Fringe Benefits Tax (FBT) applies when a business provides non-cash benefits such as vehicles, entertainment, or allowances to employees. It determines how these benefits are taxed and reported as part of overall compensation.

Understanding how FBT works helps businesses calculate taxable value, meet reporting obligations, and avoid penalties. With the right approach, FBT becomes easier to manage alongside payroll and financial processes.

Key Takeaways

Explains how Fringe Benefits Tax applies to non-cash employee benefits and impacts payroll, reporting, and overall compliance obligations.

Identifies common fringe benefits such as vehicles, entertainment, and expense payments that must be assessed and classified correctly.

Breaks down how FBT is calculated using gross-up rates, taxable value, and employee contributions to determine total liability.

Provides ready-to-use templates to track benefits, calculate FBT, and support accurate reporting throughout the year.

What Is Fringe Benefits Tax (FBT)?

Fringe Benefits Tax is a tax applied to non-cash benefits provided to employees in addition to their salary or wages. These benefits can include company cars, expense payments, or lifestyle-related perks.

FBT is paid by the employer, not the employee. It is calculated separately from income tax and follows a specific reporting period, which means businesses must track and assess these benefits accurately throughout the year.

Why Ffringe Benefits Tax Matters For Businesses

Managing FBT correctly affects both compliance and cost control. It influences how employee benefits are structured and how financial obligations are calculated.

Legal obligation under the FBT framework

FBT is regulated under a specific tax framework, requiring businesses to identify, calculate, and report all eligible benefits. Failing to meet these obligations can lead to penalties and compliance issues.

Impact on employee remuneration and payroll cost

Non-cash benefits form part of overall compensation and benefits for employees. Therefore, FBT directly affects payroll costs and must be considered when designing salary packages or offering additional perks.

Reducing audit and penalty risks

Accurate FBT reporting lowers the risk of audits and unexpected charges. Proper documentation and tracking help businesses demonstrate compliance and avoid costly corrections.

Who Is Subject to Fringe Benefits Tax

FBT applies to businesses that provide benefits beyond standard wages. The scope is broader than many expect, covering different types of entities and recipients.

Employers providing non-cash benefits

Any employer that offers benefits such as vehicles, reimbursements, or entertainment may be subject to FBT. These benefits must be identified and assessed correctly.

Benefits to family members or associates

FBT can still apply even if the benefit is provided to someone other than the employee, such as family members or related parties. What matters is the connection to the employee.

Directors, office holders, and trust beneficiaries

FBT is not limited to standard employees. It can also apply to directors and individuals who receive benefits through business structures such as trusts.

Not-for-profits and concession entities

Certain entities may receive concessions or exemptions, but they are still required to assess FBT obligations. Eligibility depends on the type of entity and the benefits provided.

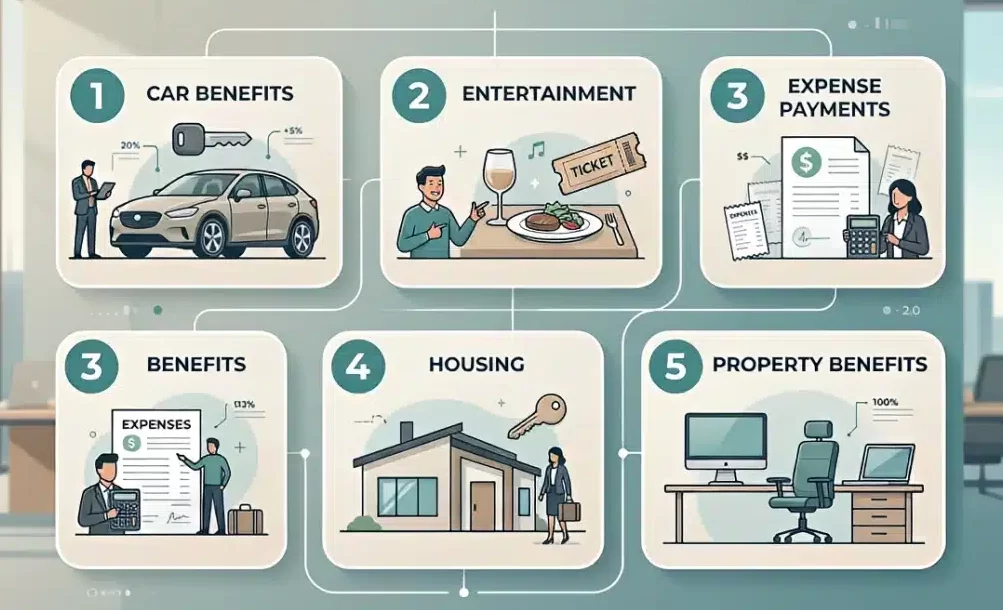

Types of Fringe Benefits Subject to FBT

Fringe benefits cover a wide range of non-cash compensation provided to employees. Each category has its own valuation rules, so identifying the correct type is essential for accurate FBT calculation.

