A balance sheet is a financial statement that shows a business’s assets, liabilities, and owner’s equity at a specific point in time. It helps businesses assess financial position, monitor liquidity, support reporting obligations, and evaluate overall financial health.

A balance sheet template gives Australian businesses a clear structure for capturing what the company owns, what it owes, and what value remains for the owners at one fixed reporting date.

It draws assets, liabilities, and equity into a single statement, helping directors plan capital, support loan applications, and meet AASB, ATO, and ASIC obligations through the financial year.

This article covers what a balance sheet is, its components, the main template formats used in Australia, and step-by-step instructions for preparing one accurately for 2026 reporting.

Key Takeaways

Balance sheet is a financial statement showing what a business owns, owes, and holds in equity at one specific reporting date.

Three pillars define every balance sheet: assets listed in order of liquidity, liabilities split by maturity, and owner's equity.

Steps to prepare a balance sheet: choose a reporting date, list assets and liabilities, calculate owner's equity, verify the accounting equation balances, then review for accuracy and check ASIC obligations.

Free downloadable templates aligned with AASB and ATO conventions help sole traders and companies record their financial position optimally.

What Is a Balance Sheet?

A balance sheet, called the Statement of Financial Position under AASB 101, is a financial statement showing what a business owns, owes, and holds in equity at one specific date. It is one of the core financial system fundamentals every business owner should understand.

It captures a single moment rather than performance over time like a profit and loss. Together with cash flow and profit and loss reports, it forms the full suite of financial statements used to assess business performance.

The accounting equation governs the entire document and must always balance: Assets = Liabilities + Owner’s Equity. This identity is the test that proves the statement has been compiled correctly.

For Australian business owners, the balance sheet sits at the centre of credit decisions, investor due diligence, and internal capital planning. Banks rely on it heavily when assessing loan applications.

Under the Corporations Act 2001, certain entities must prepare audited financial statements, including a balance sheet, and lodge them with the Australian Securities and Investments Commission (ASIC) each year.

Australian Bureau of Statistics data shows small and medium businesses make up the bulk of the economy, making an AASB-aligned balance sheet essential for credit access and growth planning.

A well-prepared template lets owners spot liquidity issues early, monitor leverage, and confirm the capital structure is positioned for long-term resilience across changing market conditions.

What Are the Key Components of a Balance Sheet?

Every balance sheet template, regardless of complexity, rests on three components: assets, liabilities, and owner’s equity. Each one tells a different part of the financial story.

Under AASB 101, these components must be classified and presented so users can assess financial position with clarity. The standard practice in Australia is to split assets and liabilities into current and non-current.

Getting this classification right matters because it directly affects how lenders, investors, and auditors interpret the company’s short-term liquidity and long-term solvency in the same statement.

1. Assets

Assets are resources the business owns or controls from past transactions, with future economic benefit expected to flow to the entity. They are listed in order of liquidity, from most to least convertible.

Current assets are realised, sold, or consumed within the normal operating cycle, typically 12 months. They include cash and cash equivalents, trade debtors, inventory, and prepaid expenses.

Trade debtors should be reported net of any allowance for doubtful debts, while inventory must be valued using ATO-accepted methods such as FIFO or weighted average to satisfy compliance.

Non-current assets are held for more than a year and underpin ongoing operations. They cover property, plant, and equipment, intangible assets, long-term investments, and deferred tax assets.

Property, plant, and equipment depreciate over their useful life apart from land, while intangibles such as patents, trademarks, and goodwill represent value that cannot be physically touched or moved.

2. Liabilities

Liabilities are obligations the business owes to external parties, arising from past transactions, where settlement is expected to result in an outflow of resources holding economic value.

Current liabilities settle within 12 months and include accounts payable, short-term debt, the current portion of long-term loans, accrued expenses, and Australian statutory liabilities.

Statutory liabilities are unique to Australia and cover GST payable from the Business Activity Statement, PAYG withholding, and Superannuation Guarantee amounts not yet remitted to employee funds.

Non-current liabilities extend beyond 12 months and reflect the long-term financing strategy. They include long-term loans, equipment finance, deferred tax liabilities, and long service leave provisions.

3. Owner’s Equity

Owner’s equity is the residual interest in the assets of the business after deducting all liabilities. It represents what would theoretically return to owners if every asset was sold and every debt paid.

