A vendor invoice is a formal billing document issued by a supplier to request payment for goods or services delivered to a buyer. It records transaction details such as item costs, GST, payment terms, and supplier information to support accounts payable processing and financial tracking.

A vendor invoice template is a structured layout that gives Australian businesses a compliant, repeatable way to record every supplier bill received against goods and services purchased.

It captures supplier details, ABN, GST, line items, and payment terms in one document, helping accounts payable teams process bills faster, claim GST credits cleanly, and stay aligned with the ATO.

This article explains what a vendor invoice is, what Australian law requires it to contain, the steps to create one, common mistakes to avoid, and when to move beyond templates into automation.

Key Takeaways

Vendor invoice is the buyer's accounts payable record of a supplier bill, capturing items, GST, and payment terms in one structured commercial document.

Australian compliance for vendor invoices means meeting ATO rules on ABN, GST breakdown, the 'Tax Invoice' label, and record retention.

Vendor invoice template gives Australian businesses a free, ATO-aligned baseline with built-in GST formulas, ABN fields, and payment terms.

Steps to create a vendor invoice cover entering parties, itemising lines, calculating GST, setting payment terms, and reviewing accuracy.

What Is a Vendor Invoice?

A vendor invoice is a commercial document a supplier issues to a buyer, requesting payment for goods or services already delivered under agreed terms.

From the buyer’s perspective, the same document is recorded in the accounts payable ledger as a vendor invoice, providing a formal trail of the transaction and what is owed.

