Accounts receivable (AR) is the outstanding payment a business is waiting to collect from customers after delivering products or services on credit. It represents unpaid invoices that are expected to be paid within the agreed payment period.

Accounts receivable refers to payments a business expects to collect after delivering goods or services on credit. It works by recording each transaction as a receivable and converting it into cash through invoicing, collection, and reconciliation.

When managed well, accounts receivable supports stable cash flow and reduces delays. A structured approach improves visibility and keeps operations running smoothly.

Accounts receivable helps businesses maintain stable cash flow by managing credit transactions and ensuring timely collection. Many companies now rely on software for managing AR to centralise records, track balances, and reduce manual effort, especially as transaction volumes grow.

Key Takeaways

Accounts receivable represents expected cash from credit sales, recorded as short-term assets until payment is collected.

Credit approval, invoicing, and follow up form a structured process that ensures payments are collected on time.

Ageing reports identify overdue balances and reveal payment risks, allowing businesses to act before cash flow is affected.

Clear policies, automation, and consistent follow up improve collection efficiency and maintain financial visibility.

What Accounts Receivable Means for Business Cash Flow

Accounts receivable represents payments a business expects to collect after delivering goods or services on credit. These amounts are classified as short-term credit and recorded as current assets on the balance sheet until payment is received.

This directly affects cash flow. Faster collection improves liquidity, allowing businesses to fund operations and manage expenses more effectively. Poor accounts receivable management increases the risk of bad debt and can erode the working capital a business needs to meet its own obligations.

Accounts receivable depends on clear credit policies, accurate invoicing, and consistent follow up. Many companies strengthen control by improving customer payment tracking, which helps teams see who has paid, who is overdue, and where attention is needed.

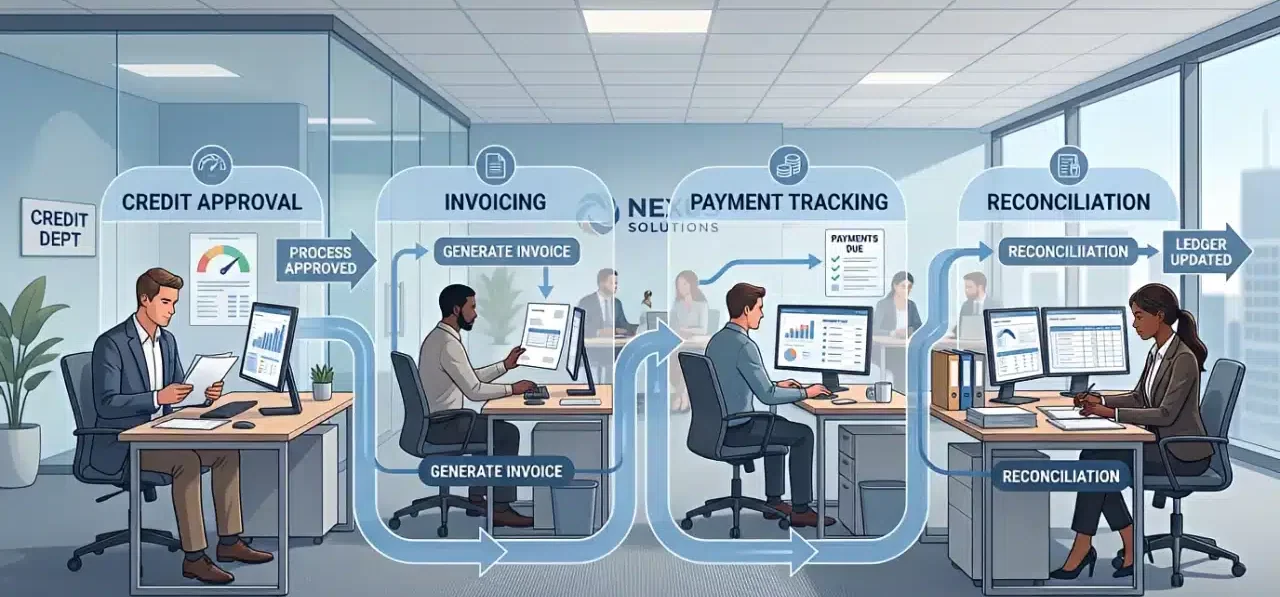

How the Account Receivable Process Flows in Practice

Managing accounts receivable involves a structured flow from sales to collection. Each stage ensures payments are received on time and cash flow remains stable.

Rather than working as isolated tasks, these activities are interconnected. Delays or errors in one stage can affect the entire cycle, making consistency and accuracy essential.