For Pty Ltd and Ltd companies, share capital reflects the total invested by shareholders in exchange for shares, while retained earnings track cumulative net profit kept inside the business.

Sole traders and partnerships use owner’s drawings to track withdrawals for personal use. Drawings reduce equity directly and should never be classified as a business expense on the profit and loss.

Reserves capture allocations set aside for specific purposes, such as an asset revaluation reserve created when property is revalued upwards in line with current market value and AASB 116.

Types of Balance Sheet Templates in Australia

There is no single template that suits every Australian business. Size, structure, and reporting obligations dictate which format works best, even though the accounting equation never changes.

Choosing the wrong format can either bury important detail or overcomplicate a small operation. The five formats below cover most common scenarios in the Australian market.

1. Simple balance sheet

The simple balance sheet lists assets, liabilities, and equity without splitting them into current and non-current categories. It gives a fast, top-level view of the financial position.

It suits micro-businesses, freelancers, and sole traders with minimal inventory and no long-term debt. It rarely satisfies bank loan applications or any analytical work needing liquidity ratios.

2. Classified balance sheet

The classified balance sheet is the standard format used by most Australian small and medium businesses. It separates assets and liabilities into current and non-current sections under AASB 101.

This split lets stakeholders judge short-term liquidity and long-term solvency at a glance. Australian banks and ASIC reviewers expect a classified format whenever financials are submitted formally.

3. Common-size balance sheet

A common-size balance sheet expresses each line item as a percentage of total assets, turning raw dollars into structural ratios that can be benchmarked against competitors of any size.

If accounts receivable jumps from 10% to 25% of total assets, the format flags a credit control issue immediately, well before raw dollar values would have made the change obvious to management.

4. Consolidated balance sheet

A consolidated balance sheet combines the financial position of a parent company and its subsidiaries into one statement, treating the group as a single economic entity under AASB 10.

Preparation requires eliminating intercompany balances and transactions, such as loans from parent to subsidiary, to prevent double-counting. Larger Australian corporate groups use this format every year.

3. Comparative balance sheet

A comparative balance sheet shows two or more periods side by side, such as 30 June 2026 next to 30 June 2025. The format is built for trend analysis and year-on-year financial review.

It exposes whether debt is climbing, inventory is bloating, or equity is strengthening. Comparative reporting is mandatory for entities preparing General Purpose Financial Statements in Australia.

Ready-to-Use Balance Sheet Templates Australia

Below are five paste-ready templates aligned with Australian accounting conventions. Recreate them in Excel or Google Sheets, or load them into accounting software for live reconciliation.

Manual templates are excellent for learning the structure, but moving to automation through an integrated ERP like HashMicro removes data entry errors and keeps the balance sheet current at all times.