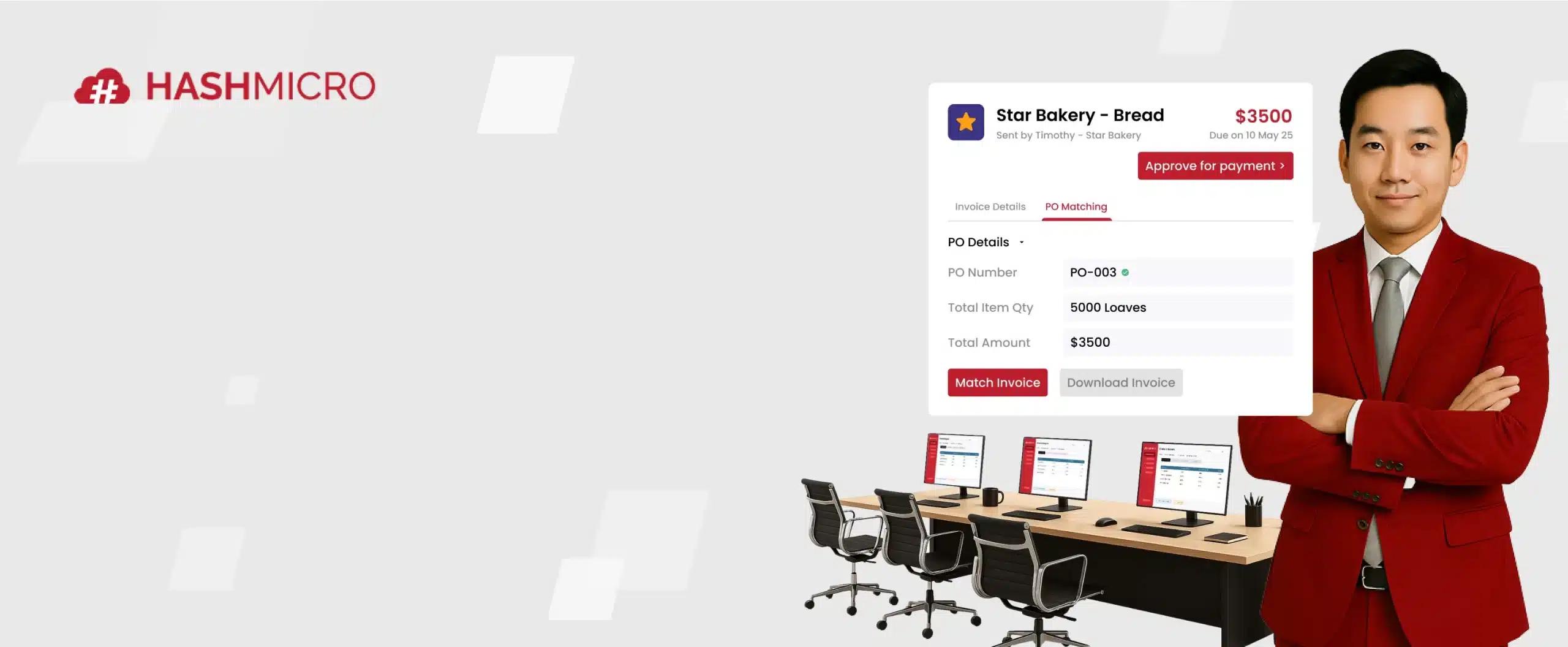

The document specifies quantities, unit prices, GST applied, and payment terms, giving both parties a clear reference if questions arise about delivery, pricing, or due dates later on. Before payment is issued, most businesses match the vendor invoice against the original purchase order and goods receipt to verify accuracy.

Vendor Invoice vs Customer Invoice

The physical document reflects the basic of invoicing; the terminology depends on which side of the transaction is reading it. Sender and recipient see the same paper, but record it under different ledger accounts.

A supplier issues a customer invoice to collect payment, treating it as an accounts receivable entry. The buyer receives that document as a vendor invoice and posts it to accounts payable.

Understanding this distinction matters for reconciliation and audit. Confused terminology can cause double entries, missed payments, or disputes when staff cannot tell which side of the ledger applies.

What Must a Vendor Invoice Include in Australia?

A compliant Australian vendor invoice contains specific data points required by the ATO and standard accounts payable practice. Missing fields can block GST credit claims and slow payment cycles.

The nine elements below cover the minimum required for tax invoices over $82.50 (GST inclusive), with extra rules applying once the invoice value passes the $1,000 threshold.

1. Supplier business name and contact details

The invoice must show the legal business name of the supplier exactly as registered, along with at least one contact detail, such as a physical address, phone number, or email.

Trading names alone are insufficient if they do not match the registered legal entity. ATO compliance requires the name on the invoice to align with the ABN it carries on the document.

2. ABN and tax invoice label

GST-registered suppliers must include their Australian Business Number (ABN) and label the document clearly as a “Tax Invoice” so the buyer can claim input tax credits through their BAS.

If the supplier is not registered for GST, they issue a regular invoice without GST. The “Tax Invoice” label is reserved exclusively for GST-registered businesses making taxable sales.

3. Invoice number and issue date

A unique invoice number prevents duplicate payments and provides a tracking reference across both supplier and buyer systems. Sequential numbering is the cleanest approach for clean audit trails.

The issue date determines when payment terms begin counting. A “Net 30” invoice issued on 1 May is due 31 May, regardless of when the buyer’s accounts payable team finally posts it.

4. Buyer details and delivery information

The buyer’s name, address, and ABN should appear on the invoice, especially for transactions above $1,000 where the ATO requires the recipient’s identity for valid GST credit support.

Delivery information confirms goods or services were sent to the correct location, helping the accounts payable team perform their three-way match against the original purchase order.

5. Description of goods or services

A clear, itemised breakdown of what was delivered allows accounts payable to verify each charge against the original purchase order and goods receipt note without ambiguity.

Vague descriptions like “professional services” without further detail often trigger approval delays. Aim for enough specificity that a non-technical reviewer can match the invoice to expected output.

6. Quantity, unit price, subtotal, and total amount

Each line item should display the quantity supplied, the agreed unit price, and the line subtotal. The cumulative subtotal across lines represents the cost before GST is applied.

The total amount is the subtotal plus GST. Showing each step transparently lets the buyer’s finance team verify the calculation rather than accept a single round figure on faith.

7. GST amount and tax breakdown

The invoice must either state the GST amount as a separate line or include a clear declaration that “the total price includes GST” so the buyer can identify the tax component.

Mixed supplies (some lines GST-applicable, some GST-free) must show the breakdown clearly. Generic statements obscure exempt items and complicate BAS reconciliation later.

8. Payment terms, due date, and payment method

Specify whether payment is Net 7, Net 14, Net 30, or another term, alongside the calculated due date. Vague language like “due on receipt” leaves room for interpretation and disputes.

