Managing fixed asset depreciation plays a key role in keeping financial records accurate and reliable. Every business relies on physical assets such as machinery, vehicles, and equipment to operate and generate revenue. However, these assets do not hold their original value forever.

Fixed asset depreciation ensures financial statements reflect economic reality. When handled correctly, it supports better budgeting, clearer reporting, and more informed decisions around asset investment and replacement.

Key Takeaways

Understanding fixed asset depreciation ensures asset values and expenses reflect real business usage.

Proper depreciation supports tax accuracy, cash flow clarity, and reliable financial reporting.

Selecting the right depreciation method aligns costs with how assets generate value.

A structured depreciation strategy reduces errors and strengthens audit readiness.

What Is Fixed Asset Depreciation?

Depreciation on fixed assets is an accounting method that allocates the upfront cost of a tangible asset across its useful lifespan. It accounts for the gradual decline in value caused by wear and tear, ageing, or obsolescence, matching the asset's cost to the revenue it generates over time.

Fixed asset depreciation refers to the accounting practice of spreading the cost of a physical asset across its useful life. Rather than recording the full cost at purchase, a company allocates the expense gradually as the asset supports operations over time.

Fixed assets include buildings, machinery, office furniture, IT equipment, and company vehicles. Land is not depreciated because it does not lose value over time. Since these assets provide long-term value, businesses must capitalise and depreciate them over their useful life.

This approach aligns with the Matching Principle, which requires expenses to be recorded in the same period as the revenue they help generate. As a result, profits remain consistent and realistic across reporting periods.

Depreciation differs from amortisation and depletion. Amortisation applies to intangible assets like software or licences, while depletion applies to natural resources. Depreciation also does not measure market value, as an asset may remain useful even after it is fully depreciated.

Why Fixed Asset Depreciation Matters for Businesses

Fixed asset depreciation directly affects tax outcomes and cash flow management. Because depreciation counts as a deductible expense, it reduces taxable income and helps businesses retain more working capital.

Depreciation further supports capital planning. By tracking asset ageing and remaining value, finance teams can plan replacements early and avoid costly disruptions caused by sudden equipment failure.

How to Calculate Fixed Asset Depreciation

Calculating fixed asset depreciation requires clear data and consistent accounting policies. Businesses must identify the asset cost, estimate its useful life, assess residual value, and apply an appropriate depreciation method. Together, these inputs form a reliable depreciation schedule.

1. Determine the asset cost

The asset cost includes more than the purchase price. It covers all expenses required to bring the asset into use, such as freight, duties, installation, and testing. However, training and ongoing maintenance remain operating expenses.

2. Estimate the useful life

Useful life reflects how long the asset delivers economic value, not how long it physically lasts. Businesses often rely on past experience, supplier guidance, and taxation authority guidelines when making this estimate.

3. Identify the salvage value

Salvage value represents the expected amount recovered when the asset is disposed of. This value reduces the total amount depreciated and often reflects resale or scrap expectations.

4. Select a depreciation method

The method should match how the asset is consumed. Some assets lose value evenly over time, while others decline faster in early years. Once selected, the method should remain consistent.

5. Calculate the depreciation expense

The final calculation records depreciation as an expense and updates accumulated depreciation on the balance sheet. Partial-year adjustments apply when assets enter service mid-year.

Common Fixed Asset Depreciation Methods

Choosing the right depreciation method ensures expenses align with asset usage. Most companies rely on a small number of accepted approaches, each suited to different asset types.

1. Straight-line method

This method spreads depreciation evenly across the asset’s useful life. It works best for assets that deliver consistent value, such as office furniture and buildings, and offers predictable expense patterns.

Formula: Asset Cost − Salvage Value / Useful Life

2. Declining balance method

This accelerated method records higher depreciation in early years. Businesses often use it for vehicles and technology assets that lose value quickly after purchase.

Formula: Beginning Book Value X Depreciation Rate

3. Units of production method

This approach links depreciation to actual usage rather than time. It suits machinery where wear depends on output, making it common in manufacturing environments. This also helps businesses better understand asset value over time based on actual performance.

Depreciation Rules for Australian Businesses

Australian businesses follow depreciation rules set by the Australian Taxation Office, which determines how assets are written off for tax purposes.

