Australian payroll rules are changing, and Payday Super sits at the centre of that shift. From 1 July 2026, businesses must pay superannuation at the same time as wages, not quarterly. This reform directly affects payroll timing, cash flow planning, and compliance practices.

Payday Super requires companies to align Superannuation Guarantee payments with each payroll cycle. As a result, super moves from a deferred obligation to an immediate cost of every pay run. Therefore, payroll accuracy and funding discipline become critical.

For many businesses, this change goes beyond administration. It forces a rethink of payroll systems, internal controls, and financial forecasting. Early preparation will reduce disruption and compliance risk.

Key Takeaways

What is Payday Super? It requires businesses to pay superannuation at the same time as wages rather than quarterly.

Key updates under Payday Super include real-time payments, updated SG calculations, and stronger ATO enforcement.

Impact on employers and businesses includes cash flow pressure, higher payroll accuracy demands, and increased compliance monitoring.

How employers can prepare involves upgrading payroll systems, adjusting cash flow planning, and training payroll teams early.

What is Payday Super?

Instead of paying super quarterly, businesses must submit contributions with each payroll cycle. This applies to weekly, fortnightly, and monthly payrolls from 1 July 2026.

The quarterly model was designed for manual payroll environments. However, digital payroll systems now allow faster processing and reporting. Consequently, the government is removing the delay between wage payments and super funding.

More frequent payments improve employee retirement outcomes. Funds enter super accounts earlier, which increases the benefit of compound returns over time. For example, long-term balances grow simply because money is invested sooner.

The reform also targets unpaid super. By removing the quarterly gap, the ATO can detect non-compliance faster using Single Touch Payroll data. This makes compliance more visible and far less forgiving.

Key Updates Under Payday Super

Payday Super introduces several regulatory changes that reshape how payroll operates. These updates affect payment timing, Super Guarantee calculations, and enforcement. Understanding them helps businesses avoid costly errors.

Super paid on payday instead of quarterly

Super payments are now triggered by each payroll event. When wages are paid, the related super liability must follow within a short window. This removes the previous buffer that many companies used to manage cash flow.

Because of this change, late payments become a frequent risk rather than a quarterly issue. Businesses must treat every pay run as a compliance deadline.

Updated Super Guarantee (SG) obligations

By July 2026, the Super Guarantee rate reaches 12 percent. Payroll systems must apply this rate accurately on every pay run without manual adjustments.

At the same time, errors in Ordinary Time Earnings classification will cause immediate underpayments. There is no longer time to correct mistakes at quarter end.

Changes to SG shortfall calculations

Shortfalls will no longer be assessed quarterly. Instead, missing a single payday contribution may trigger a compliance event.

As a result, even small processing delays can create exposure. Payroll accuracy and timing now carry equal weight.

Stronger penalties for late payments

The ATO will receive near real-time visibility of super liabilities and payments. If funds do not arrive on time, penalties may apply quickly.

These consequences can include fines, director liability, and loss of tax deductibility. Repeated delays increase enforcement risk.

Voluntary disclosure options for employers

Businesses can still self-report errors. Early disclosure generally leads to reduced penalties and faster resolution.

However, the window to act is much shorter. Payroll teams must monitor payments continuously, not periodically.

ATO compliance approach during transition period

Initial enforcement is expected to focus on education and system issues. Businesses showing genuine effort may receive support rather than penalties.

That said, deliberate non-compliance will not receive leniency. Companies must aim for full compliance from day one.

How Payday Super Works

Payday Super relies on tight coordination between payroll, banking, and reporting systems. Payments and data must move quickly and accurately to meet deadlines.

