In modern business, data drives decisions, but raw numbers alone are not enough. Companies generate large volumes of transactions every day, and without a clear framework to interpret them, it becomes difficult to understand the organisation’s real financial position. Proper financial reporting provides the structure needed to make sense of this data.

Financial reporting acts as the main communication link between a company and its stakeholders, including management, investors, and regulators. It goes beyond compliance by translating daily operations into measurable financial results that can be analysed and compared.

Through standardised reports, businesses can track performance across periods and industries, helping investors make informed decisions. Managers also use these insights to guide strategy, control costs, and drive sustainable profitability for the company.

Key Takeaways

Financial reporting is the systematic process of documenting and communicating a company's financial activities to stakeholders for transparency and decision-making.

The four core types include the Balance Sheet, Income Statement, Cash Flow Statement, and Statement of Shareholder Equity, each serving a unique analytical purpose.

Accurate financial reporting in Australia ensures compliance, transparency, and proper record-keeping for all companies under AASB standards.

Implementing automation, ensuring data integrity, and shortening reporting cycles are essential best practices for modern financial management.

What is Financial Reporting?

Financial reporting is the structured process of recording, summarising, and presenting a company’s financial data to show its performance and position. It includes reports shared with investors, creditors, regulators, and the public. While closely related to accounting, reporting is the final output that turns daily transactions into a clear financial summary.

At its core, financial reporting promotes transparency. In a market shaped by volatility and scrutiny, clear and timely information builds trust. It goes beyond standard statements to include footnotes, management discussion and analysis, and supporting schedules that explain the numbers.

Financial reporting serves both external and internal audiences. External reports must follow standards such as AASB or IFRS to ensure consistency and comparability between companies. Internal reports are more flexible and focus on operational details like segment performance and budget variances.

Technology has expanded the role of financial reporting. What was once mainly historical now includes real time data and forward looking forecasts. With modern accounting software for business, finance teams can automate data collection and reporting, allowing them to play a more strategic role in guiding future decisions.

The Purpose of Financial Reporting

Types of Financial Reporting

Balance Sheet

The Balance Sheet, or Statement of Financial Position, shows a company’s financial position at a specific date. Unlike period based reports, it presents a snapshot as of the final day of the reporting cycle. It follows the core accounting equation: Assets equal Liabilities plus Equity. The statement must always remain balanced.

Assets represent resources the company owns or controls that are expected to generate future economic benefits. Current assets, such as cash, inventory, and receivables, are typically converted into cash within a year. Non current assets, including property, plant, equipment, and intangible assets, support long term operations. Reviewing asset composition helps assess liquidity and investment focus.

Liabilities and equity show how those assets are financed. Liabilities include obligations to suppliers, lenders, and other creditors, divided into short term and long term categories. Equity reflects the owners’ residual interest after liabilities are deducted. The relationship between liabilities and equity provides insight into leverage and overall financial stability.

Income Statement

The Income Statement, also known as the Profit and Loss statement, measures financial performance over a set period. It summarises revenue, costs, and expenses to show whether the company generated a profit or loss. The top line shows total revenue, while the bottom line reflects net income. Between them is a breakdown of how revenue is absorbed by operating activities.

This statement helps evaluate operational efficiency. Costs are typically divided into Cost of Goods Sold, which relates directly to production, and Operating Expenses such as rent, marketing, and administrative salaries. Reviewing gross and operating margins reveals whether production costs are increasing or overheads are becoming excessive.

Investors analyse the Income Statement to track profitability trends. Strong assets mean little if revenues are declining or losses are widening. The statement also includes non operating items like interest and taxes, offering insight into financing decisions and overall financial management.

Cashflow Statement

The Cash Flow Statement tracks the actual movement of cash in and out of a business. Managing working capital effectively also requires close monitoring of accounts payable (AP) and receivables to maintain liquidity and meet short term obligations without disrupting operations.

The statement is divided into Operating, Investing, and Financing activities. Operating cash flow reflects cash generated from core business operations and signals day to day health. Investing activities show cash used for asset purchases or received from asset sales. Financing activities record cash movements related to debt and equity, including loans, share issuances, and dividend payments.

Reviewing the Cash Flow Statement helps determine whether a company is growing or under pressure. Negative cash flow from investing may indicate expansion, while weak operating cash flow funded by heavy borrowing can signal financial strain. This analysis provides a clearer picture of sustainability than profit alone.

