Every financial transaction your business makes needs to be recorded somewhere. That’s what a journal entry does. It’s the foundation of accurate bookkeeping, and without it, your financial statements won’t balance.

In 2024, manual data entry error rates ranged from 1% to 5% (DocuParser, 2024). For businesses handling hundreds of transactions a month, those errors stack up quickly. Getting journal entries right from the start stops mistakes from spreading through your books.

This guide covers what journal entries are, how they work, the different types, real examples including how to record GST, and how software takes most of the manual work off your plate.

Key Takeaways

A journal entry records every financial transaction using debits and credits, helping keep financial records accurate and balanced.

Every journal entry follows the double-entry accounting system, where total debits must always equal total credits.

Businesses use different types of journal entries including simple, compound, adjusting, opening and closing, and reversing entries.

Modern accounting software can automate journal entries, GST calculations, recurring transactions, and audit trails.

What Is a Journal Entry?

A journal entry is the record of a financial transaction in your accounting system. It captures what happened, which accounts were affected, and by how much. Double-entry bookkeeping has been the global standard for over 800 years, first documented by Luca Pacioli in 1494 (QuickBooks, 2024).

Every entry needs five things: the transaction date, a reference number, the account names, the debit and credit amounts, and a short narration explaining what it was.

Think of it as a logbook. Nothing shows up on your balance sheet or P&L until it’s been recorded here first.

How Journal Entries Work

Getting journal entries right comes down to two things: knowing how debits and credits behave, and making sure every entry balances.

1. Debits and Credits Explained

Debits and credits don’t mean “increase” and “decrease”. They mean left and right in the T-account system. Whether a debit adds to or reduces an account depends on the account type.

Assets and expenses go up with a debit. Liabilities, equity, and revenue go up with a credit. So when you pay rent, you debit Rent Expense and credit Cash. The expense goes up, the cash goes down.

Once that pattern clicks, most entries become second nature.

2. The Double-Entry Rule

Every journal entry must balance. Debits always equal credits, no exceptions. This is what keeps the accounting equation (Assets = Liabilities + Equity) intact.

Buy $5,000 of equipment on credit? Equipment is debited $5,000 and Accounts Payable is credited $5,000. Both sides move, both sides balance.

What to Include in a Journal Entry

In 2024, around 60% of small business owners said they felt unsure about core accounting practices (6W Research, 2024). Incomplete journal entries are one of the most common and avoidable gaps.

A proper entry needs six things: the transaction date, a reference number, account names from your chart of accounts, the debit amount, the credit amount, and a narration of what happened.

The ATO requires financial records to be kept for at least five years. For GST transactions, always record the GST on a separate line rather than in a gross total, so your BAS stays correct.

Types of Journal Entries

Understanding the main types helps ensure transactions are recorded accurately and financial reports remain reliable.

1. Simple and Compound Entries

Simple entries involve one debit and one credit account, making them the most common type of journal entry. Compound entries affect three or more accounts and are often used for transactions involving GST, payroll, or multiple expenses.

2. Adjusting Entries

Adjusting entries are made at the end of an accounting period to ensure income and expenses are recorded in the correct period. Common examples include depreciation, accrued expenses, and prepaid expenses.

3. Opening, Closing, and Reversing Entries

Opening entries carry balances forward into a new financial year, while closing entries transfer revenue and expense balances into retained earnings. Reversing entries are optional entries used to reverse certain accruals and prevent duplicate transactions in the following period.