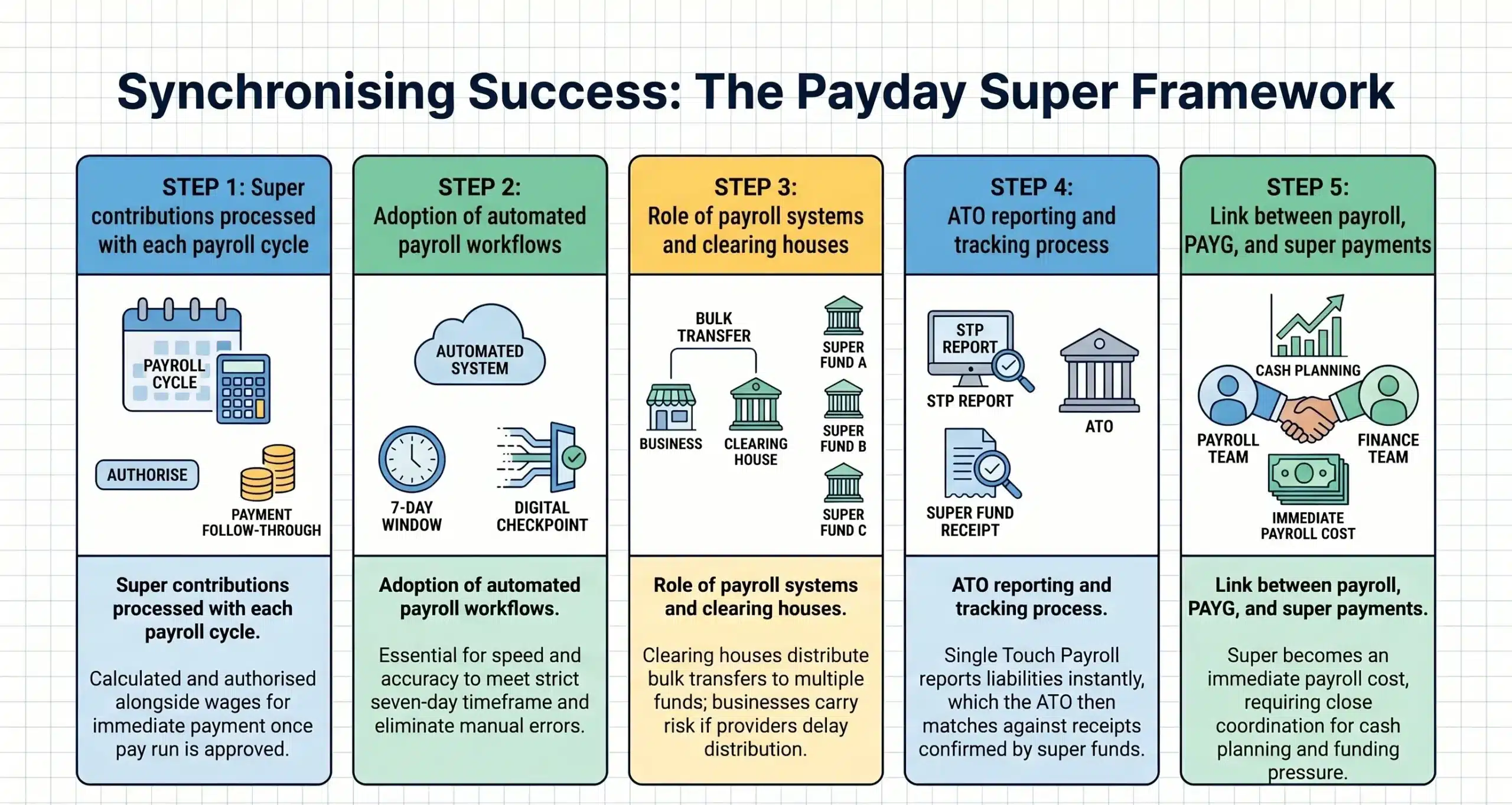

Super contributions processed with each payroll cycle

Super is calculated and authorised alongside wages. Once a pay run is approved, the super payment must follow immediately.

This process leaves little room for manual fixes. Automated payroll workflows become essential to meet the seven-day timeframe.

Role of payroll systems and clearing houses

Clearing houses distribute super payments to multiple funds from one bulk transfer. Under Payday Super, processing speed becomes critical.

If a clearing house delays distribution, the business still carries compliance risk. Therefore, system integration and provider performance matter more than before.

ATO reporting and tracking process

Single Touch Payroll reports super liabilities as soon as payroll runs. Super funds then confirm receipt through separate reporting channels.

The ATO matches these datasets. Any timing mismatch triggers alerts and potential follow-up.

Link between payroll, PAYG, and super payments

Super now forms part of the immediate payroll cost. While PAYG may follow a different schedule, funding pressure occurs at the same time.

As a result, payroll and finance teams must coordinate more closely on cash planning.