The ATO assigns effective life estimates to most asset types, which businesses can adopt directly or challenge with their own assessment.

Small businesses accessing the instant asset write-off threshold can deduct eligible assets immediately in the year of purchase, rather than depreciating them over time.

Under the general small business pool, assets that do not qualify for immediate write-off are pooled together and depreciated at a set rate, reducing administrative complexity.

For larger businesses, the ATO’s diminishing value and prime cost methods mirror the declining balance and straight-line approaches used in financial reporting.

However, tax depreciation and accounting depreciation often differ, so companies must maintain separate records to satisfy both the ATO and Australian Accounting Standards Board requirements.

Industry-Specific Use Cases for Fixed Asset Depreciation

Different industries rely on different asset types, which affects how depreciation applies in practice. Understanding these variations helps businesses align accounting with operational reality.

1. Manufacturing and heavy industry

Manufacturers often depreciate machinery based on production output. This method ensures costs rise during high-demand periods and align with revenue generation.

2. Transportation and logistics

Fleet assets degrade based on distance and usage. Accurate depreciation helps companies time vehicle replacement and manage maintenance costs effectively.

3. Information technology

Technology assets lose value due to rapid innovation rather than physical wear. Accelerated depreciation reflects this decline and supports realistic budgeting.

4. Healthcare

Medical facilities rely on high-value equipment that impacts both compliance and pricing. Depreciation affects overheads, funding decisions, and upgrade planning. Many facilities also rely on software for fixed asset tracking to manage equipment lifecycle and reporting.