Statement of Shareholder Equity

The Statement of Shareholder Equity shows changes in the value of shareholders’ ownership over a reporting period. It connects the Income Statement and the Balance Sheet by explaining how net income, dividends, and share issuances affect total equity. This statement highlights whether profits are reinvested or distributed to shareholders.

Key components include common stock, preferred stock, additional paid in capital, retained earnings, and treasury stock. Retained earnings represent accumulated profits kept in the business rather than paid out as dividends. Consistent growth in retained earnings often signals financial stability and internal funding capacity.

The statement also discloses share buybacks and new share issuances. Repurchased shares appear as treasury stock and reduce total equity, often increasing earnings per share. At the same time, issuing new shares can dilute ownership, making this report essential for understanding changes in shareholder value.

Benefits of Financial Reporting

Robust financial reporting delivers value beyond regulatory compliance. Accurate and timely reports help management identify operational inefficiencies, declining margins, or rising costs, allowing quicker corrective action. Clear visibility into performance supports better strategic decisions and improves overall efficiency.

It also strengthens relationships with lenders and investors. Transparent reporting reduces perceived risk, which can lead to better loan terms and improved access to capital. Reliable financial data enables lenders to assess covenant compliance and allows investors to build accurate forecasts, making the company a more attractive and credible investment.

Additionally, strong reporting supports effective tax planning and risk management. Accurate records help ensure proper tax payments while identifying legitimate deductions and credits. Poor reporting, on the other hand, increases the likelihood of audits, penalties, and reputational damage, making high quality financial systems a long term safeguard.

Financial Reporting Requirements

Best Practices for Financial Reporting

To get more value from financial reporting, companies should centralize data and reduce manual processes. Implementing integrated finance management software helps create a single source of truth, automate reconciliations, and improve overall accuracy across departments.

Automation is also important in modern reporting. Manual spreadsheets and data entry increase the risk of errors and slow down the closing process. Solutions from companies like SAP, Oracle, and HashMicro help automate journal entries, reconciliations, and consolidations. This improves accuracy, saves time, and strengthens audit trails.

Standardized reporting formats and charts of accounts are essential, especially for businesses with multiple branches. Consistent categories make consolidation easier and allow fair comparison across units. In addition, visual dashboards and clear explanations help executives quickly understand key performance indicators and trends. Presenting both numbers and context turns financial reporting into a practical decision making tool.

Industry-Specific Nuances in Financial Reporting

1. Manufacturing: Cost Accounting and Efficiency

In the manufacturing sector, financial reporting is closely linked to cost accounting. The main focus is not only revenue, but also accurate inventory valuation and cost of goods sold. Manufacturers must manage raw materials, work in process, and finished goods, each requiring careful tracking. Proper valuation ensures that profits and assets are not overstated.

Reports often highlight absorption costing and variance analysis. They break down direct materials, direct labor, and manufacturing overhead to show true production costs. Metrics such as Purchase Price Variance help identify differences between standard and actual material costs. Many companies also connect operational data like machine utilization and Overall Equipment Effectiveness to financial dashboards to measure the cost of downtime.

Inventory Turnover and Days Inventory Outstanding are also key indicators. Excess inventory ties up capital and increases storage costs. Detailed aging reports by product or SKU help identify slow moving or obsolete stock. This prevents inflated asset values and supports better working capital management.

2. Retail: Margin Analysis and Store Performance

In brick and mortar retail, financial reporting focuses on store level performance and inventory speed. A common tool is the Four Wall Analysis, which reviews revenue and direct expenses for each store without including head office costs. This helps management see which locations generate positive cash flow and which reduce profits.

Retailers closely monitor Same Store Sales to measure organic growth without the impact of new store openings. Another key metric is Gross Margin Return on Investment, which shows how effectively inventory generates profit compared to its cost. These reports help teams decide which products are not only popular but also profitable.

Seasonal patterns strongly affect retail results. To avoid misreading short term spikes or declines, companies often review performance on a trailing twelve months basis. This approach provides a more stable view of demand, cash flow, and overall business health.

3. Distribution and Logistics: Margin Per Shipment

Distributors operate on thin margins, so financial reporting focuses on efficiency and logistics control. Instead of production costs, reports highlight freight cost as a percentage of sales and overall cost to serve. Cost to serve analysis assigns warehousing, picking, packing, and shipping expenses to specific customers. This often shows that some high revenue accounts are less profitable due to complex delivery needs or frequent small orders.