Accepted payment methods (EFT, BPAY, credit card, direct debit) should be listed with the relevant bank account, BSB, BPAY biller code, or card processing instructions.

9. Extra requirements for invoices above AUD 1,000

Tax invoices for taxable sales of $1,000 or more must additionally show the buyer’s identity, address, or ABN. Without these details, the document does not support a valid GST credit claim.

This rule catches many small businesses by surprise. Even if every other field is present, an invoice over $1,000 missing the buyer’s identity is rejected for GST credit purposes.

Australian Compliance Requirements for Vendor Invoices

The Australian Taxation Office sets enforceable rules for what qualifies as a valid tax invoice. Falling short of these standards has direct consequences for both the buyer and the supplier.

Australian Bureau of Statistics data shows small and medium businesses generate most local invoice volume, making strict ATO compliance critical at every transaction value.

The five compliance areas below cover the most common requirements that apply to Australian businesses dealing with vendor invoices in the 2026 financial year.

1. ATO tax invoice requirements

For taxable sales over $82.50 including GST, the supplier must provide a valid tax invoice within 28 days of the buyer requesting it. Failure to do so blocks the buyer’s GST credit claim.

A valid tax invoice carries the words “Tax Invoice”, the supplier’s ABN, the issue date, a brief description of items sold, the GST amount, and the total price including GST.

2. ABN requirements on vendor invoices

When a supplier does not provide an ABN, the buyer may be required to withhold the top marginal tax rate (47%) from the payment and remit it directly to the ATO under no-ABN withholding rules.

This rule prevents tax avoidance through unregistered suppliers. Buyers who fail to withhold can be liable for the missed tax themselves, so confirming the ABN before payment is essential.

3. GST rules for vendor invoices

Only suppliers registered for GST can issue tax invoices and charge GST on taxable sales. Unregistered suppliers must issue a regular invoice without GST and without the “Tax Invoice” label.

GST is generally 10% on taxable supplies, with specific exemptions for fresh food, exports, and certain education and health services. The breakdown must be transparent on every invoice.

4. Invoice requirements for amounts above AUD 1,000

Tax invoices over $1,000 must additionally include the buyer’s identity, name, address, or ABN. This higher-value threshold reflects the larger GST credit risk if the document is challenged later.

Buyers should reject incomplete invoices over $1,000 and request a corrected version, rather than process payment and risk an ATO disallowance during BAS audit cycles.

5. Record-keeping requirements for Australian businesses

Australian law requires businesses to retain vendor invoice records for at least five years from the date the BAS or income tax return supported by the invoice is lodged.

Records can be paper or electronic, but must remain readable, secure, and easily retrievable on ATO request. Cloud-based ERP systems satisfy this requirement automatically.

Free Vendor Invoice Template for Australia

A standardised vendor invoice template gives Australian businesses a baseline that includes every ATO-mandated field, reducing the chance of compliance errors at the document creation stage.

The template below is available as a free downloadable Excel file with built-in formulas for GST and totals, plus pre-set fields for ABN, payment terms, and supplier identification.

EOFY Financial Analysis Report Template

It works for sole traders, Pty Ltd companies, and partnerships. Customise the supplier details, branding, and line items to match your business, then save it as a master copy for repeat use.

5 Steps to Create a Vendor Invoice

Creating a vendor invoice consistently and accurately depends on a repeatable workflow. The five steps below cover the core actions from data entry through final review.

Following them in order reduces formatting errors, missed compliance fields, and disputes that delay payment for both supplier and buyer.

