FIFO, or first in first out, is one of the most widely used inventory valuation methods in business, assuming the oldest stock is sold or used before newer items reach customers or production lines.

In accounting terms, FIFO assigns the cost of the oldest inventory to the cost of goods sold first, leaving newer, often higher costs sitting in ending inventory on the balance sheet.

For businesses managing perishables, fast-moving consumer goods, or any operation where inflation and supply costs shift over time, FIFO directly shapes profit margins, tax liabilities, and asset valuation.

Key Takeaways

FIFO is an inventory method where the oldest stock and its cost are recognised first when goods are sold or used.

Compared with other methods, FIFO produces clearer cost trails, higher profits during inflation, and inventory values close to current market prices.

Implementing FIFO involves auditing current stock, reorganising warehouse layout, configuring inventory software, and training warehouse and finance staff.

Best practices include accurate batch records, regular physical-to-system reconciliations, automation through ERP software, and ongoing monitoring.

What Is FIFO (First In, First Out)?

FIFO, or first in first out, is an inventory valuation and management method where the first goods purchased or produced are the first ones to be sold, consumed, or shipped out.

Under this approach, the oldest stock is prioritised for fulfilment, so the inventory remaining on hand at the end of an accounting period is composed of the most recently acquired goods.

A grocery store stocking milk illustrates the principle clearly, with employees placing newest cartons at the back of the shelf and pushing older cartons to the front so customers grab the oldest stock first.

This rotation prevents spoilage and minimises waste, but the principle extends well beyond perishables, serving as a foundational rule for financial accounting across virtually every industry that holds inventory.

In accounting, FIFO dictates how costs are assigned to inventory when it is sold, particularly when supplier prices shift over time due to inflation, exchange rates, or input cost changes.

When a sale occurs, the system assigns the cost of the oldest batch to the goods sold, regardless of which physical item the customer actually receives, creating a transparent and auditable cost trail.

Understanding the dual nature of FIFO, the physical rotation of stock and the financial assumption of cost flow, is the first step toward mastering inventory valuation in a modern business.

How FIFO Shapes Financial Results

The choice of inventory valuation method is not just a bookkeeping exercise; it is a strategic financial decision that flows through the income statement, balance sheet, and cash flow statement.

FIFO produces specific, predictable effects on financial reporting, particularly when viewed through the lens of changing macroeconomic conditions such as inflation, deflation, or sudden cost shifts.

1. Impact on profit margins

Gross profit is calculated by subtracting COGS from total revenue, so the inventory valuation method heavily influences reported profitability for any business holding inventory across periods.

Because FIFO typically assigns the oldest, lowest costs to COGS in an inflationary environment, the resulting COGS figure is minimised and gross profit is maximised on the income statement.

Higher gross profit cascades down through operating profit and net income, which boosts earnings per share for publicly traded businesses and improves headline performance reported to investors.

Because executive bonuses and incentives are often linked to profitability metrics, FIFO can create internal pressure to maintain robust margins, even when operational reality does not fully support the figures.

2. Effect during rising prices and inflation

The financial impact of FIFO is most pronounced during inflation or rising supplier costs, when the gap between historical inventory costs and current replacement costs widens significantly.

Under FIFO, the business continues to recognise the historical, cheaper costs on its income statement while selling goods at current, higher market prices, inflating the gross profit it reports.

This dynamic creates what accountants describe as inventory profits or phantom profits, where reported profit looks technically accurate but does not reflect the economic reality of replacement costs.

Higher reported profits also lead to higher taxable income, so a business using FIFO during inflation generally pays more income tax than one using a method matching current revenues with current costs.

3. Inventory value on the balance sheet

While the income statement reflects older costs under FIFO, the balance sheet benefits significantly because the ending inventory consists of the most recently purchased or produced goods.

The inventory asset value reported on the balance sheet therefore closely mirrors the current market value or replacement cost, giving stakeholders a more realistic picture of current asset positions.

This accurate valuation strengthens the balance sheet and improves liquidity ratios such as the current ratio, which divides current assets by current liabilities to gauge short-term solvency for the business.