Common fringe benefits subject to FBT include:

- Car and car parking benefits

Benefits arise when employees use company vehicles for private purposes or receive parking privileges provided by the business. - Entertainment and meal benefits

This includes meals, events, or recreational activities provided to employees, whether on-site or off-site. - Expense payment and loan benefits

Occurs when a business pays for personal expenses or provides loans at reduced or no interest. - Housing and living-away-from-home allowance

Applies when employees are provided accommodation or receive allowances while working away from their usual residence. - Property and residual benefits

Covers goods or services provided that do not fall into other specific categories. - Reportable fringe benefits amount

Certain benefits must be reported on employee income statements, even though the tax is paid by the employer.

Understanding these categories helps ensure that all applicable benefits are captured and reported correctly.

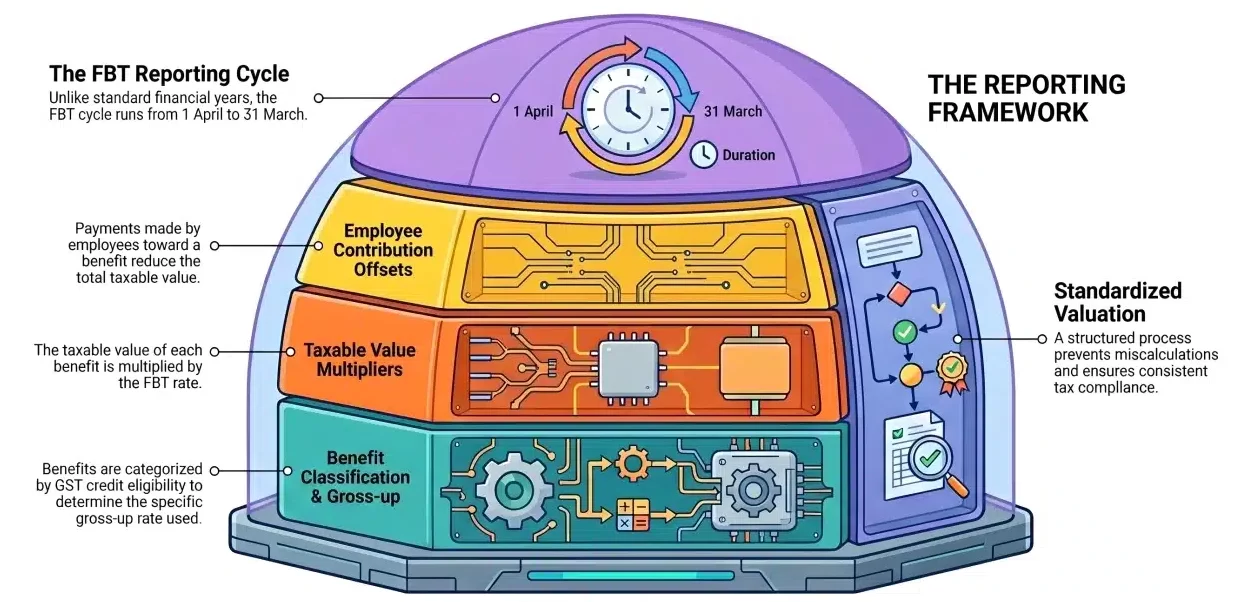

How Fringe Benefits Tax Is Calculated

Calculating FBT involves multiple components, including benefit classification, valuation, and applicable rates. A structured approach helps businesses avoid miscalculations and reporting errors.