1. Start with supplier and buyer information

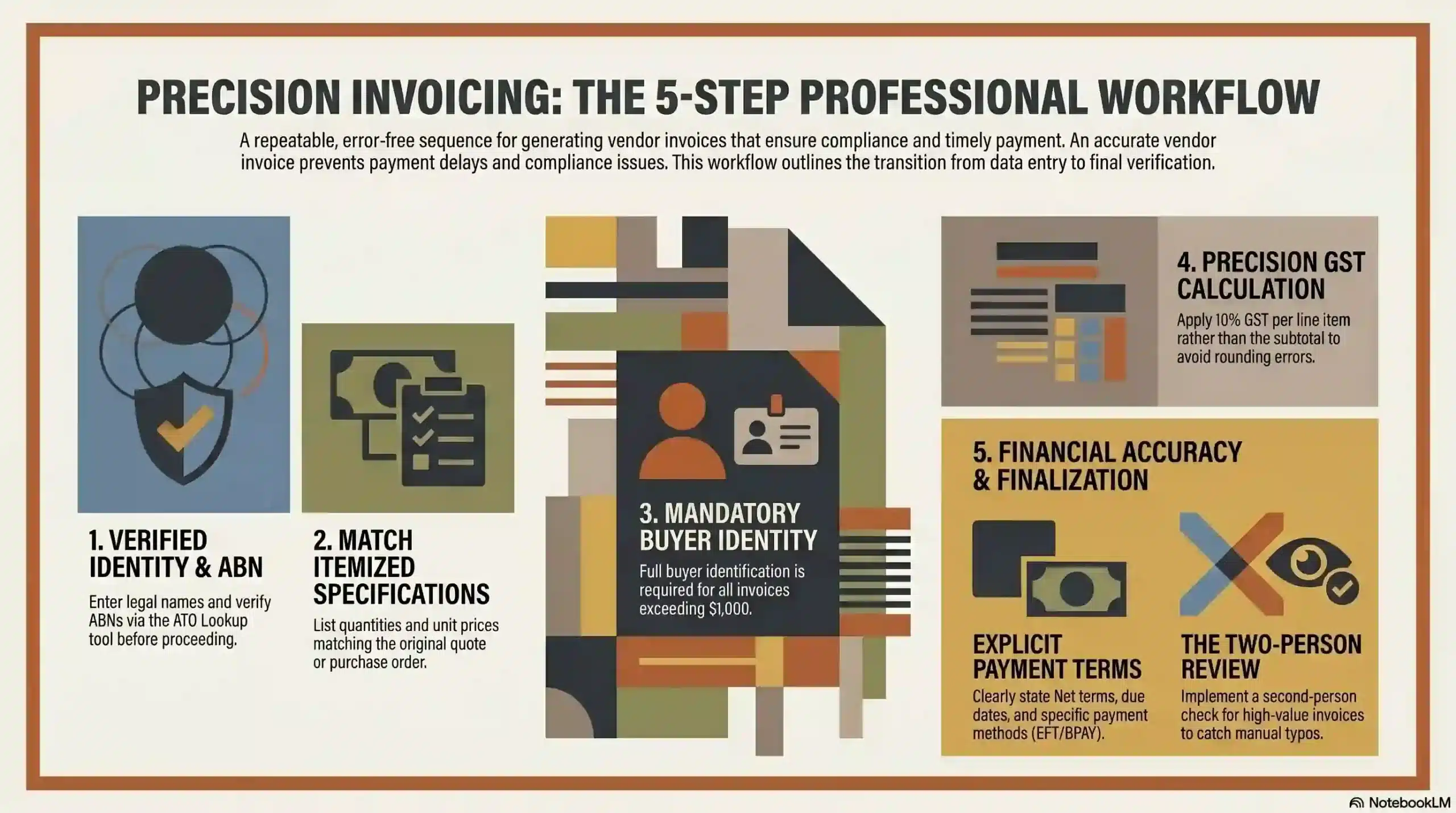

Enter the legal business names, addresses, and ABNs of both parties at the top of the invoice. Confirm the ABN against the ATO ABN Lookup tool before completing the document.

For invoices over $1,000, the buyer’s full identity is mandatory. Building this into step one prevents missed fields downstream when the focus shifts to line items and totals.

2. Add itemised products or services

List every product or service supplied, with descriptions matching the original quote or purchase order. Vague entries often trigger approval queries and slow the payment cycle.

Include unit price and quantity for each line, along with any product code or service identifier the buyer uses internally for reconciliation against their inventory or budget.

3. Calculate totals and GST correctly

Confirm GST is 10% of the taxable amount on relevant lines, with GST-free items excluded. Apply the rate per line rather than to the cumulative subtotal to avoid rounding drift.

The grand total equals the subtotal plus GST. Spreadsheet templates with locked formulas remove the risk of manual arithmetic errors that often appear in fast-paced billing cycles.

