Construction isn’t like most industries. Every project is unique, timelines stretch over months, and costs can change quickly. No wonder standard bookkeeping often falls short and construction accounting becomes essential.

The Australian Bureau of Statistics reports that the construction sector generates over A$633 billion in income. It’s clear that without proper financial control, even one bad project can put an entire business at risk.

In this guide, we’ll break down the key insights you need to manage construction finances effectively. You’ll also see how the right construction administration tools can help you stay in control and run a more efficient operation.

Key Takeaways

Construction accounting is a project-based financial framework that tracks costs, revenue, and profitability across each job.

The components of construction accounting includes job costing, WIP reporting, progress billing, and precise cost categorization across labor, materials, and overhead.

Best practices for construction accounting include real-time cost tracking, accurate coding, and consistent use of purpose-built systems.

Implementing a construction-specific system requires auditing current processes, standardizing cost codes, and running parallel testing before full migration.

What Is Construction Accounting?

Construction accounting is a specialised financial framework designed for project-based work. It tracks costs, revenue, and profitability at the individual project level rather than across the entire business.

It covers job costing, payroll across multiple sites, subcontractor payments, and revenue recognition. This level of detail ensures financial data reflects actual project performance.

Accurate construction accounting also supports external requirements such as financing, bonding, and compliance. Without it, businesses struggle to maintain cash flow and secure larger projects.

How Construction Accounting Differs from Traditional Accounting

Construction accounting differs significantly from traditional accounting. While industries like retail rely on immediate transactions and stable costs, construction operates on long-term, project-based work with shifting expenses.

Projects run across multiple sites, costs change over time, and overhead must be allocated across concurrent jobs. These conditions create distinct financial challenges that require a different accounting approach.

1. Project-based financial tracking

Construction accounting tracks performance at the project level, where each job has its own budget, timeline, and cost structure. This differs from traditional models that rely on company-wide tracking.

Each cost must be assigned to a specific project and phase. This allows businesses to monitor profitability per job and identify issues before they impact overall financial performance.

2. Long-term contract revenue recognition

Unlike traditional accounting, revenue in construction is recognised over time rather than at a single transaction point. This reflects how projects are delivered across extended periods.

The percentage of completion method aligns revenue with project progress. It provides a more accurate financial picture, but depends heavily on precise cost tracking and forecasting.

3. Managing multiple projects simultaneously

Construction companies often run several projects at once, each with different timelines, costs, and resource demands. This creates more complex financial management compared to stable operations.

Overhead and cash flow must be tracked per project to avoid imbalance. Without proper separation, businesses risk using funds across projects in ways that create financial instability.

To understand better, see this table below.

| Aspect | Construction accounting | Traditional accounting |

| Tracking | Project-based | Company-wide |

| Revenue | Progress-based | Point of sale |

| Cost allocation | Per project | General allocation |

| Cash flow | Multiple project streams | Single flow |

Core Components of Construction Accounting

Construction accounting relies on several core components to make project-based tracking and long-term revenue recognition work in practice. These are the building blocks that turn raw field data into financial clarity for project managers and executives alike.

1. Job costing and project budgeting

Job costing tracks all expenses against a project’s budget. Each cost is assigned to a defined category, helping teams monitor spending throughout the project lifecycle.

This structure allows managers to detect cost variances early. Accurate tracking supports better control over margins and prevents small overruns from escalating.

2. Work in progress (WIP) reporting

WIP reports provide a snapshot of project financial status, including costs, billings, and recognised revenue. They help identify whether a project is over-billed or under-billed.

These insights are essential for managing cash flow and financial risk. Regular updates ensure that reporting reflects actual project progress.

3. Progress billing and retention

Construction billing is based on project progress rather than full completion. Contractors submit staged invoices aligned with work completed.

Retention adds another layer, where a portion of payment is withheld until project completion. This requires careful tracking to maintain accurate cash flow visibility.

4. Cost categories: labor, materials, and overhead

Construction costs are divided into direct costs and overhead. Labour and materials are tied to specific projects, while overhead supports overall operations.

Clear categorisation ensures accurate reporting and fair cost allocation. This helps maintain consistency across multiple projects.

Financial Reporting in Construction Projects

Financial reporting turns construction data into actionable insights. Without it, job costing and data collection provide limited value.

While standard reports support compliance, project-level reporting drives daily decisions by reflecting real-time performance across active jobs.

1. Project cost reports

Project cost reports track budgets, actual costs, and committed expenses. They provide a clear view of financial performance at the project level.

Including committed costs ensures future obligations are considered. This prevents overspending and improves financial accuracy.

2. Budget vs actual analysis

This analysis compares planned budgets with actual costs and forecasts remaining expenses. It helps assess whether a project is on track financially.

Metrics like estimate at completion (EAC) highlight potential losses early. This allows teams to adjust strategies before issues escalate.

3. Profitability tracking by project

Profitability tracking evaluates performance across multiple projects. It helps identify which projects or segments generate stronger margins.

This insight supports better decision-making and resource allocation. Businesses can focus on more sustainable and profitable work.