Impact on Employers and Businesses

Payday Super changes how businesses manage money, people, and compliance. The effects reach far beyond payroll processing.

Cash flow implications for businesses

Quarterly super once provided short-term liquidity. That buffer disappears under Payday Super.

Businesses must now fund super in real time. Companies with thin margins may need new financing strategies.

Changes to payroll operations and scheduling

Payroll reconciliation becomes a recurring task, not a quarterly one. Errors must be fixed immediately.

Payment timing also becomes critical. A single incorrect fund detail can delay compliance.

Administrative workload and compliance requirements

Transaction volumes increase sharply. Weekly payrolls now require dozens of super submissions each year.

This raises the need for stronger controls and more frequent checks.

Impact on small businesses vs larger organisations

Larger companies often have automated systems and dedicated payroll teams. Smaller businesses may rely on manual processes.

As a result, smaller companies face higher relative costs and operational strain.

Payroll System and Process Changes

Payday Super requires modern payroll infrastructure. Manual workarounds will no longer support compliance.

Payroll software must calculate super instantly and send compliant data without delay. Integration with financial systems helps detect errors early.

Data accuracy becomes non-negotiable. Employee fund details must be verified before the first pay run.

Failed payments also require clear workflows. Businesses need audit trails and rapid employee communication to stay compliant.

Challenges Employers Should Prepare For

Clearing house processing times create timing risk. Delays caused by weekends or public holidays can breach deadlines.

Complex payments such as bonuses and backpay add further pressure. These calculations must be correct immediately.

Employee enquiries will also increase. More frequent super payments make discrepancies more visible and more questioned.

How Employers Can Prepare

Preparation requires coordination across payroll, finance, and HR. Starting early reduces risk and avoids rushed decisions.

Reviewing payroll systems and processes

Begin with a full payroll process review. Identify manual steps and system gaps. If current software cannot support Payday Super, migration planning should start immediately.

Adjusting cash flow planning and budgeting

Quarterly super buffers must be removed from forecasts. Payroll costs now include immediate super outflows. Businesses may need revised credit arrangements to maintain stability.

Training HR and payroll teams

Teams must understand new timing rules and error risks. Regular training improves accuracy and confidence. Clear internal guidance also reduces inconsistent handling of issues.

Monitoring ATO updates and regulatory changes

Technical guidance may evolve before July 2026. Payroll leaders should track updates closely. Staying informed prevents misinterpretation and late adjustments.

Testing payroll workflows before implementation

Test runs help identify timing and data issues. Simulated pay cycles expose system weaknesses early. Fixing these problems before the deadline avoids live compliance failures.

Compliance Timeline and Expectations

The Payday Super requirement begins on 1 July 2026. From that date, every payroll run creates an immediate obligation to pay superannuation. Businesses must ensure contributions reach the employee’s nominated fund within the required timeframe.

During the early rollout period, the ATO is expected to take a practical approach to compliance. Initial efforts will likely focus on education, system alignment, and resolving technical issues. Businesses that show genuine intent to comply may receive guidance rather than penalties.

That said, accountability still applies from day one. Single Touch Payroll reporting gives the ATO near real-time visibility over payroll and super payments. Repeated delays or ignored issues may still trigger compliance action.

For this reason, businesses should plan to operate at full compliance from the first pay run. Treating the transition as a trial period increases financial and regulatory risk. Strong systems and clear internal controls remain essential.

Conclusion

Payday Super fundamentally changes how businesses manage payroll, cash flow, and compliance. Superannuation is no longer a deferred obligation but a real-time cost tied to every pay run. Businesses that adapt early will reduce financial strain and avoid compliance risk.

Preparing now gives companies time to stabilise systems, train teams, and adjust cash flow planning. Waiting increases exposure to penalties and operational disruption. Book a free consultation to assess your readiness and plan a smooth transition.

Frequently Asked Question

Payday Super requires businesses to pay superannuation at the same time as wages rather than quarterly.

The requirement begins on 1 July 2026 and applies to all payrolls from that date.

Yes. Payday Super applies to all businesses regardless of size or industry.

Super must reach the employee’s nominated fund within the required timeframe, currently proposed as seven days.

Late payments may result in penalties, loss of tax deductions, and increased ATO enforcement.