To determine FBT payable, businesses typically follow this process:

- Type 1 and Type 2 benefits and gross-up rates

Benefits are classified based on whether GST credits can be claimed. Each type uses a different gross-up rate to calculate the taxable value. - FBT rate and taxable value calculation

The taxable value of each benefit is calculated first, then multiplied by the applicable FBT rate to determine the amount payable. - Employee contributions and adjustments

Any amount paid by the employee toward the benefit can reduce the taxable value, lowering the overall FBT liability. - FBT year reporting period

FBT is calculated based on a specific reporting cycle, which runs from 1 April to 31 March, not the standard financial year.

By following this structured calculation process, businesses can ensure that FBT obligations are met accurately and consistently.

FBT Exemptions and Concessions

Not all benefits are subject to FBT. Certain exemptions and concessions can reduce or eliminate the tax liability, depending on the nature of the benefit and how it is provided.

Minor benefits exemption

Benefits with a low value may be exempt if they are provided infrequently and meet specific conditions. This helps reduce the need to track small, irregular perks.

Work-related items exemption

Items such as laptops, mobile phones, and tools used primarily for work purposes are generally exempt. These are considered necessary for performing job duties rather than personal benefits.

Otherwise deductible rule

If an employee could have claimed a tax deduction for the expense personally, the taxable value of the benefit can be reduced. This ensures that employees are not taxed twice on work-related costs.

Concessions for eligible entities

Certain entities may receive reduced FBT obligations or rebates. Eligibility depends on the type of entity and how benefits are provided to employees.

How to Lodge and Pay FBT

Once benefits are identified and calculated, businesses need to complete the reporting and payment process correctly. This ensures compliance and avoids penalties.

Registering for FBT

Businesses must register for FBT before lodging returns. This establishes their obligation to report and pay tax on fringe benefits.

Recording and tracking benefits

Accurate records must be maintained throughout the year. This includes details of the benefit, recipient, and calculated value.

Calculating FBT payable

The total taxable value is determined based on benefit categories, adjustments, and applicable rates. This forms the basis of the FBT liability.

Lodging the annual return

FBT returns must be submitted within the required timeframe under ATO lodgement rules. Late lodgement can result in penalties and additional scrutiny.

Managing instalments

Some businesses may be required to pay FBT instalments. These are typically included in regular activity statements to spread the tax burden.

How Businesses Manage FBT Across Indsutries

FBT requirements apply across industries, but the types of benefits and how they are managed can vary depending on operational needs.

Professional services

Businesses in this sector often provide benefits such as vehicles, allowances, or expense reimbursements. Managing FBT involves ensuring these benefits are properly documented and valued.

Retail and hospitality

Employee benefits may include meals, entertainment, or staff discounts. These require careful tracking to determine whether they fall within FBT rules or exemptions.

Construction and trades

Benefits can include vehicles, tools, and travel-related allowances. Accurate classification is important to avoid overreporting or missing taxable items.

Healthcare and not-for-profit

Some entities may qualify for concessions, but they still need to assess benefits carefully. Proper documentation ensures that exemptions are applied correctly.

Common FBT Compliance Mistakes to Avoid

Even when businesses understand FBT rules, errors can still occur due to inconsistent tracking or incorrect assumptions. Identifying common mistakes helps reduce compliance risks.

Common FBT mistakes include:

- Failing to identify all fringe benefits provided to employees

- Misclassifying benefits, leading to incorrect tax treatment

- Not applying exemptions or concessions correctly

- Keeping incomplete or inconsistent records

- Missing lodgement deadlines or reporting incorrect values

Avoiding these issues requires consistent processes and regular review of FBT data.

Download Free FBT Template for Reporting

Managing FBT manually often leads to inconsistent records and missed details. Using a structured template helps standardise how benefits are tracked, calculated, and reported throughout the FBT year.

The templates below are designed to support accurate reporting and align with FBT requirements, making it easier to organise data and prepare returns.