4. Add payment terms and supporting references

State payment terms clearly (Net 7, Net 14, Net 30) along with the calculated due date. Include the purchase order number and any contract reference to speed up internal matching.

List accepted payment methods with the corresponding details: BSB and account for EFT, BPAY biller code, or other instructions that prevent bounce-backs and follow-up calls.

5. Review accuracy before sending or recording

Cross-check the supplier name, ABN, invoice number, total, and GST amount before issuing or filing the invoice. Errors at this stage often cause weeks of payment delay later.

A short two-person review for higher-value invoices catches typos that single-person checks miss. Build the review step into the standard procedure rather than treating it as optional.

How the Vendor Invoice Process Works

The vendor invoice process, supported by a procurement automation platform, runs from invoice receipt to payment and audit storage.

Each step protects against errors, fraud, and duplicate payments. Mature processes usually involve five distinct stages, each with specific checks and ownership.

1. Invoice receipt and document capture

The invoice arrives by email, post, or e-invoicing portal and is captured into the accounting system. OCR scanning or e-invoicing automation reduces manual data entry significantly.

Capturing the invoice promptly, ideally on the day of receipt, prevents lost paperwork and allows the rest of the workflow to start within payment-term windows.

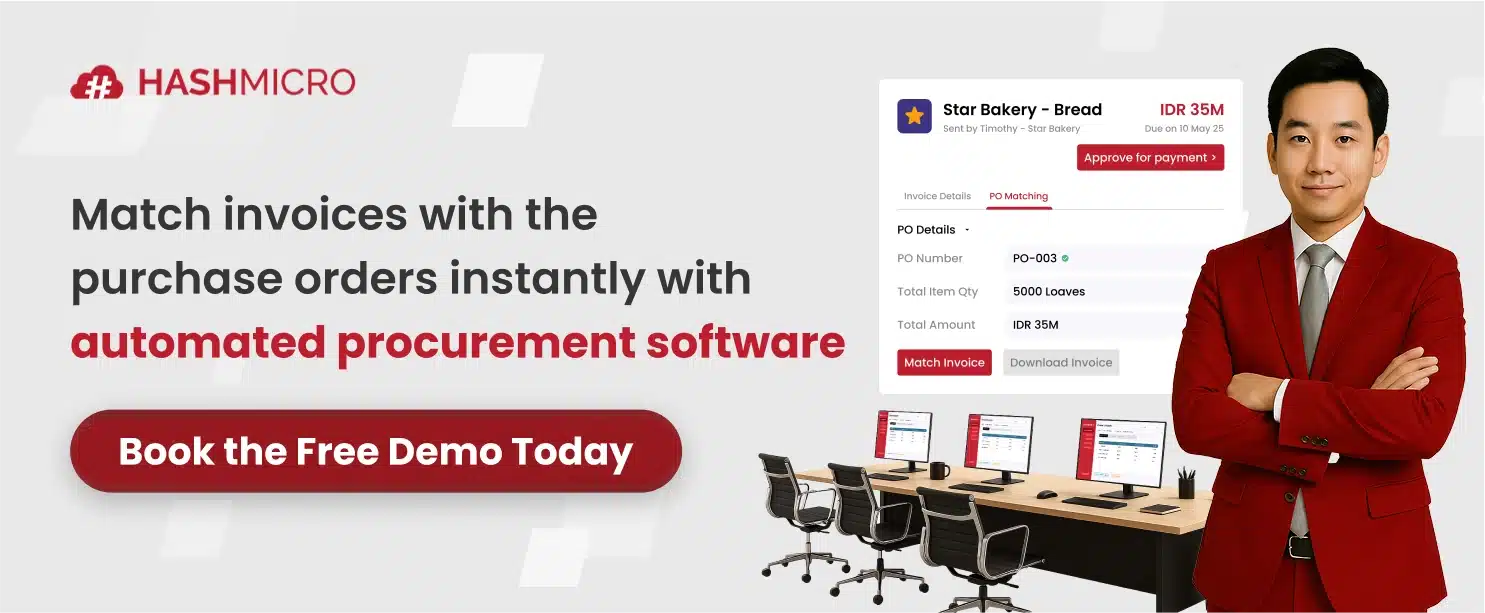

2. PO matching and goods receipt verification

Finance teams perform a three-way match between the invoice, the original purchase order, and the goods receipt note. Any mismatch in price, quantity, or item code is flagged for resolution.