Journal Entry Examples

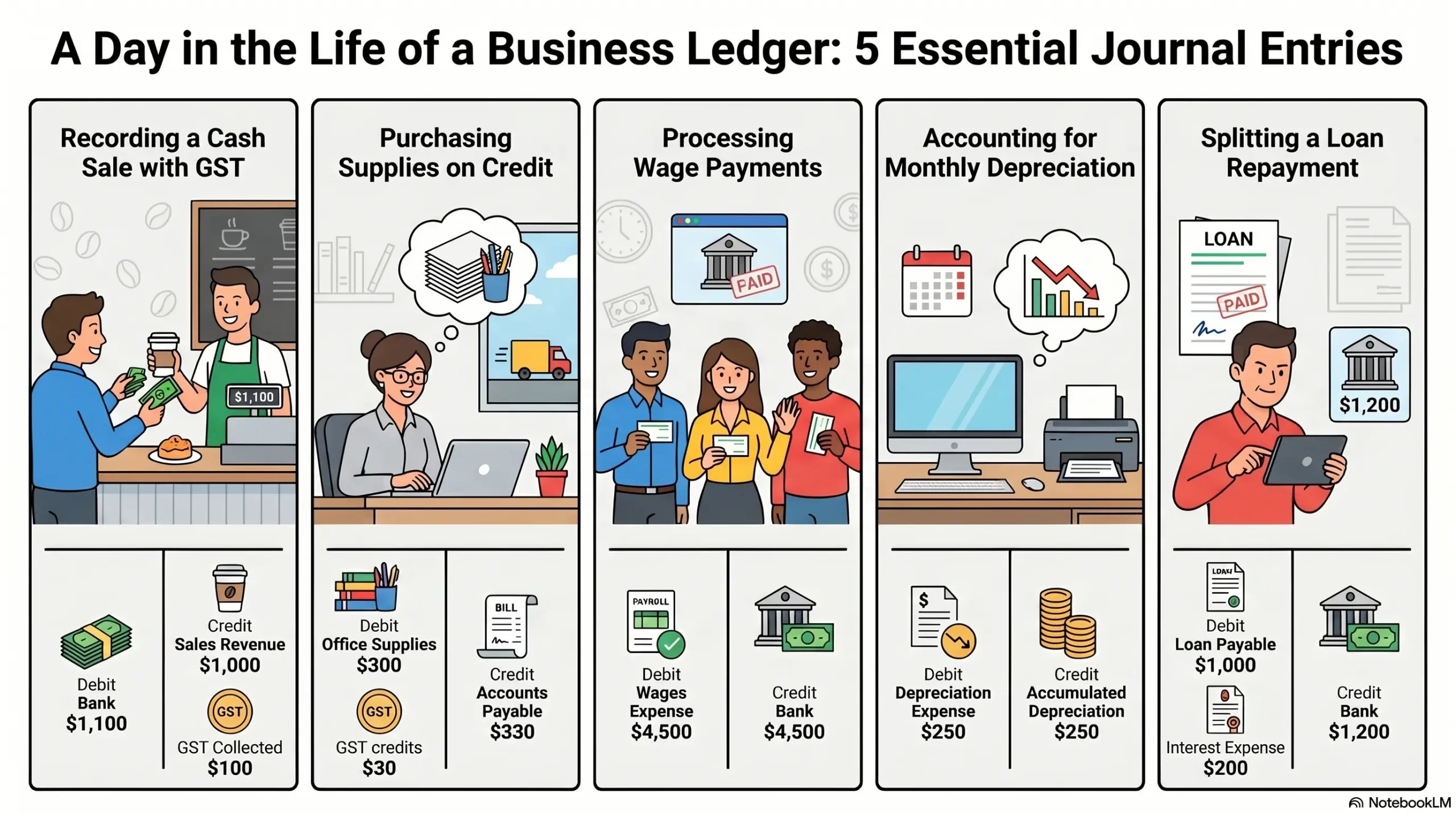

Here are five entries that Australian businesses deal with regularly. The debit is always listed first.

- Cash Sale with GST: You sell products for $1,100 including $100 GST. Debit Cash/Bank $1,100, credit Sales Revenue $1,000 and GST Collected $100. Revenue stays clean and the GST liability is tracked on its own line.

- Credit Purchase with GST: You buy $330 of supplies on credit, including $30 GST. Debit Office Supplies $300 and GST Input Tax Credit $30, then credit Accounts Payable $330. That Input Tax Credit is claimable on your BAS.

- Wage Payment: You pay $4,500 in wages. Debit Wages Expense $4,500, credit Cash/Bank $4,500. If PAYG withholding applies, add a separate PAYG Payable credit line.

- Monthly Depreciation: Equipment depreciates $250 per month. Debit Depreciation Expense $250, credit Accumulated Depreciation $250. This gradually reduces the asset’s net book value on the balance sheet.

- Loan Repayment: A $1,200 monthly repayment splits into $1,000 principal and $200 interest. Debit Loan Payable $1,000 and Interest Expense $200, then credit Cash/Bank $1,200. Always separate these two, as they land in different parts of your financial statements.

Common Journal Entry Mistakes to Avoid

Even small journal entry mistakes can affect your financial reports, tax calculations, and reconciliation process. Understanding the most common errors can help keep your records accurate and easier to manage.

1. Incorrect Account Entries

Posting transactions to the wrong accounts or reversing debits and credits can lead to inaccurate financial reports. Consistently using your chart of accounts helps reduce these errors.

2. GST and Duplicate Entry Errors

Failing to separate GST correctly may affect BAS reporting and cause missed Input Tax Credits. Duplicate entries can also occur when transactions are entered manually and imported from bank feeds.

3. Skipping Reconciliation

Closing a period without reconciling accounts can leave errors undetected. Regular reconciliations help identify issues early and keep records accurate.

Journal Entry vs General Ledger

Journal entries and general ledgers are closely connected, but they have different purposes.

A journal entry records individual transactions as they happen. The general ledger then groups those entries by account and shows the running balance of each account.

Journal entries feed into the general ledger, which is then used to prepare financial reports. Recording entries promptly also helps businesses spot and fix errors before they become larger reconciliation issues.

How Accounting Software Automates Journal Entries

Modern accounting software reduces manual data entry by automating many journal entry tasks. Businesses using digital accounting tools often see improved accuracy and spend less time on administrative work.

Bank feeds automatically import transactions from your accounts, while recurring entries such as rent, depreciation, and loan repayments can be scheduled to post automatically.

For Australian businesses, GST calculations and BAS reporting are handled automatically. The software validates entries, maintains a complete audit trail, and helps finance teams focus more on analysis instead of data entry.

Conclusion

Journal entries are where all your financial reporting begins. Get them right and everything downstream, your BAS, balance sheet, and P&L, stays accurate.

The core rules are simple: every transaction touches at least two accounts, debits always equal credits, and a clear narration saves time later. The five entry types cover every scenario a business will face.

Accounting software handles the mechanics so your team can focus on what the numbers mean, not on entering them

Frequently Asked Question

A journal entry is the record of a financial transaction in an accounting system. It shows how a transaction affects different accounts using debits and credits.

The main types of journal entries are simple entries, compound entries, adjusting entries, opening and closing entries, and reversing entries.

A journal entry records an individual transaction, while the general ledger organises and summarises all journal entries by account.

GST is recorded separately from the transaction value. Typically, the transaction amount, GST component, and related account balances are recorded in the same journal entry.

Yes. Most modern accounting systems can automatically create journal entries from bank transactions, invoices, payroll, and recurring transactions.