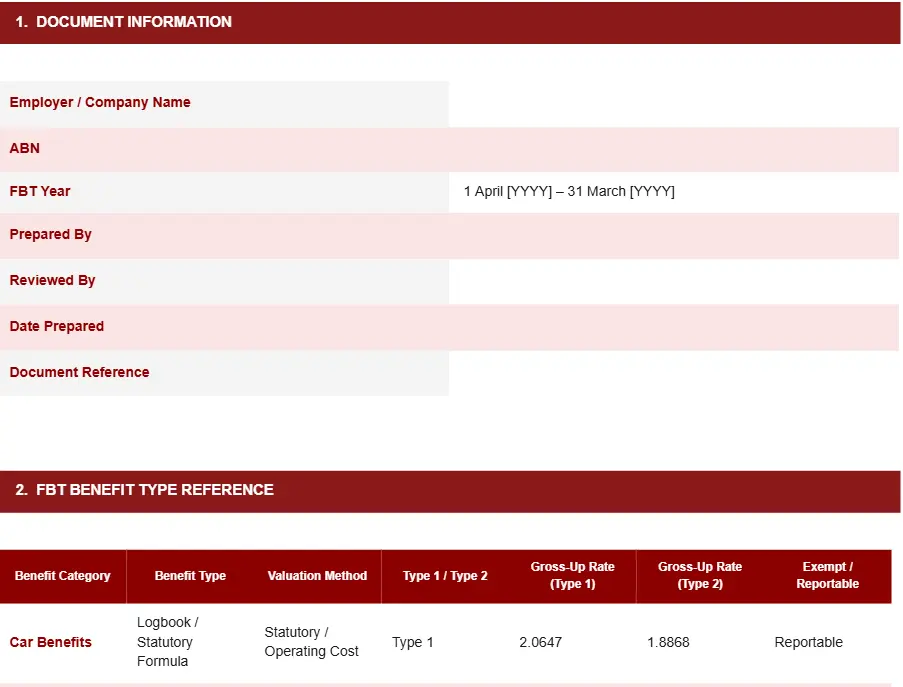

FBT calculation worksheet template

Used to calculate taxable value, apply gross-up rates, and determine total FBT payable based on benefit classification.

FBT CALCULATION WORKSHEET TEMPLATE

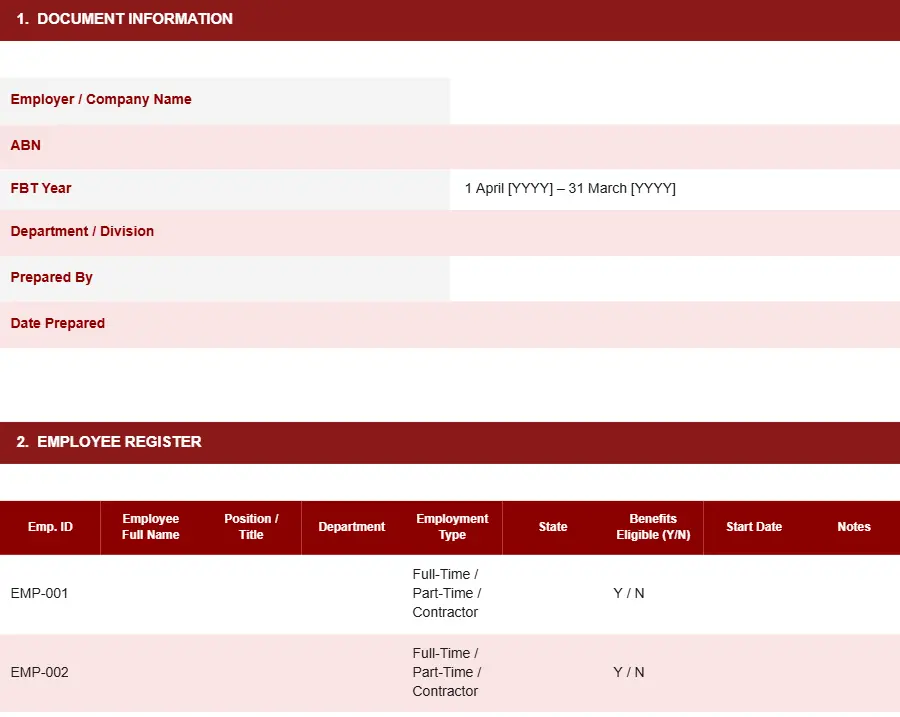

Employee benefit tracking template

Tracks all fringe benefits provided to employees, including categories, recipients, and usage throughout the FBT year.