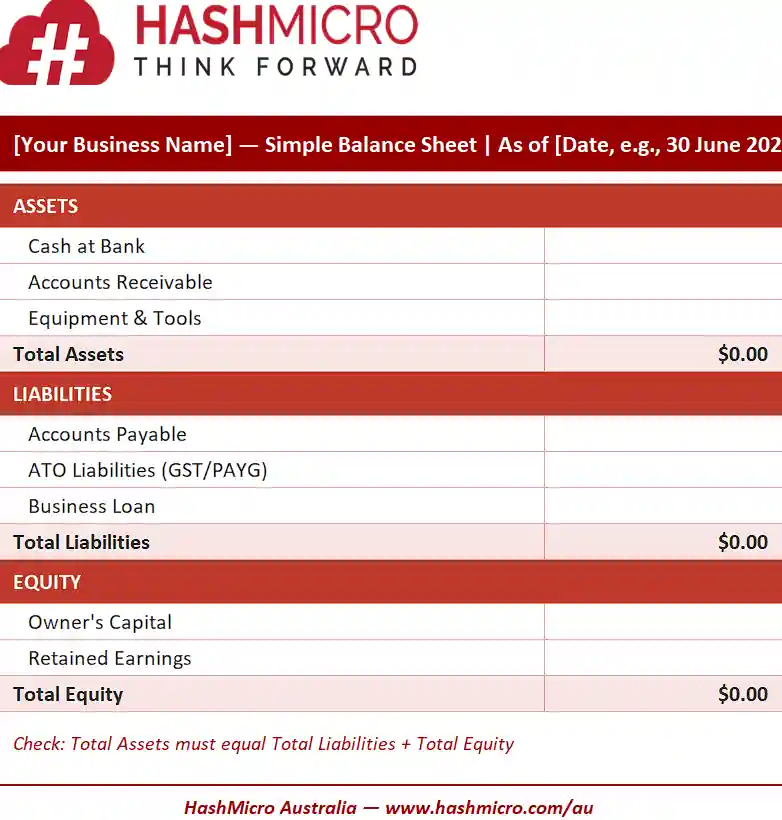

1. Simple balance sheet template

Best suited to a sole trader or freelancer with minimal complexity.

| Simple Balance Sheet | |

|---|---|

| ASSETS | |

| Cash at Bank | $ [Amount] |

| Accounts Receivable | $ [Amount] |

| Equipment & Tools | $ [Amount] |

| Total Assets | $ [Total A] |

| LIABILITIES | |

| Accounts Payable | $ [Amount] |

| ATO Liabilities (GST/PAYG) | $ [Amount] |

| Business Loan | $ [Amount] |

| Total Liabilities | $ [Total L] |

| EQUITY | |

| Owner’s Capital | $ [Amount] |

| Retained Earnings | $ [Amount] |

| Total Equity | $ [Total E] |

Check: Total Assets must equal Total Liabilities + Total Equity.

Simple balance sheet template

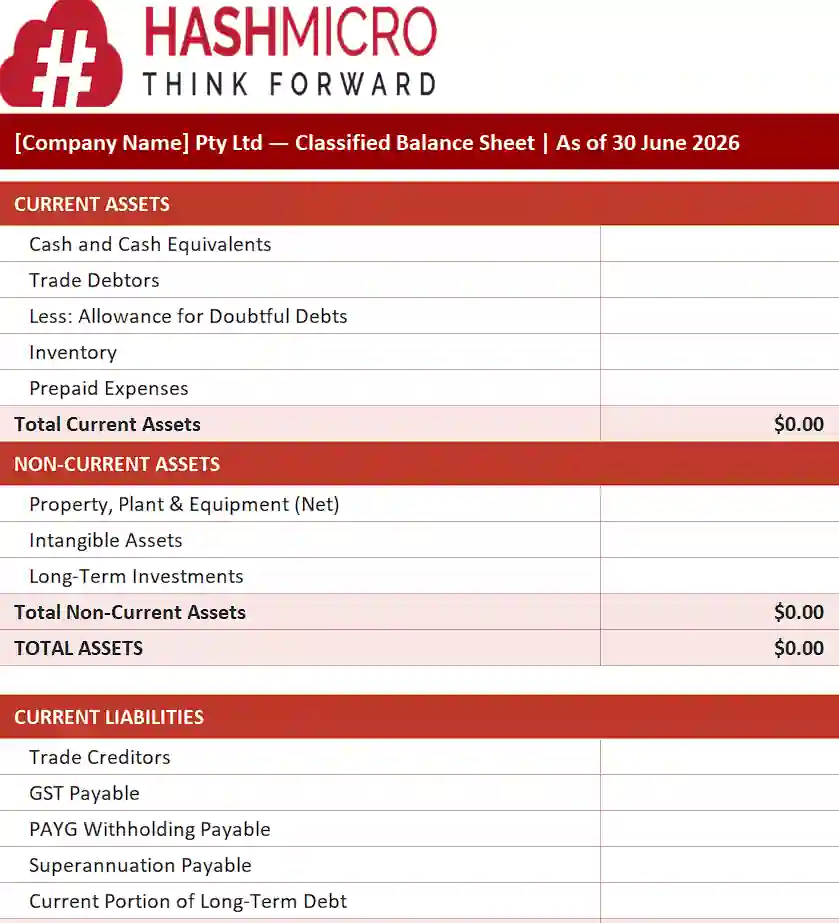

2. Classified balance sheet template

Built for Pty Ltd companies needing current and non-current classification with Australian statutory line items.