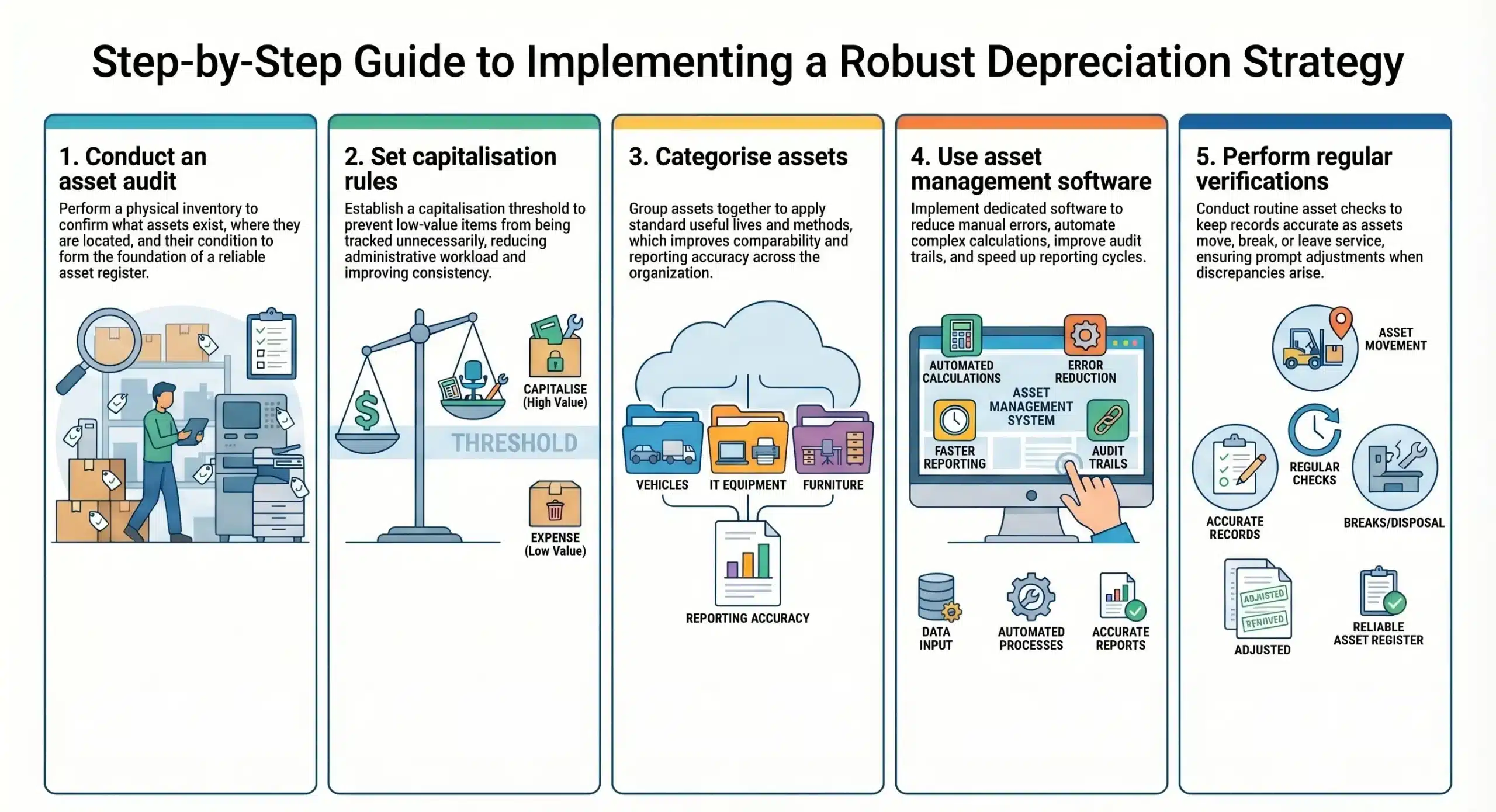

A Guide to Implementing a Robust Depreciation Strategy

A structured depreciation approach improves accuracy and audit readiness. Businesses benefit from clear policies, reliable records, and regular asset reviews.

1. Conduct an asset audit

A physical inventory confirms what assets exist, where they are located, and their condition. This information forms the foundation of a reliable asset register.

2. Set capitalisation rules

A capitalisation threshold prevents low-value items from being tracked unnecessarily. Clear rules reduce administrative workload and improve consistency.

3. Categorise assets

Grouping assets allows finance teams to apply standard useful lives and methods. This approach improves comparability and reporting accuracy.

4. Use asset management software

Dedicated software reduces manual errors and automates calculations. It also improves audit trails and speeds up reporting cycles.

5. Perform regular verifications

Routine asset checks keep records accurate as assets move, break, or leave service. Adjustments should follow promptly when discrepancies arise. This process also supports condition-based asset care, where maintenance aligns with actual asset condition.

Common Pitfalls in Fixed Asset Depreciation

Even experienced finance teams encounter depreciation challenges. Awareness of common errors helps businesses avoid costly misstatements.

1. Ghost assets

Assets that no longer exist but remain on the ledger inflate asset values. Regular audits help remove these entries and correct depreciation records.

2. Incorrect estimates

Poor useful life or salvage value estimates distort profit reporting. Businesses should review assumptions regularly to maintain accuracy.

3. Policy inconsistency

Changing depreciation methods without valid justification raises audit concerns. Companies should apply methods consistently and document any changes.

4. Ignoring impairment

Unexpected events can sharply reduce asset value. Businesses must recognise impairment promptly to avoid overstated balance sheets.

Advanced Practices in Depreciation Management

As companies grow, depreciation management becomes more complex. Advanced practices improve precision, compliance, and strategic insight.

Component depreciation improves accuracy by depreciating asset parts separately. For example, different building components wear at different rates, which affects replacement planning and cost allocation.

Managing separate records for financial and tax depreciation allows businesses to meet reporting requirements while optimising tax outcomes. This approach requires careful reconciliation and strong controls.

Integrating depreciation with enterprise systems improves data accuracy and visibility. In an ERP system, depreciation schedules are configured once and run automatically each period.

The system applies the selected method, updates the asset register, and posts journal entries without manual input. It ensures asset records update automatically and support real-time financial insights.

Sustainability initiatives also affect depreciation planning. Incentives for energy-efficient assets influence investment decisions and long-term financial modelling.

Conclusion

Fixed asset depreciation helps businesses maintain accurate financial records while supporting long-term planning. When applied consistently, it improves reporting clarity, tax efficiency, and asset lifecycle management.

Frequently Asked Question

Yes. A business may revise useful life or residual value when justified, applying changes prospectively with proper documentation.

Depreciation does not reduce cash directly. It adjusts reported profit while improving visibility into operating cash flow.

Yes. Fully depreciated assets remain on the balance sheet until disposal or write-off.

Depreciation assumptions should be reviewed at least annually to ensure they remain accurate.