EMPLOYEE BENEFIT TRACKING TEMPLATE

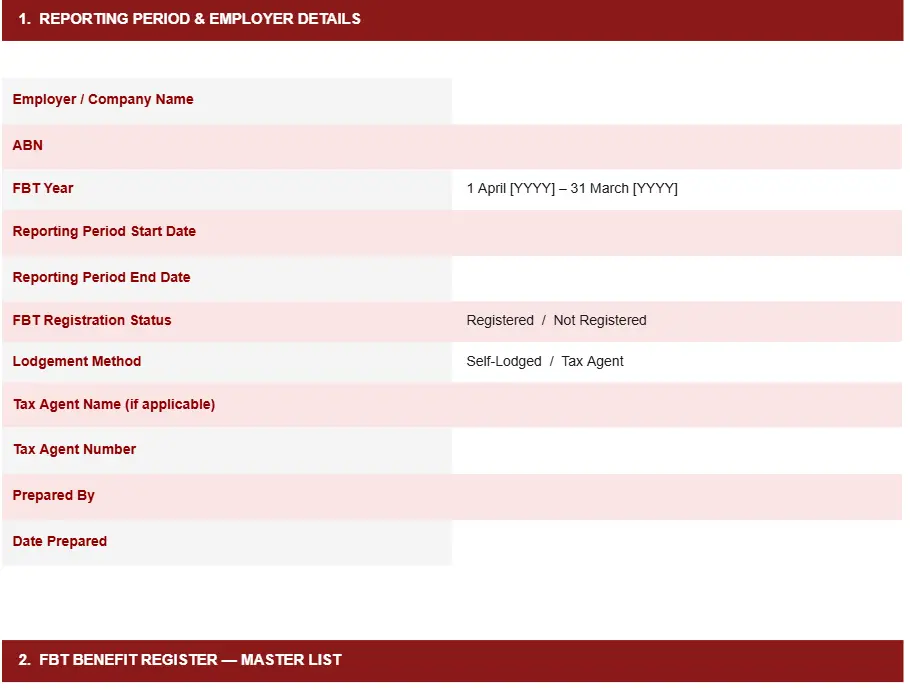

FBT register and reporting template

Organises benefit records into a structured format to support FBT return preparation and ensure consistent reporting.

FBT REGISTER AND REPORTING TEMPLATE

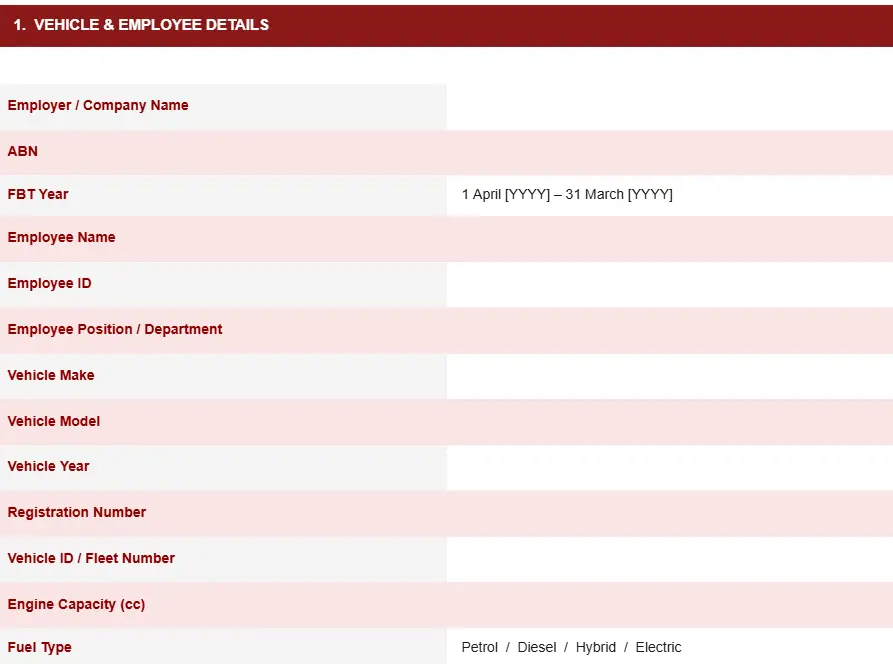

Car fringe benefits logbook template

Used to record business and private usage of company vehicles to support accurate FBT calculation for car benefits.