This step prevents overpayment, fraud, and disputes. Automated matching engines in modern ERPs flag discrepancies in seconds, where manual matching often takes hours per invoice.

3. Internal review and approval workflow

The relevant department head or budget owner reviews the invoice to confirm the goods or services were received satisfactorily and the charge aligns with the agreed scope.

Approval thresholds typically scale with invoice value: smaller invoices may need only one approver, while larger ones require multi-level sign-off through CFO or board approval.

4. Recording the invoice in accounts payable

Once approved, the invoice is posted to the general ledger as a current liability under accounts payable, with the matching expense or asset account credited based on the line items.

Accurate posting affects financial reporting, BAS lodgement, and creditor balances. Double-entry conventions and a clear chart-of-accounts mapping prevent reconciliation issues at month end.

5. Payment scheduling and audit storage

Payment is scheduled according to terms, prioritising invoices that approach the due date or carry early-payment discounts. Batch payment runs reduce processing time and bank fees.

Once paid, the invoice is archived with proof of payment for the five-year ATO retention period. Cloud archives keep records searchable for both BAS reviews and supplier reconciliation.

Common Vendor Invoice Mistakes

Errors on vendor invoices create downstream pain: rejected GST credits, delayed payments, strained supplier relationships, and ATO compliance risk during BAS reviews.

The five mistakes below are the most frequent issues seen across Australian small and medium businesses. Each carries a clear fix.

1. Missing ABN or incomplete supplier details

Without a valid ABN, the document is not a tax invoice. The buyer cannot claim input GST credits and may need to apply no-ABN withholding rules, holding back 47% of the payment.

Always verify the supplier’s ABN through the free ATO ABN Lookup tool. Cancelled or incorrect ABNs cause exactly the same problems as a missing one when BAS lodgement comes around.

2. Incorrect GST calculation

Rounding errors, applying GST to exempt items, or omitting the breakdown on mixed supplies leads to incorrect BAS filings, ATO follow-up, and amended returns to fix later.

Calculate GST per line item rather than against the rolled-up subtotal. Spreadsheet formulas should round at the line level using consistent rules to avoid cumulative drift across the invoice.

3. Duplicate invoice numbers

Re-using invoice numbers across different transactions creates confusion in both supplier and buyer ledgers, and frequently results in overpayments, missed payments, or both.

Sequential numbering with a year prefix (for example, 2026-0001) keeps numbers unique and traceable. Accounting software typically enforces this rule automatically once configured.

4. Mismatch between invoice, PO, and received goods

Differences in price, quantity, or item code between the invoice, purchase order, and goods receipt require manual investigation that can take days, blocking payment in the meantime.

Tight purchase order discipline upfront prevents most mismatches. When discrepancies do appear, a single owner should drive resolution to avoid the issue stalling between teams.

5. Unclear payment terms or due dates

Vague language like “due on receipt” or “net soon” leaves room for interpretation. Buyers often default to their longest internal cycle, leading to late fees and supplier complaints.

Specify a calculated calendar due date alongside the term, such as “Net 30, due 30 May 2026”. Concrete dates remove ambiguity and accelerate scheduling at the buyer’s end.

Why Businesses Use a Vendor Invoice Template

Templates give Australian finance teams a stable baseline for invoice quality, compliance, and processing speed. The four benefits below explain why the template approach remains popular.

1. Save time on document preparation

A pre-built template removes the need to redesign the layout, reorder fields, or rewrite legal language for every invoice. Staff input data into known cells and the document is ready.

For supplier-side businesses issuing dozens of invoices a week, this saving translates directly into hours reclaimed for higher-value finance work each month.

2. Reduce formatting and calculation errors

Pre-set formulas in Excel templates calculate GST and totals automatically. Locked cells prevent accidental edits to key formulas, removing a major source of arithmetic mistakes.

Consistent formatting also reduces the risk of fields being missed. If the template requires an ABN before the document is generated, no invoice goes out without one.