Creditors and lenders pay close attention to these ratios when evaluating creditworthiness, and a robust inventory valuation can directly increase a business’s borrowing capacity or improve loan terms.

FIFO in Day-to-Day Operations

Translating FIFO from theory into practical, day-to-day operations requires careful planning, the right equipment, and robust processes that ensure physical stock rotates correctly across the warehouse floor.

Aligning operational reality with financial reporting also requires discipline and technology, because gaps between physical movement and digital records create reporting errors and inaccuracies over time.

1. Stock rotation in warehouses

Implementing an effective stock rotation system on the warehouse floor often dictates the layout and design of the facility, requiring infrastructure that makes the oldest stock easy to identify and retrieve.

Pallet flow racks and carton flow racks are common solutions, using gravity-fed systems where new inventory loads at the back and pallets glide forward as items are picked from the front.

This forces warehouse workers to pick the oldest items first, automating the physical FIFO process and removing the temptation to grab whatever pallet is closest at the loading face.

For bulk storage or floor stacking, clear aisle markings and strict procedures keep forklift operators digging into older stock instead of pulling from the most accessible recent pallets.

Proper labelling is also critical, with every batch of received goods marked with receipt dates, lot numbers, or colour-coded tags that instantly communicate inventory age to floor staff during picking.

2. Managing perishable and time-sensitive goods

For industries dealing with perishables such as food, pharmaceuticals, and cosmetics, the FIFO principle often shifts to expiry-based stock rotation such as FEFO.

While FIFO uses the date goods were received, FEFO uses the printed expiration or best-before date, which becomes the controlling factor when managing inventory with strict shelf life requirements.

Most of the time, the first goods received are also the first to expire, making the two concepts interchangeable in practice across the majority of normal supply chain conditions.

However, supply chain anomalies can produce a newer shipment with an earlier expiration date than older stock already in the warehouse, and managing by expiration date prevents selling spoiled goods.

Time-sensitive goods also require rigorous batch tracking and lot control, because a defective batch must be traceable through every finished product and every shipment that reached customers.

3. Aligning physical and system records

The greatest challenge in modern inventory management is keeping the physical reality of the warehouse perfectly aligned with the digital records held in the accounting and inventory systems.

Discrepancies between the two cause stockouts, overstocking, inaccurate financial reporting, and operational chaos that compounds over time if reconciliations are not performed regularly.

Businesses use an automated inventory records platform with barcode scanners, RFID tags, and automated data capture to record inventory movements in real time.

When a worker scans a pallet on receipt, the system logs date, time, and cost, then triggers the accounting system to recognise the right COGS based on the chronological FIFO queue at picking.

Integrated platforms that connect warehouse management directly to financial accounting modules ensure every physical scan automatically updates the ledger, removing the need for manual reconciliation work.

Comparing FIFO with Other Cost Methods

To fully understand the strategic value of FIFO, evaluate it against its main alternatives, because the choice of inventory valuation method shapes a business’s financial narrative for years.

| Aspect | FIFO | LIFO | Weighted Average |

|---|---|---|---|

| Cost flow assumption | Oldest costs assigned to COGS first | Newest costs assigned to COGS first | Average cost applied to all units sold |

| Effect during inflation | Lower COGS, higher reported profit | Higher COGS, lower reported profit | Smoothed COGS, moderate profit |

| Balance sheet inventory | Close to current market value | Outdated historical cost | Blended average value |

| Tax impact during inflation | Higher taxable income | Lower taxable income (US only) | Moderate taxable income |

| Allowed under IFRS | Yes | No | Yes |

| Allowed under Australian Accounting Standards | Yes | No | Yes |

| Best suited for | Perishables, FMCG, electronics, fashion | US-based tax-driven businesses | Volatile commodity markets |

| Audit trail clarity | Clear chronological trail | Complex layered tracking | Single average per period |

Each method has different strengths, weaknesses, and tax implications, and matching the method to your business model is more important than picking the most popular option for its own sake.