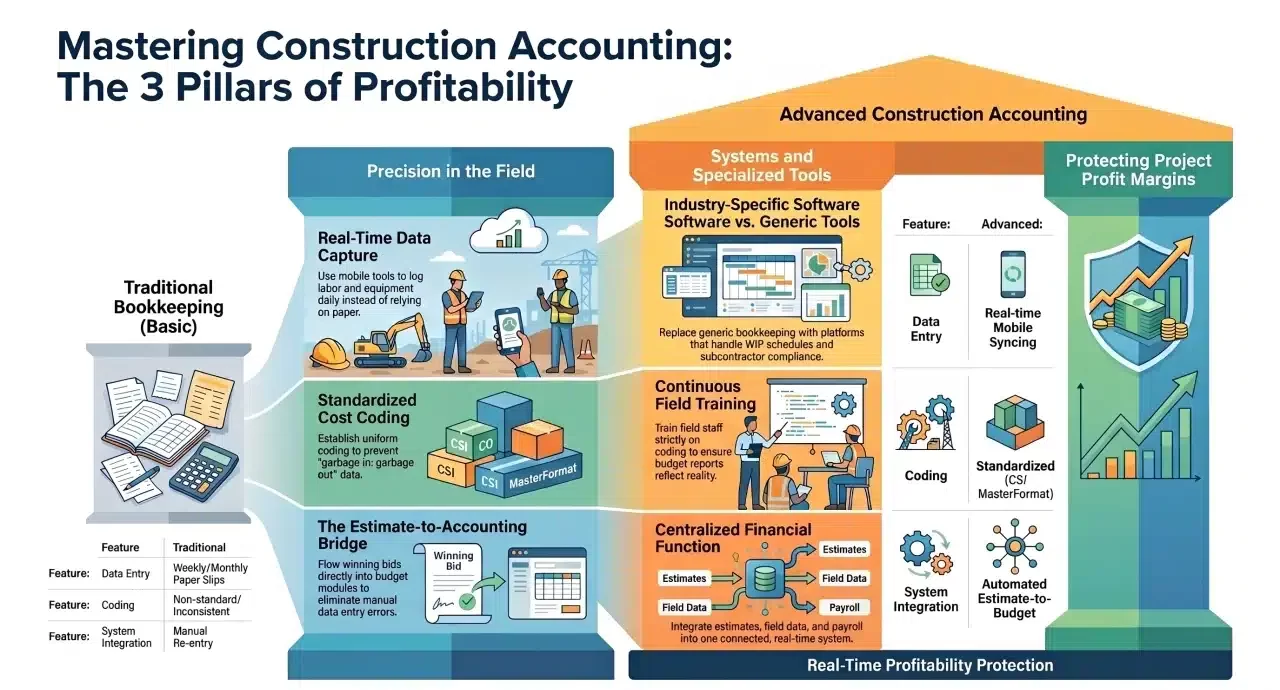

Best Practices for Effective Construction Accounting

Moving from basic bookkeeping to advanced construction accounting takes real commitment. It requires process discipline and the use of construction administration tools to maintain consistency across projects.

Contractors who consistently hit strong profit margins do not get there by accident. They follow a strict set of financial best practices that run from the field worker all the way up to the CFO.

1. Track project costs in real time

Real-time tracking ensures cost data reflects current site activity. Delayed input reduces accuracy and limits decision-making effectiveness.

Using digital tools allows teams to capture data directly from the field. This improves visibility and helps prevent cost overruns.

2. Use accurate job costing methods

Consistent cost coding is essential for reliable reporting. Without it, financial data becomes fragmented and harder to interpret.

Standardised structures ensure all departments follow the same framework. This improves data quality and supports better analysis.

3. Implement construction accounting software

Generic systems often lack the features needed for project-based accounting. Using software for constructors helps centralise job costing, reporting, and compliance processes.

The right system improves accuracy and reduces manual work. It also ensures financial data keeps pace with project activity.

Implementation Steps for Construction Accounting Systems

Transitioning to a specialized financial framework or upgrading to a construction financial software requires a methodical, phased approach to ensure success:

- Conduct a Financial Audit: Identify current reporting gaps, workflow bottlenecks, and areas where data silos exist between the field and the office.

- Select Industry-Specific Software: Choose a platform that natively supports robust job costing, WIP reporting, and union payroll rather than trying to customize generic accounting software.

- Standardize Cost Codes: Develop a uniform set of cost codes (such as CSI MasterFormat) across the entire business to ensure historical data consistency and accurate estimating.

- Parallel Testing and Migration: Execute a controlled data migration, running the legacy system and the new platform in parallel for at least one billing cycle to catch discrepancies.

- Comprehensive Training: Invest heavily in training not just for the accounting department, but also for project managers and field superintendents who will be inputting raw data.

Common Pitfalls to Avoid

Even with the right system, errors often come from execution rather than tools.

- Failing to connect field and office data: This delays reporting and leads to decisions based on outdated information.

- Poor change order management: Performing work without approval reduces profitability and creates billing issues.

- Not updating WIP regularly: This results in inaccurate revenue reporting and potential cash flow problems.

- Mixing project cash flow: Using funds across projects increases financial risk and reduces control.

Conclusion

Construction accounting is the financial backbone of every project a contractor takes on. Firms that treat it as a priority consistently protect their margins, maintain healthy cash flow, and build the credibility needed to land bigger work.

The principles in this guide, from job costing to real-time tracking and change order discipline, are not reserved for large contractors. Any contractor willing to invest in the right tools and commit to sound financial habits can build a business that survives volatility and grows with confidence.

Managing your own construction accounting process is complex work that carries many risks when done improperly. If you have this concern, then you can apply for a free consultation with our team so we can help you understand everything you need to change for your business to thrive even more.

Frequently Asked Question

Construction accounting uses project-based accounting, where each project is treated as a separate financial unit with its own costs, revenue, and profitability tracking.

Construction expenses are recorded through job costing, assigning each cost to a specific project and category such as labour, materials, or overhead.

Construction accounting is complex because projects are long-term, costs fluctuate, and revenue must be recognised progressively rather than at a single point.

A common rule of thumb is to monitor cost-to-complete regularly and maintain profit margins by identifying and addressing cost variances early.