3. Standardise invoice records across teams or branches

When every team or branch issues invoices using the same template, the finance head office sees a uniform structure during reconciliation, making month-end and audit work significantly faster.

Standardisation also helps suppliers process payments faster on the recipient side, since their AP teams recognise the layout and know exactly where to find each required field.

4. Support faster approvals and cleaner audits

Approvers move faster through invoices that follow a predictable structure, because they know where to find totals, GST, ABN, and payment terms without scanning the entire document.

Auditors equally benefit from standardised records. Clean templates with clear data trails reduce the time and questions involved during ATO BAS audits or external financial reviews.

When to Move from Templates to Invoice Automation

Templates work well at low volume, but as complexity grows, businesses evaluate procurement system options. As transactions increase, manual handling becomes a bottleneck that automation solves.

The four signals below indicate it is time to move beyond spreadsheet templates into a fully automated accounts payable workflow.

1. Signs manual invoice handling is slowing the business down

When the AP team spends hours each day on data entry, chasing missing approvals, or hunting paper invoices across desks, the manual workflow has hit its capacity limit.

Other warning signs include rising late-payment fees, missed early-payment discounts, and supplier complaints about response times. Each points to capacity strain that staffing alone will not fix.

2. Risks of spreadsheet-based invoice management

Spreadsheets carry no audit trail, no role-based access controls, and no automated validation. Errors can go undetected for weeks, only surfacing during BAS lodgement or external review.

Version control is the second risk. Multiple staff editing a shared workbook produces conflicting copies, and a single corrupt file can wipe weeks of invoice records without backup discipline.

3. How automation improves approval speed and visibility

Invoice templates are often sufficient for businesses with low invoice volumes. However, as transaction volumes increase, manual data entry, approval delays, and limited visibility can make template-based processes inefficient and prone to errors.

Invoice automation helps overcome these challenges by using OCR to capture invoice data automatically, matching invoices against purchase orders and goods receipts, and routing them to the appropriate approvers based on predefined rules.

Real-time dashboards also provide visibility into each invoice’s status, helping businesses reduce processing time, identify bottlenecks quickly, and maintain a complete audit trail without relying on spreadsheets or email chains.

4. How ERP helps connect procurement, AP, and finance

An ERP system creates an end-to-end purchasing framework linking the purchase-to-pay cycle in one platform. When a purchase order is raised, three-way matching with goods receipts and invoices happens automatically.

HashMicro’s ERP unifies procurement, accounts payable, and finance, removing handoffs between teams and giving the CFO a single view of cash flow obligations across every supplier relationship.

Conclusion

A vendor invoice is more than a payment request; it is a legal document central to Australian tax compliance, supplier relationships, and accurate financial reporting.

Using a structured template ensures every ATO-mandated field appears, every time, with built-in formulas reducing manual error risk for businesses at any scale.

As volume grows, moving from templates to automated invoice processing keeps accounts payable fast, accurate, and audit-ready. You can request a free consultation to optimise your accounts payable process.

FAQ About Vendor Invoices

-

Can vendors issue invoices in foreign currency in Australia?

Yes. ATO rules allow foreign currency invoices, but the AUD equivalent of GST and the total must also be shown. Use an ATO-accepted exchange rate at the date of supply or invoice issue.

-

What is a Recipient Created Tax Invoice (RCTI), and when can it be used?

An RCTI is issued by the buyer instead of the supplier, allowed in specific industries under a written ATO agreement between both parties. Common in agriculture and recurring service contracts.

-

What is the difference between a proforma invoice and a vendor invoice?

A proforma invoice is a preliminary quote sent before goods or services are delivered, with no payment obligation. A vendor invoice is the final billing document raised after delivery, requiring payment.

-

How are credit notes or invoice corrections handled in Australia?

Issue an adjustment note (or credit note) referencing the original tax invoice and showing the GST adjustment. Both supplier and buyer must update their BAS to reflect the change in the same period.

-

Is e-invoicing through the Peppol network mandatory in Australia?

Not yet for private businesses. All Commonwealth government agencies must accept Peppol e-invoices, and the framework is being progressively extended through ATO guidance for broader adoption.