The table below summarises the key stages in the accounts receivable process and how each step supports cash flow management.

| Process Stage | Description | Impact on Cash Flow |

|---|---|---|

| Credit Approval | Evaluate customer creditworthiness before approving sales | Reduces risk of late or unpaid invoices |

| Invoice Creation | Issue accurate and timely invoices with complete details | Speeds up payment processing |

| Payment Terms Alignment | Define clear due dates and payment conditions | Sets expectations and avoids disputes |

| Collection and Follow Up | Track outstanding invoices and send reminders | Improves payment timeliness |

| Payment Reconciliation | Match incoming payments with invoices | Ensures accurate records and visibility |

Credit approval and sales initiation

The process begins when a business decides to offer goods or services on credit. Before approving the transaction, it is important to assess the customer’s financial reliability and define appropriate credit limits.

Clear credit control reduces the risk of overdue payments. It also ensures that sales growth does not come at the expense of cash flow stability.

Invoice creation and documentation

Once the transaction is completed, invoices must be issued accurately and without delay. This includes clear details such as pricing, quantities, due dates, and payment instructions.

Well-prepared invoices reduce disputes and confusion. As a result, customers are more likely to process payments on time.

Payment terms alignment

Payment terms define when and how customers are expected to settle their balances. These terms should be agreed upon early and consistently reflected in all documentation.

Clear expectations help avoid misunderstandings. They also provide a reference point for follow up if payments are delayed.

Collection and follow up

After invoices are issued, businesses need to actively monitor outstanding balances. This includes sending reminders before and after due dates when necessary.

Many businesses use payment follow-up tools to automate reminders and maintain consistent communication without straining relationships.

Payment reconciliation

The final stage occurs when payments are received and matched with the correct invoices. Accurate reconciliation ensures financial records remain reliable and up to date.

This step is essential for maintaining visibility into outstanding balances. It also prevents errors that could affect reporting and future collection efforts.

Recording Accounts Receivable in Accounting Systems

Recording accounts receivable ensures every credit transaction is reflected accurately in financial records. This process tracks how receivables are recognised and later converted into cash.

Initial journal entry for credit sales

When a business completes a sale on credit, the transaction is recorded as accounts receivable and revenue. This reflects the right to receive payment even though cash has not been collected.

This entry increases assets and recognises income. It ensures financial statements reflect actual business activity.

Recording payment received

When payment is collected, the receivable is converted into cash. The accounts receivable balance decreases while the cash balance increases.

This does not affect revenue, as it was recorded earlier. It simply updates the composition of assets in the financial records.

Accounts Receivable vs Accounts Payable

Accounts receivable and accounts payable represent opposite sides of business cash flow. Accounts receivable refers to incoming customer payments, while accounts payable refers to payments owed to suppliers or vendors.

Both play an important role in working capital management. Managing them properly helps businesses maintain healthier cash flow and financial stability.

| Aspect | Accounts Receivable | Accounts Payable |

| Definition | Money owed by customers to the business | Money the business owes suppliers or vendors |

| Financial Classification | Recorded as a current asset | Recorded as a current liability |

| Cash Flow Impact | Supports incoming cash flow | Represents outgoing cash obligations |

| Main Focus | Collect customer payments | Manage supplier payments |

| Common Activities | Invoicing, collection, reconciliation | Bill processing, payment scheduling |

Key Payment Terms in Accounts Receivable

Payment terms define when and how customers settle invoices. Clear terms reduce disputes and improve collection efficiency.

- Net payment terms: Net terms specify the number of days a customer has to pay, such as 30 or 60 days. These terms provide a standard timeline for payment processing.

- Early payment discounts: Early payment discounts encourage customers to pay before the due date by offering a small reduction in the total amount. This helps accelerate cash inflow.

- Late payment penalties: Late payment penalties apply when invoices are not settled on time. These charges encourage timely payment and discourage delays.

Well-defined terms also help manage payables and receivables together, giving businesses a clearer view of incoming and outgoing obligations.

Accounts Receivable Ageing and Reporting Insights

Accounts receivable ageing shows how long invoices remain unpaid and where collection risks are building. Instead of just tracking totals, it provides visibility into payment patterns and collection risks.

This insight allows teams to prioritise follow up and detect potential cash flow issues earlier. It also supports better planning by showing how quickly receivables are being converted into cash.

What an ageing report shows

An ageing report categorises outstanding invoices based on how long they have been due, such as current, 30 days, or over 90 days. This structure highlights which accounts are at risk of late payment.