| Line Item | 30 June 2026 | 30 June 2025 | Change ($) |

|---|---|---|---|

| Total Current Assets | $ [Amount] | $ [Amount] | $ [Δ] |

| Total Non-Current Assets | $ [Amount] | $ [Amount] | $ [Δ] |

| Total Assets | $ [Total] | $ [Total] | $ [Δ] |

| Total Current Liabilities | $ [Amount] | $ [Amount] | $ [Δ] |

| Total Non-Current Liabilities | $ [Amount] | $ [Amount] | $ [Δ] |

| Total Liabilities | $ [Total] | $ [Total] | $ [Δ] |

| Total Equity | $ [Total] | $ [Total] | $ [Δ] |

Classified balance sheet template

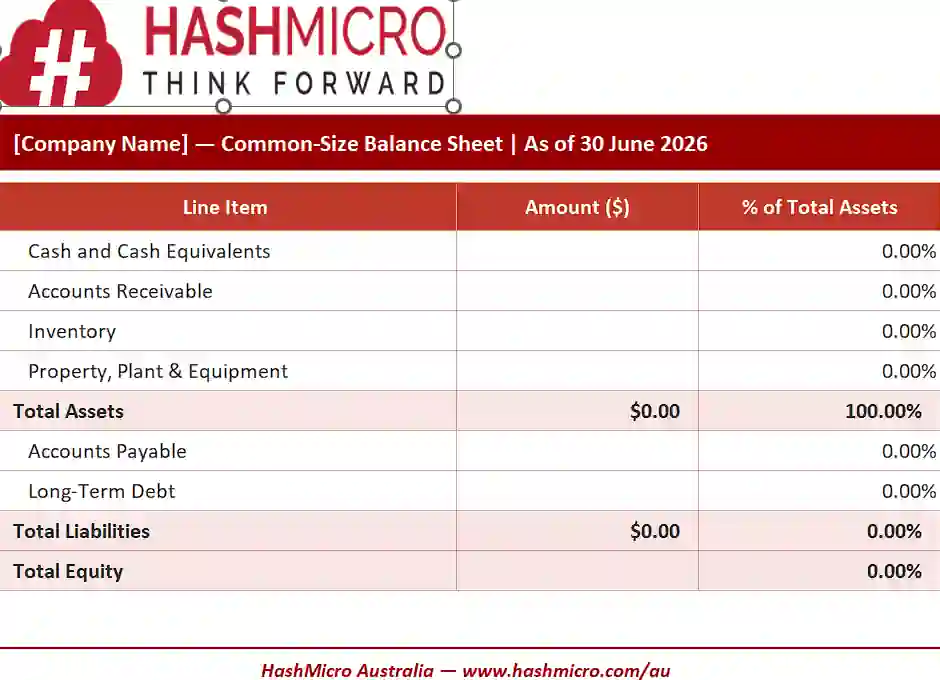

3. Common-size balance sheet template

Each line item expressed as a percentage of total assets for benchmarking and structural review.