CAR FRINGE BENEFITS LOGBOOK TEMPLATE

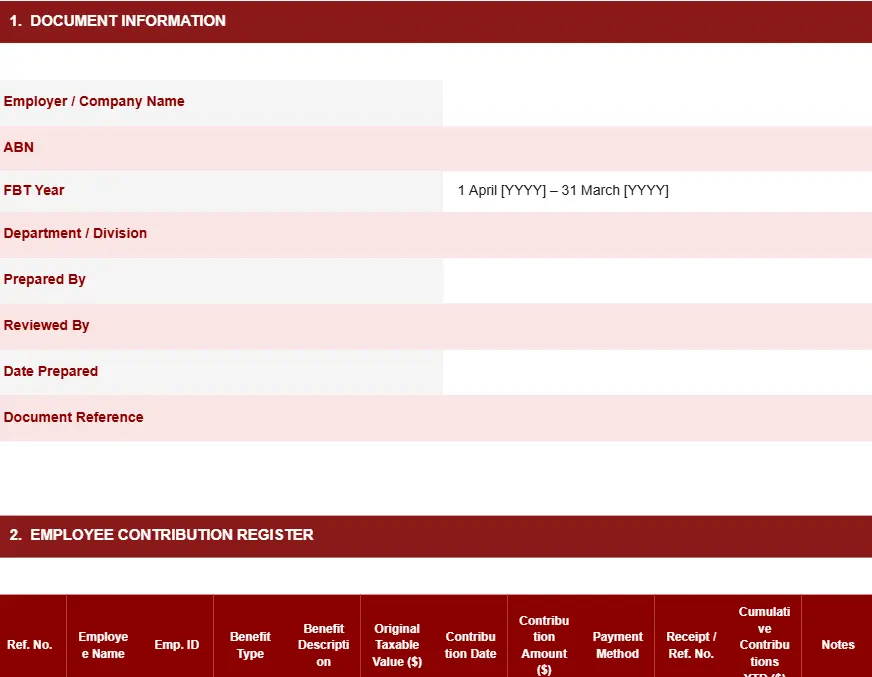

Employee contribution and adjustment template

Captures employee contributions that may reduce taxable value and affect final FBT payable.

EMPLOYEE CONTRIBUTION AND ADJUSTMENT TEMPLATE

FBT return summary template

Summarises total taxable value, adjustments, and final FBT liability for lodgement and internal review.

FBT RETURN SUMMARY TEMPLATE

Best Practices for Managing FBT Complance

Beyond using templates, maintaining strong FBT compliance requires consistent processes and regular review. These practices help ensure accuracy and reduce the risk of errors.

Maintain accurate records

Detailed records of all benefits, including values and recipients, are essential for compliance. ATO-ready accounting software captures these details automatically, so calculations stay based on complete and reliable data.

Review FBT treatment before year-end

Assessing benefits before the end of the FBT year allows time to correct errors and apply any relevant exemptions. This helps avoid rushed adjustments during reporting.

Use systems for automation

Compliant accounting tools can simplify tracking and calculations by reducing manual input. They improve consistency and support more efficient reporting throughout the FBT year.

Keep teams updated on regulations

FBT rules can change, so it is important to ensure that relevant teams stay informed. Regular updates help maintain compliance and reduce the risk of outdated practices.

Conclusion

Fringe Benefits Tax requires consistent tracking, accurate calculation, and proper reporting to avoid compliance risks. Without a structured approach, errors can quickly impact payroll costs and financial reporting.

To simplify FBT management and keep accuracy high, consider using a business accounting solution that automates tracking, calculation, and reporting in one workflow.

Request a free consultation to explore how your business can manage FBT more efficiently and stay aligned with ATO requirements year round.

FAQ About Fringe Benefits Tax

-

Can FBT apply even if employees do not directly receive the benefit?

Yes, FBT can still apply if the benefit is provided to an associate of the employee, such as a family member, as long as it relates to the employment arrangement.

-

Do all employee perks need to be reported under FBT?

Not all perks are taxable. Some may fall under exemptions or concessions, depending on their value, frequency, and purpose.

-

How do businesses handle benefits provided irregularly?

Irregular benefits still need to be assessed individually. Some may qualify for exemptions, but proper documentation is required to support the treatment.

-

Can FBT be reduced through salary packaging arrangements?

Yes, structured salary packaging can influence how benefits are taxed, but it must be managed carefully to ensure compliance with FBT rules.

-

What happens if FBT is calculated incorrectly?

Incorrect calculations may lead to underpayment or overpayment, which can trigger adjustments, penalties, or additional reporting requirements.