By segmenting receivables, businesses can quickly identify problem accounts. This makes collection efforts more focused and efficient.

How ageing reports support cash flow decisions

Ageing reports provide a clearer picture of expected cash inflows over time. This helps businesses plan expenses, manage liquidity, and avoid shortfalls.

It also strengthens cash inflow tracking, which allows businesses to act before delays affect operations.

"Strong visibility into ageing receivables allows businesses to act earlier on payment risks and maintain more predictable cash flow."

Core Accounts Receivable Metrics for Performance Tracking

Tracking key metrics helps businesses measure how efficiently receivables are managed. These indicators provide a clearer view of collection speed and overall financial health.

- Days sales outstanding: Days sales outstanding measures how long it takes to collect payment after a sale. Lower values indicate faster collection and better cash flow efficiency.

- Receivables turnover ratio: Receivables turnover ratio shows how often a business collects its receivables within a period. A higher ratio indicates stronger collection performance.

How Different Industries Manage Accounts Receivable

Accounts receivable practices vary across industries depending on billing complexity, customer behaviour, and operational risks. Each sector requires a different approach to maintain cash flow and minimise payment delays.

- Healthcare and medical billing

Healthcare receivables involve insurers, making the process longer and more complex. Delays often result from approvals, rejections, or incomplete documentation.

- Construction and contracting

Construction businesses rely on milestone-based billing, where payments are tied to project progress. This creates irregular cash flow and requires close tracking of payment timelines.

- SaaS and subscription models

SaaS businesses manage recurring invoices through automated billing systems. The main challenge is failed payments, which are handled through reminders and retry mechanisms.

- Manufacturing and wholesale distribution

Manufacturing and distribution businesses deal with high-value transactions and extended credit terms. Strong credit control is needed to reduce risk and maintain stable cash flow.

Building an Effective Accounts Receivable System

An effective accounts receivable system ensures each stage runs consistently and supports timely collection. A structured approach reduces errors and improves cash flow predictability.

Without clear processes, receivables can become difficult to track and manage. This often leads to delays, disputes, and reduced financial visibility.

Define credit policies

Clear credit policies set the foundation for managing receivables. They define who qualifies for credit and how much risk the business is willing to accept.

Strong policies reduce exposure to bad debt. They also create consistency across all credit decisions.

Standardise and automate invoicing

Automated invoicing ensures bills are issued accurately and on time. Businesses using an ERP system can automate the entire AR cycle within a single platform, reducing manual effort and improving data accuracy across teams. This reduces errors and shortens the payment cycle.

Consistent invoicing also improves customer clarity. As a result, disputes and delays are minimised.

Establish a structured collection process

A structured collection process ensures follow ups are consistent and timely. This includes reminders before and after due dates.

Regular communication improves payment behaviour. It also helps maintain professional customer relationships.

Enable flexible payment options

Providing multiple payment options makes it easier for customers to settle invoices. This reduces friction in the payment process.

Simpler payment methods often lead to faster collections. It also improves the overall customer experience.

Maintain regular reconciliation and reporting

Regular reconciliation ensures payments are matched accurately with invoices. This keeps financial records up to date and reliable.

Consistent reporting provides visibility into receivables performance. It also supports better decision making.

Common Accounts Receivable Challenges and Solutions

Accounts receivable issues often come from gaps in control and coordination. When not addressed early, these challenges can delay payments and disrupt cash flow.