| Line Item | Amount ($) | % of Total Assets |

|---|---|---|

| Cash and Cash Equivalents | $ [Amount] | [%] |

| Accounts Receivable | $ [Amount] | [%] |

| Inventory | $ [Amount] | [%] |

| Property, Plant & Equipment | $ [Amount] | [%] |

| Total Assets | $ [Total] | 100% |

| Accounts Payable | $ [Amount] | [%] |

| Long-Term Debt | $ [Amount] | [%] |

| Total Liabilities | $ [Total] | [%] |

| Total Equity | $ [Total] | [%] |

Common-size balance sheet template

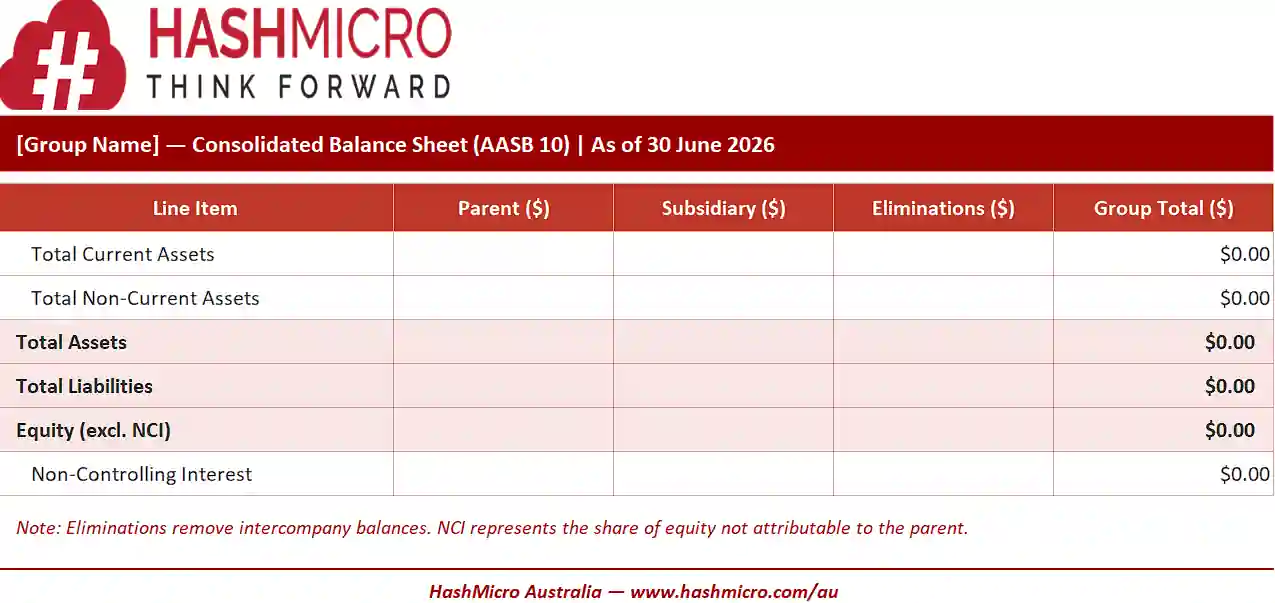

4. Consolidated balance sheet template

Combines parent company and subsidiaries into one set of group financials under AASB 10.

| Line Item | Parent ($) | Subsidiary ($) | Eliminations ($) | Group Total ($) |

|---|---|---|---|---|

| Total Current Assets | $ [A] | $ [A] | ($ [A]) | $ [A] |

| Total Non-Current Assets | $ [A] | $ [A] | ($ [A]) | $ [A] |

| Total Assets | $ [T] | $ [T] | ($ [T]) | $ [T] |

| Total Liabilities | $ [L] | $ [L] | ($ [L]) | $ [L] |

| Equity (excl. NCI) | $ [E] | $ [E] | ($ [E]) | $ [E] |

| Non-Controlling Interest | – | – | – | $ [NCI] |

Consolidated balance sheet template

5. Comparative balance sheet template

A comparative balance sheet shows two or more reporting periods side by side, letting teams track how assets, liabilities, and equity shift over time. Auditors and investors often request this format for trend analysis.