1. FIFO vs LIFO in cost recognition

The most direct contrast to FIFO is LIFO, or last in first out, which assumes the most recently acquired inventory is sold first and assigns those newest costs to the cost of goods sold.

From an income statement perspective, LIFO matches current revenues with current costs, giving a more accurate reflection of profitability and addressing the matching principle issue inherent in FIFO.

During inflation, LIFO assigns the highest, most recent costs to COGS, which lowers reported profit and reduces income tax liability, making it attractive for businesses focused on tax deferral strategies.

However, LIFO distorts the balance sheet by valuing ending inventory at the oldest, often outdated costs, and is prohibited under International Financial Reporting Standards used in over 140 jurisdictions.

2. FIFO vs weighted average cost method

The weighted average cost method calculates an average cost per unit by dividing the total cost of goods available for sale by the total units, then applies that average to both COGS and ending inventory.

This method smooths out price fluctuations and produces more stable margins, which is useful for businesses operating in volatile commodity markets where input prices swing sharply within a single period.

FIFO retains separate cost layers and produces more granular tracking, while weighted average loses the chronological detail in exchange for simplicity and consistency across the inventory pool.

Weighted average is permitted under both IFRS and GAAP, making it a workable alternative for businesses that want compliance flexibility without the historical-cost mismatch issues affecting FIFO.

3. Advantages of using FIFO

FIFO matches the natural physical flow of goods in most businesses, because companies generally want to sell oldest stock first to minimise obsolescence, spoilage, or damage from extended storage.

In food, pharmaceuticals, cosmetics, and fast-moving consumer goods, selling oldest items first is a regulatory requirement, so FIFO accounting mirrors what operations teams are already doing.

FIFO also produces a transparent, easily auditable trail because the chronological tracking of purchases leaves a clear sequence of cost assignments that auditors can verify against purchase invoices.

Compared with LIFO, FIFO is also less open to manipulation because management has less leeway to choose which costs to recognise, which builds trust with investors, lenders, and tax authorities.

4. Limitations of FIFO

The most significant criticism of FIFO is that it violates the matching principle, which states expenses should be recognised in the same period as the revenues they helped generate.

Under FIFO during inflation, current high revenues match with historical low costs, distorting gross profit margins and making the business appear more profitable than current economics actually support.

FIFO can also produce erratic results in industries with extreme price volatility such as oil, lumber, agricultural commodities, or precious metals, where input costs swing sharply within short periods.

FIFO is also unsuitable for businesses selling unique, high-value, non-fungible goods such as fine art, custom jewellery, or bespoke machinery, where the Specific Identification method is far more accurate.

5. Choosing the right method for your business

The right inventory valuation method depends on the type of products sold, the rate at which prices change, the regulatory environment, and the business’s strategic priorities around tax and reporting.

Businesses with perishable goods, regulatory shelf-life requirements, or fast-rotating inventory typically benefit most from FIFO because it aligns physical and accounting flows in a single, auditable framework.

Businesses operating in highly volatile commodity markets often prefer the weighted average cost method, while those with unique items default to Specific Identification for accuracy on a per-item basis.

Whatever method is chosen, businesses should apply it consistently across reporting periods, since switching valuation methods triggers disclosure requirements and may distort comparability of financial statements.