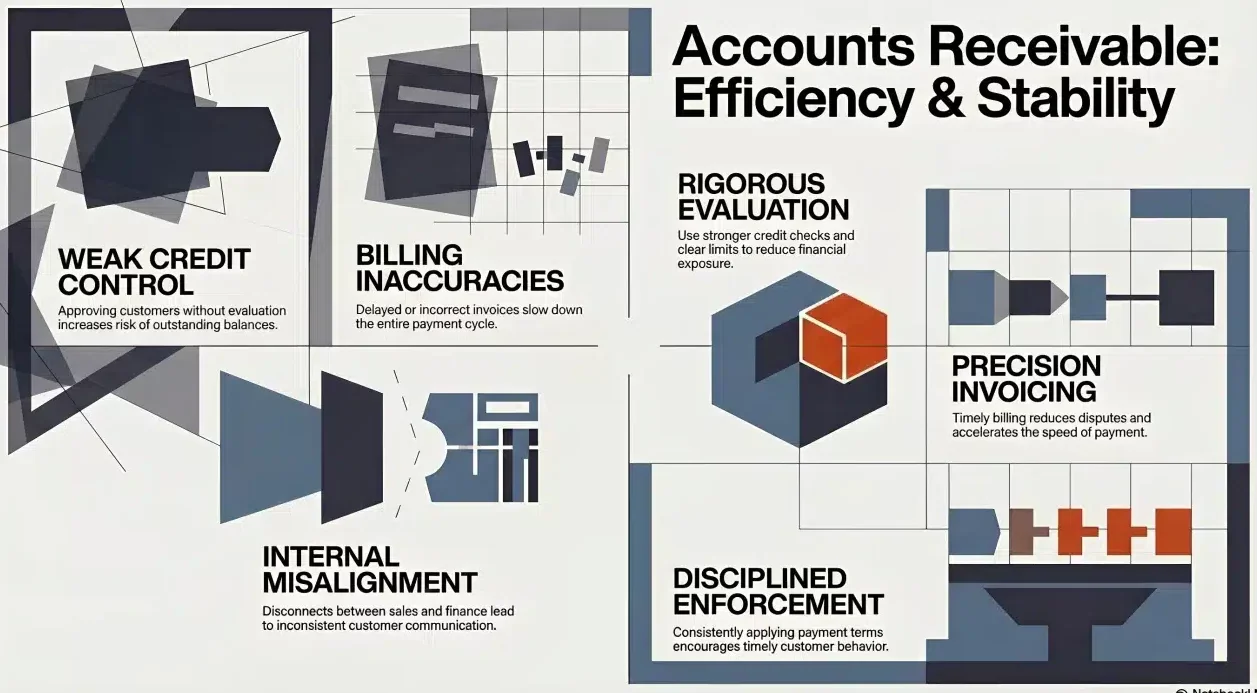

Weak credit control

Approving customers without proper evaluation increases the risk of late or unpaid invoices. This often leads to higher outstanding balances over time.

Stronger credit checks and clear limits help reduce exposure. It also ensures sales growth remains aligned with financial stability.

Delayed or inaccurate invoicing

Late or incorrect invoices slow down the entire payment cycle. Customers may delay payment due to missing or unclear information.

Timely and accurate invoicing improves payment speed. It also reduces disputes that can extend collection timelines.

Poor internal coordination

Poor coordination between sales, finance, and operations can lead to billing errors and delayed follow-ups. The issue becomes more serious for multi-branch businesses using separate or outdated data, making it difficult to track outstanding receivables accurately.

Better coordination ensures issues are resolved quickly. It also improves overall efficiency in managing receivables.

Failure to enforce payment terms

Payment terms lose effectiveness when they are not consistently enforced. Customers may delay payments if there are no clear consequences.

Applying terms consistently encourages timely payment. It also reinforces financial discipline across customer accounts.

Advanced Accounts Receivable Strategies for Optimisation

As receivables processes mature, businesses can adopt more advanced strategies to improve efficiency and cash flow performance. These approaches focus on automation, predictive insights, and financial flexibility.

- Dynamic discounting: Dynamic discounting adjusts incentives based on how early a payment is made. This encourages faster payment while maintaining flexibility for customers.

- AI and predictive analytics: AI analyses historical payment behaviour to identify potential delays. This allows businesses to act earlier and prioritise high-risk accounts.

- Accounts receivable financing: Receivable financing allows businesses to convert outstanding invoices into immediate cash. This helps maintain liquidity without waiting for payment cycles.

- Self service customer portals: Customer portals allow clients to view invoices, track balances, and make payments independently. This reduces administrative workload and speeds up collections.

Conclusion

Accounts receivable helps businesses maintain stable cash flow by ensuring timely collection of credit transactions. With a structured approach, companies can reduce delays and improve financial visibility.

As operations grow, inconsistent processes can increase risk and limit control. Businesses that manage receivables effectively can maintain predictable cash flow and stronger financial performance.

If your business wants to improve accounts receivable management and strengthen cash flow control, you can request a free consultation with our expert to find the right approach for your needs.

FAQ About Accounts Receivable

Uncollected receivables can reduce cash flow and limit a business’s ability to cover operational expenses. Over time, it may also increase the risk of bad debt.

Businesses can reduce overdue receivables by setting clear payment terms, automating invoicing, and following up consistently with customers.

A good turnover ratio depends on the industry, but generally a higher ratio indicates faster collection and better cash flow management.

Credit terms are usually based on customer creditworthiness, transaction history, and business risk tolerance.