| Line Item | 30 June 2026 | 30 June 2025 | Change ($) |

|---|---|---|---|

| Total Current Assets | $ [Amount] | $ [Amount] | $ [Δ] |

| Total Non-Current Assets | $ [Amount] | $ [Amount] | $ [Δ] |

| Total Assets | $ [Total] | $ [Total] | $ [Δ] |

| Total Current Liabilities | $ [Amount] | $ [Amount] | $ [Δ] |

| Total Non-Current Liabilities | $ [Amount] | $ [Amount] | $ [Δ] |

| Total Liabilities | $ [Total] | $ [Total] | $ [Δ] |

| Total Equity | $ [Total] | $ [Total] | $ [Δ] |

Consolidated balance sheet template

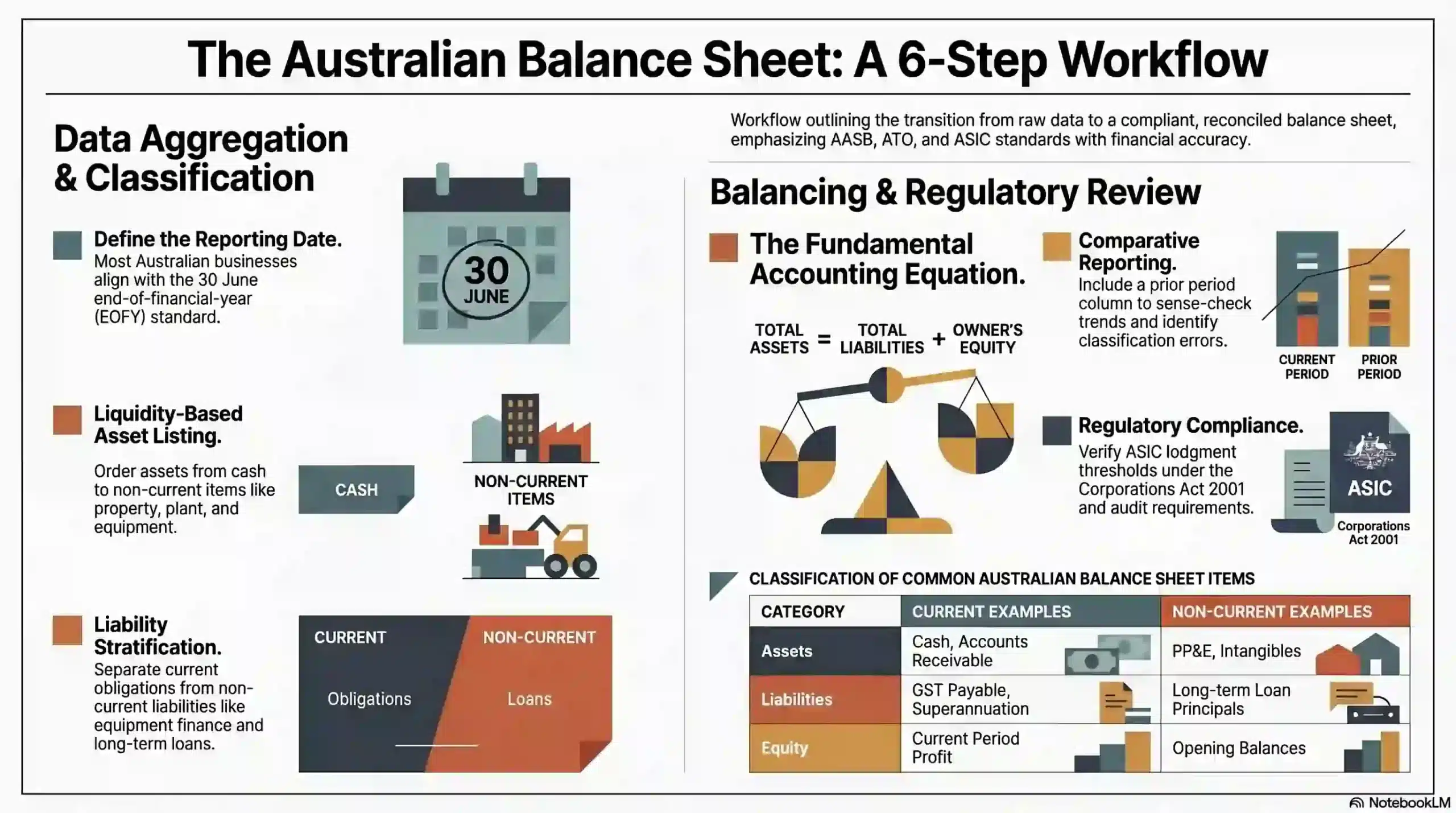

How to Prepare a Balance Sheet in Australia

Preparing a balance sheet means moving from raw transaction data to a final, reconciled statement that satisfies AASB, ATO, and lender expectations across the financial year.

The six steps below cover the core workflow for sole traders, companies, and not-for-profits, whether the statement is being prepared for end of financial year or an interim review using one of the top accounting software options available to Australian businesses.

1. Choose your reporting date

Most Australian businesses align their balance sheet with the standard end of financial year on 30 June, the date the ATO uses for income tax assessment and BAS reporting cycles.

Companies with an approved Substituted Accounting Period may choose another date, while interim reporting at 31 December or month-end suits internal reviews and quarterly board reporting.

2. List all assets

Begin with current assets in order of liquidity: cash and cash equivalents, accounts receivable net of doubtful debts, inventory at the chosen valuation method, and prepaid expenses.

Move next to non-current assets, recording PP&E at cost less accumulated depreciation, then add intangibles, long-term investments, and any deferred tax assets confirmed through tax workings.

3. List all liabilities

Current liabilities include accounts payable, GST payable from the BAS, PAYG withholding, superannuation owed, current portions of long-term debt, and accrued staff entitlements due within 12 months.