Working capital management is critical in distribution. Metrics such as Days Sales Outstanding and Days Payable Outstanding are monitored closely to manage cash timing. Since distributors may pay suppliers before receiving payment from customers, cash flow reports must be forward looking. Rolling cash flow forecasts help control the cash conversion cycle and maintain liquidity for ongoing inventory purchases.

4. E-commerce: Unit Economics and Acquisition Costs

E-commerce financial reporting blends standard accounting with digital performance metrics. While general accounting rules still apply, management reporting focuses on unit economics, especially contribution margin per order. This measures revenue minus variable costs such as cost of goods sold, payment fees, packing, and shipping, giving a clear view of real profitability per transaction.

Marketing and returns are also critical in e-commerce reports. Metrics like Customer Acquisition Cost and Lifetime Value are tracked together, often through the LTV to CAC ratio to ensure marketing spend is sustainable. In addition, net sales are reported after deducting returns and allowances at a product level, helping businesses detect quality issues and protect margins.

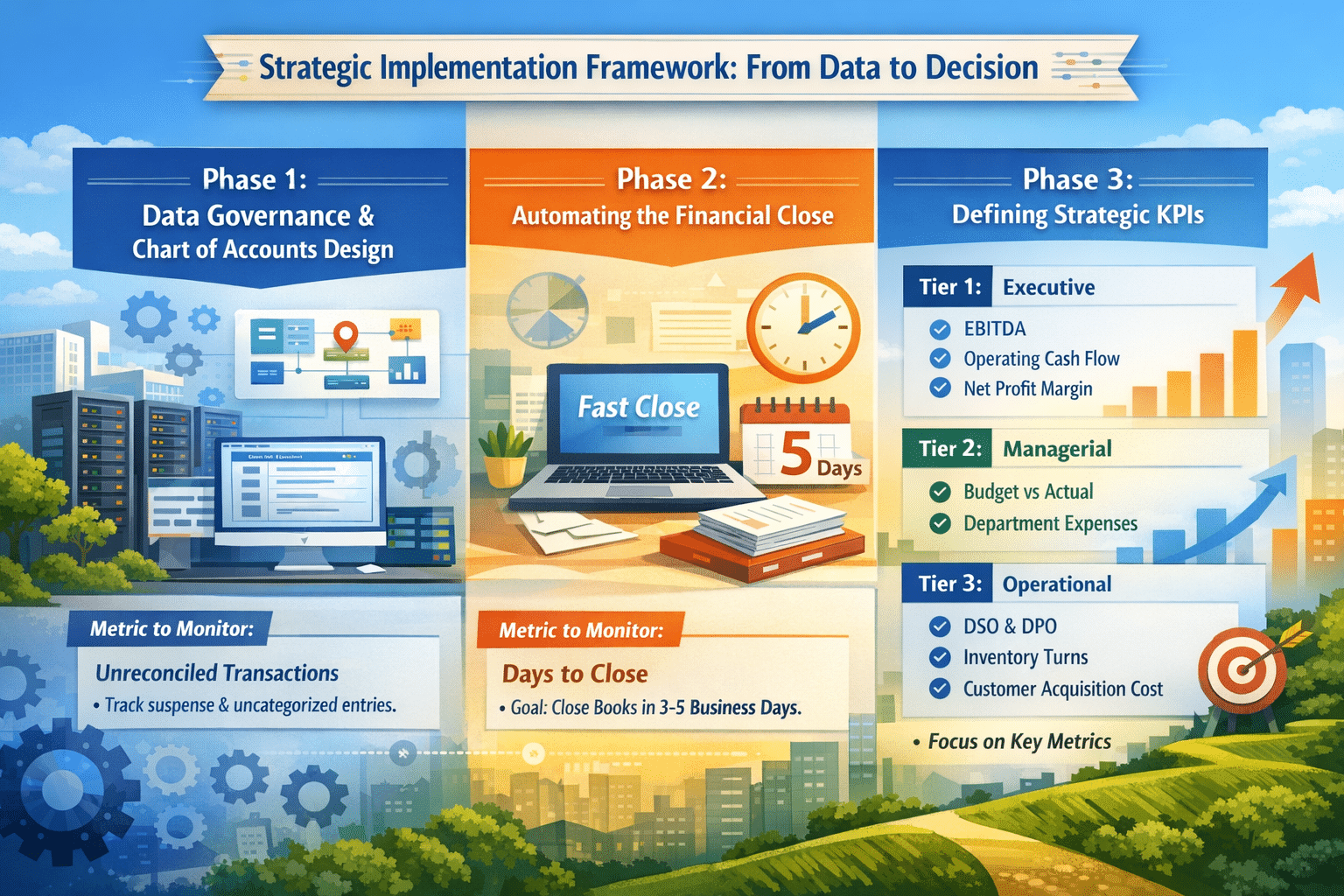

Strategic Implementation Framework: From Data to Decision

Phase 1: Data Governance and Chart of Accounts Design

Phase 2: Automating the Financial Close

Phase 3: Defining Strategic KPIs

Once data is accurate and delivered on time, the next step is choosing the right metrics. A common mistake is KPI overload, where too many indicators reduce clarity and focus. Companies should create a clear hierarchy so each level of management sees only what is relevant to their role.

- Tier 1 (Executive): EBITDA, Operating Cash Flow, Net Profit Margin.

- Tier 2 (Managerial): Budget vs Actual Variance, Departmental Operating Expenses, Headcount Ratios.

- Tier 3 (Operational): Days Sales Outstanding (DSO), Days Payable Outstanding (DPO), Inventory Turns, Customer Acquisition Cost (CAC).

Common Pitfalls and Mitigation Strategies

Even with sophisticated tools, financial reporting initiatives often fail to deliver value due to process flaws or behavioral biases. Recognizing these pitfalls early is essential for maintaining the integrity of the financial narrative.

The Trap of Historical Bias

The Pitfall: Traditional financial reporting is inherently backward-looking. It tells you what happened last month, not what will happen next month. relying solely on historical data can lead to reactive management, where decisions are made to fix past problems rather than seize future opportunities.

Mitigation: Shift from static reporting to Rolling Forecasts. Instead of holding to an annual budget that becomes obsolete by Q2, implement a 12-month rolling forecast that updates monthly based on recent actuals. This forces the organization to constantly look forward and adjust resources based on current trajectories.