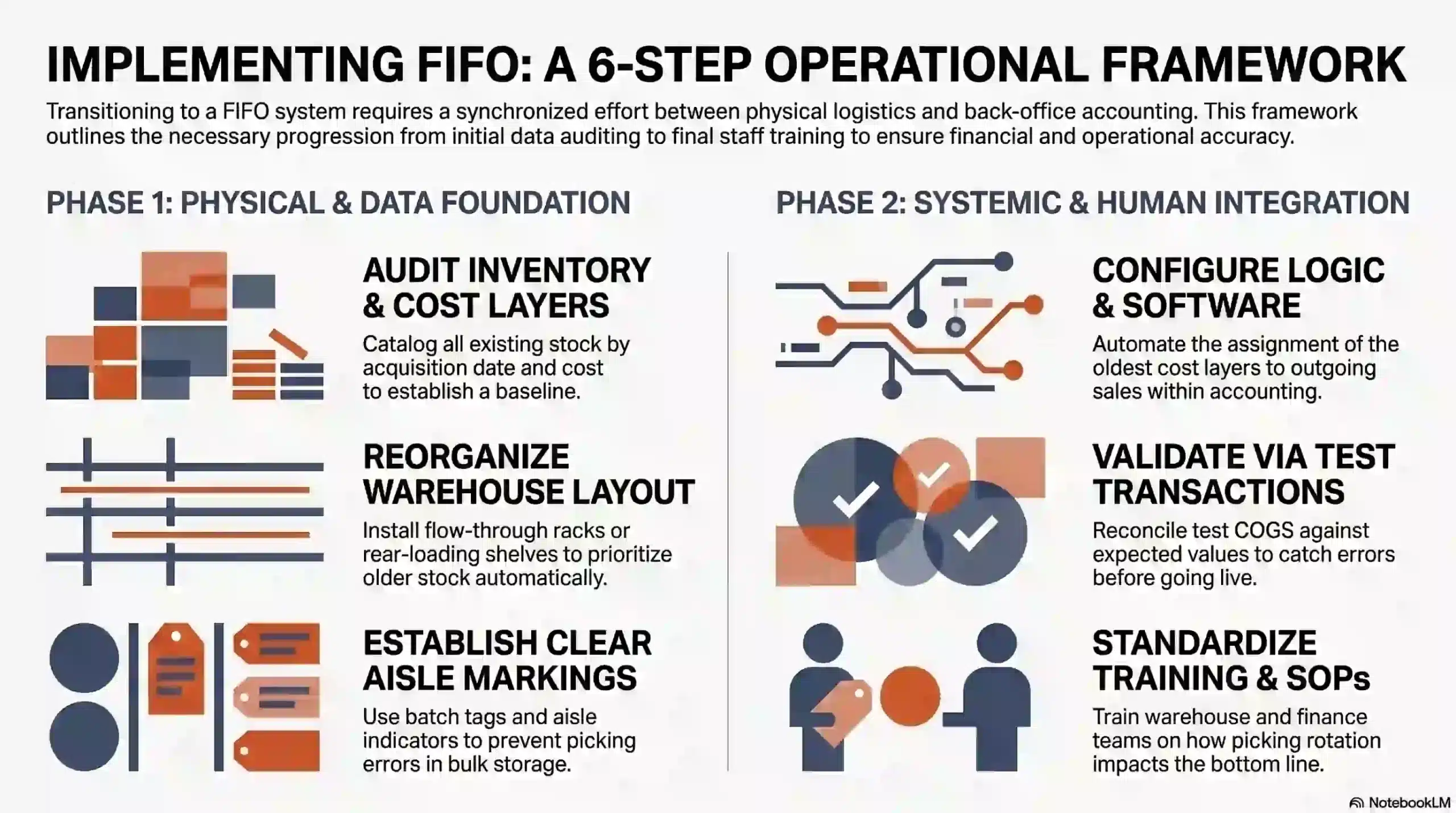

Implementation of FIFO in Your Business

Transitioning to a strict FIFO system requires coordinated effort between physical warehouse management and back-office accounting, with clear sequencing across infrastructure, software, and people.

Each step builds on the previous one, so skipping ahead to software configuration without first auditing existing stock or aligning warehouse layout creates errors that surface during reconciliation.

1. Audit current inventory and cost layers

Begin by cataloguing all existing stock, noting acquisition dates, lot numbers, and historical purchasing costs to establish an accurate financial baseline before any FIFO logic is applied.

Without an accurate starting point, the FIFO cost flow cannot produce correct COGS or ending inventory values, so the audit must capture every batch held in storage at the cutover moment.

2. Reorganise warehouse and storage layout

Physically arrange storage areas to naturally facilitate FIFO picking, with flow-through pallet racks or rear-loading shelving ensuring older stock is always at the picking face for warehouse staff.