Non-current liabilities cover long-term loan principals beyond 12 months, equipment finance, deferred tax liabilities, and long service leave provisions extending past the next year.

4. Calculate owner’s equity and classify current vs. non-current

Equity blends opening balances, current period profit, owner contributions, and any drawings or dividends paid during the period. Each movement should reconcile back to the source ledger.

While compiling each section, confirm the current versus non-current split is correct. Misplacing a long-term loan as current can damage liquidity ratios and frighten lenders unnecessarily.

5. Verify the accounting equation

Once each section is totalled, run the check that defines the entire statement: Assets = Liabilities + Owner’s Equity. Total assets must equal total liabilities plus total equity, without exception.

If the figures disagree, the statement is not yet ready for use. Common causes include retained earnings not rolling forward, a missing one-sided journal, or a typo in a single line item.

6. Review for accuracy, add comparative figures, and check ASIC obligations

Add the prior period column for comparative reporting, then sense-check the trend on each major line. Sharp movements without an operational reason often signal a posting or classification error.

Confirm whether the entity must lodge the balance sheet with ASIC under the Corporations Act 2001 thresholds, and whether audit, review, or directors’ declaration requirements apply for the period.

Balance Sheet Format by Business Structure in Australia

Australian business structures shape the balance sheet’s equity section more than its asset or liability sections. Each structure carries different legal and tax obligations under ATO and ASIC rules.

Choosing the right format keeps the statement aligned with the structure’s compliance pathway, whether that is a sole trader BAS lodgement or a company General Purpose Financial Statement.

1. Sole trader balance sheet

A sole trader balance sheet typically uses the simple format. Equity collapses to a single owner’s capital account, with drawings tracked as a contra-account that reduces the year-end balance.

There is no legal separation between the trader and the business, so personal liability extends to business debts. The statement still informs personal income tax and any ABN-linked finance applications.

2. Company balance sheet

A Pty Ltd or Ltd company uses the classified format with a clearly defined equity section showing share capital, retained earnings, reserves, and any non-controlling interest in subsidiaries.

Companies face stricter reporting thresholds under the Corporations Act 2001 and may need to prepare General Purpose Financial Statements depending on size, ownership, and consolidation requirements.

3. Partnership balance sheet

Partnerships record a separate capital account for each partner, capturing initial contributions, share of profits, drawings, and any loans made to the partnership through the financial year.

The partnership itself does not pay income tax. Profits flow to partners’ individual returns, but a clear balance sheet is still essential for distribution accuracy and dispute resolution.

4. Nonprofit/charity balance sheet

Not-for-profits and registered charities replace owner’s equity with accumulated funds or reserves, often split between unrestricted, restricted, and endowment categories under donor conditions.

ACNC-registered charities must follow the Australian Charities and Not-for-profits Commission reporting framework, with tiered AASB compliance based on annual revenue and operational scale.

How to Read and Analyse a Balance Sheet

Reading a balance sheet means asking what the totals reveal about liquidity, leverage, and operational health, not just confirming that the equation balances at the end of a reporting period.

Three core metrics give a fast diagnostic: the current ratio for short-term solvency, debt-to-equity for capital structure risk, and working capital for day-to-day operational headroom.

1. Current ratio

Current ratio is calculated as current assets divided by current liabilities. It measures whether the business can meet short-term obligations using its most readily convertible assets.

A ratio between 1.5 and 2.0 is generally considered healthy in Australia. Below 1.0 signals strain on cash flow, while a very high figure may indicate idle cash that could be deployed elsewhere.

2. Debt-to-equity ratio

Debt-to-equity divides total liabilities by total equity. The metric exposes how much of the business is funded through borrowings versus owner investment, and where financial risk concentrates.

Australian lenders use this ratio when assessing loan applications. A high figure can disqualify finance approvals, especially when the Reserve Bank of Australia is in a tightening interest rate cycle.

3. Working capital

Working capital is the dollar difference between current assets and current liabilities. It reflects the operational liquidity available to fund day-to-day activity and short-term growth initiatives.

A negative working capital figure points to potential cash strain, while consistent positive working capital supports payroll, supplier payments, and unexpected expenses without external borrowing.

Balance Sheet and Australian Regulatory Requirements

An Australian balance sheet sits within a regulatory framework managed by ASIC, the ATO, and AASB. Each places different obligations on what must be reported, when, and to what assurance level.