Inconsistent Revenue Recognition

The Pitfall: ASC 606’s complexity makes consistent revenue recognition challenging, especially for subscriptions, bundled services, or long-term contracts. Inconsistencies can cause volatile monthly P&Ls, confusing investors and internal teams.

Mitigation: Use a centralized Revenue Recognition Engine in your ERP instead of manual spreadsheets. Automating the revenue “waterfall” ensures compliance and gives a clear view of recognized versus deferred revenue.

Data Silos and Excel Dependency

The Pitfall: “Excel Hell” happens when the true numbers live in offline spreadsheets, causing version conflicts, security risks, and formula errors. With Finance, Sales, and Operations using different sheets, trust in revenue reporting disappears.

Mitigation: Create a Single Source of Truth (SSOT). Only reports from the centralized Data Warehouse or ERP should be official. Use BI tools like Tableau, Power BI, or Looker to pull data directly, avoiding manual errors.

Conclusion

Financial reporting shows how business performance is understood and improved, requiring accuracy and consistency. Balance Sheets, Income Statements, and Cashflow Statements give stakeholders the insights they need. High-quality reporting affects reputation, capital access, and operational agility.

Companies that treat reporting as a strategic asset can build investor trust and drive sustainable growth. If you are looking to strengthen your financial systems and reporting framework, it may be time to explore your options with an expert and identify the right solution for your business.

Frequently Asked Question

Financial reporting focuses on providing standardized historical data to external stakeholders like investors and regulators for compliance. Management reporting is internal, flexible, and detailed, focusing on operational metrics to help executives make day-to-day business decisions.

The Cash Flow Statement reveals the actual liquidity of a business, stripping away non-cash accounting items like depreciation. Analysts value it because a company can show profit on the Income Statement but still fail if it lacks the cash flow to pay its immediate obligations.

GAAP is rules-based and primarily used in the US, offering specific guidance for accounting scenarios. IFRS is principles-based and used internationally, offering broader guidelines that require more interpretation, allowing for flexibility but potentially less consistency.

Automation reduces human error by eliminating manual data entry and ensures data consistency across reports. It accelerates the financial close process, allowing finance teams to focus on strategic analysis rather than data gathering.

XBRL (eXtensible Business Reporting Language) is a global standard for exchanging business information digitally. It tags financial data electronically, making it machine-readable, which allows investors and regulators to instantly analyze and compare data across different companies.