Floor stacking and bulk storage need clear aisle markings, batch tags, and standard procedures so workers cannot pick the most accessible pallet without considering its position in the FIFO queue.

3. Configure inventory and accounting software

Configure stock control software in Australia and accounting systems to assign the oldest cost layers to outgoing sales automatically, regardless of physical movement, so the cost flow assumption stays consistent.

Validate the configuration by running test transactions through the system and reconciling the resulting COGS against expected values, catching errors before they affect live financial reporting.

4. Train warehouse and finance staff

Update standard operating procedures and run training sessions so warehouse staff understand why prioritising older stock matters and what happens financially when picking rotation is bypassed.

Finance teams also need refresher training on how the FIFO cost layers feed into COGS and ending inventory, particularly during high-volume periods or when external auditors review the books.

Best Practices for FIFO Management

Effective FIFO management depends on consistent processes, clean data, and the right software, with each component reinforcing the others to keep both physical and financial records accurate over time.

Treating FIFO as an ongoing discipline rather than a one-off implementation is what separates businesses that maintain accurate margins from those that drift into reporting errors as conditions change.

1. Maintain accurate batch and cost records

Keep detailed records of every batch including receipt date, supplier, quantity, unit cost, and lot number, because the FIFO cost flow depends entirely on the accuracy of these foundational data points.

Inaccurate batch records compound silently, so a single missing entry can throw off cost layer assignment for months until reconciliation surfaces the discrepancy and forces a manual investigation.

2. Run regular physical-to-system reconciliations

Schedule periodic stock counts and compare them against system record and compare them against system records monthly or quarterly, because timing differences, miscounts, or unrecorded movements always emerge between the two over time.

Reconciliation is also when FIFO logic is stress-tested, since any picking that bypassed older stock shows up as discrepancies between the system’s cost layers and the actual inventory still on the floor.

3. Automate cost layer assignment with inventory or ERP software

Inventory or ERP software designed for FIFO automates cost layer assignment, applying the oldest cost first to every sale and updating the ending inventory value without manual intervention from finance staff.

Integrated platforms also connect inventory data with general ledger postings, so the same cost flow assumption flows from receipt through sale to financial reporting without duplicate data entry.

4. Track FIFO performance against business outcomes

Monitor inventory turnover, dead stock rates, and gross margin variance to confirm FIFO is delivering the intended outcomes rather than producing reporting figures disconnected from operational reality.

Regular reviews also surface when FIFO no longer suits the business, such as when input prices become highly volatile and a switch to weighted average might better match operations to reporting.

Conclusion

FIFO is one of the most widely used inventory valuation methods because it aligns physical stock movement with financial reporting in a transparent, auditable way that meets global accounting standards.

Successful FIFO management depends on consistent batch tracking, regular physical-to-system reconciliations, and software automation that holds the chronological cost layers stable as the business grows.

If you want to bring FIFO discipline to your warehouse and accounting workflows, you can schedule a free consultation with our expert to optimise your inventory system.

FAQ About First In First Out (FIFO)

-

Is FIFO required by law in Australia?

FIFO is not legally required in Australia, but it is the most common inventory valuation method used by Australian businesses because it aligns with International Financial Reporting Standards.

-

Why is LIFO not allowed under Australian Accounting Standards?

LIFO is prohibited under International Financial Reporting Standards, which form the basis of Australian Accounting Standards, because it valuates ending inventory at outdated costs that distort the balance sheet.

-

Can a business switch between FIFO and another inventory method?

Yes, but switching valuation methods requires disclosure under Australian Accounting Standards, restated comparative figures, and a clear business reason, so most businesses commit to a single method consistently.

-

How does FIFO affect tax in Australia?

Under FIFO, older costs flow to COGS first, increasing reported profits and taxable income during inflation. Australian businesses generally pay more income tax under FIFO than under methods that match current revenue.

-

Which industries use FIFO most often?

Industries dealing with perishable goods, fast-moving consumer products, pharmaceuticals, cosmetics, fashion, and consumer electronics rely on FIFO most because their products risk spoilage, expiry, or obsolescence.