The three subsections below outline lodgement requirements, ATO interactions through the company tax return, and the statutory line items that distinguish Australian balance sheets from those overseas.

1. When must an Australian business lodge a balance sheet with ASIC?

Public companies, large proprietary companies, and registered foreign companies must lodge audited financial statements, including a balance sheet, with ASIC each year under the Corporations Act 2001.

A proprietary company is large when it meets two of three thresholds across revenue, gross assets, and employees. Small proprietary companies generally have no lodgement duty unless directed by ASIC.

2. Balance sheet and your ATO company tax return

The balance sheet feeds directly into the company tax return through schedules covering reconciliation of accounting profit to taxable income, asset registers, and shareholder loan disclosures.

Director or shareholder loans must be reviewed for Division 7A compliance. Unsecured loans without a complying agreement risk being treated as deemed unfranked dividends, triggering significant tax penalties.

The franking account, while not on the face of the balance sheet, runs alongside it. Distributions and tax instalments must be tracked to ensure dividends are correctly franked at year end.

3. GST, PAYG, and superannuation line items unique to Australian balance sheets

Three statutory liabilities appear on Australian balance sheets that overseas templates often miss: GST payable, PAYG withholding, and Superannuation Guarantee payable. These reflect key employer tax withholding duties under Australian law.

Each must be reconciled at period end to the corresponding ATO ledger. Underpayment of super carries automatic penalties through the Super Guarantee Charge, separate from regular tax compliance.

Common Balance Sheet Mistakes Australian Businesses Make

Even experienced bookkeepers make recurring errors that distort balance sheet readings, weaken loan applications, or trigger ATO and ASIC follow-up. The three below are the most damaging in practice.

1. Missing Australia-specific line items

Generic templates pulled from overseas sources rarely include GST payable, PAYG withholding, or Superannuation Guarantee payable as separate liabilities, even though these are mandatory in Australia.

Folding statutory liabilities into accounts payable hides them from auditors, lenders, and management. Always show GST, PAYG, and super as discrete current liability lines on the statement.

2. Not separating current from non-current assets and liabilities

Listing a five-year commercial loan entirely as a current liability artificially crashes the current ratio and makes the business look insolvent on paper, even when cash flow is healthy.

Only the principal due in the next 12 months belongs in current liabilities. The remainder sits as non-current. The same rule applies in reverse for long-dated receivables and term deposits.

3. Confusing owner’s drawings with a business expense

Owner’s drawings reduce equity, not profit. Treating them as a business expense overstates costs, understates profit, and distorts both the income statement and the equity section of the balance sheet.

Sole traders and partnerships are most prone to this error. Run drawings through a contra-equity account that reduces total equity at year end, never through a profit and loss expense line.

Conclusion

A balance sheet template gives Australian businesses a reliable structure for recording assets, liabilities, and equity at any reporting date, supporting both compliance and strategic decisions.

Whether the entity is a sole trader using the simple format or a corporate group preparing consolidated statements, the same accounting equation applies and the same statutory line items must appear.

If you are interested in using your own balance sheet, you can consult our experts to start implementing this change today.

FAQ About Balance Sheet Templates

-

How often should an Australian business prepare a balance sheet?

Most Australian businesses prepare a balance sheet at least annually for the 30 June EOFY. Quarterly or monthly preparation supports better cash flow management and faster strategic decisions.

-

What is the difference between book value and market value on a balance sheet?

Book value reflects the historical cost of assets minus depreciation, while market value reflects what the asset would sell for today. Balance sheets primarily use book value under AASB rules.

-

How long must Australian businesses keep balance sheet records?

The ATO requires records supporting tax returns to be kept for five years from lodgement. ASIC-regulated companies must retain records for seven years under the Corporations Act 2001.

-

Can a balance sheet show negative equity, and what does it mean?

Yes. Negative equity occurs when total liabilities exceed total assets, often after sustained losses. It signals insolvency risk and may trigger director duties under the Corporations Act 2001.

-

Do crypto holdings or NFTs go on an Australian balance sheet?

Yes. Cryptocurrency and digital assets are recorded as intangible assets or inventory under AASB guidance, valued at cost or fair value depending on intent and how the business uses them.