventory regularly, rather than relying on a single annual stocktake.

Step 5 — Train Staff and Monitor Performance

Provide structured training for warehouse staff and finance teams so each group understands how their actions affect financial reporting. Warehouse scanning errors have direct and measurable consequences for valuation accuracy.

Track KPIs such as inventory turnover ratio, gross margin consistency, and frequency of write-downs. These metrics signal whether your chosen valuation method is delivering accurate and useful financial data over time.

Common Pitfalls in Inventory Valuation

Even with robust systems in place, businesses can easily fall victim to critical accounting errors that distort their financial reality. Recognizing these pitfalls is the first step toward safeguarding your balance sheet.

- Inconsistent Application of Valuation Methods: Switching valuation methods from year to year to influence profitability or tax outcomes is a serious violation of IFRS consistency requirements. Any change must be commercially justified and accompanied by restated prior period financial statements.

- Ignoring or Misallocating Landed Costs:

Many businesses fail to include landed costs such as freight, import duties, and transit insurance in their inventory value. This leads to understated assets and inflated profit margins that do not reflect the true cost of acquiring stock.

- Failing to Account for Shrinkage and Obsolescence:

Neglecting to write down obsolete, damaged, or missing stock results in a balance sheet that overstates the value of assets. Regular physical audits and prompt write-downs are essential to keeping inventory records accurate and compliant.

Advanced Inventory Valuation Practices

Selecting the right method is only the starting point. Businesses must also apply it consistently, capture all relevant costs, and maintain accurate stock records to ensure financial statements remain reliable and audit-ready.

The Lower of Cost or Net Realizable Value (NRV) Rule

Under AASB 102, inventory must be reported at the lower of its historical cost or its Net Realizable Value (NRV). NRV is the expected selling price minus any estimated costs required to complete and sell the item.

If market conditions cause NRV to fall below cost, a write-down must be recorded immediately. This prevents assets from being overstated on the balance sheet and ensures conservative, compliant financial reporting.

Use Consistent Methods Across Periods

Applying the same valuation method consistently from one period to the next is required under IFRS. Consistency allows stakeholders to compare financial statements across years with confidence in the underlying accounting data.

Conduct Regular Physical Audits

Cycle counting is the practice of auditing a rotating portion of inventory throughout the year rather than performing one large annual stocktake. It catches discrepancies early and keeps ledger balances aligned with actual stock on hand.

Use Inventory Software to Automate Valuation

Inventory tracking software can automate valuation methods, calculate landed costs, and generate accurate COGS with less manual input. This removes a major source of human error from the valuation process.

When selecting software, look for systems that integrate with your existing accounting platform and support real-time updates to inventory values as stock is received and sold. Automation also improves audit readiness and speeds up financial reporting cycles.

Conclusion

Choosing the right inventory valuation method is a foundational financial decision for any Australian business that holds stock. The method chosen affects COGS, gross profit, taxable income, and balance sheet accuracy across every reporting period.

Australian businesses must work within the FIFO, WAC, or Specific Identification frameworks to stay compliant with AASB 102 and ATO requirements. Each method carries distinct advantages depending on the type and volume of stock being managed.

Consistent application, accurate landed cost capture, and regular physical auditing are the foundations of a reliable valuation system. If you want to implement these methods effectively, you can book a free consultation anytime.

Frequently Asked Question

The main inventory valuation methods used in Australia are FIFO, Weighted Average Cost, and Specific Identification. LIFO is not accepted by the ATO or permitted under IFRS for Australian statutory reporting.

No. LIFO is not permitted under IFRS or accepted by the ATO for statutory financial reporting in Australia. Australian businesses must use FIFO, WAC, or Specific Identification to remain compliant with AASB 102.

FIFO assigns the oldest inventory costs to COGS first, leaving the most recent costs on the balance sheet. WAC blends all purchase costs into a single average unit cost applied equally to both COGS and ending inventory.