Managing inventory without real-time tracking can feel like working with incomplete information. Many businesses still rely on periodic checks to understand stock levels, costs, and overall performance. This is where the periodic inventory system offers a simple yet structured approach.

Instead of updating inventory continuously, this method focuses on scheduled counts and end-of-period calculations. While it may seem less advanced than automated systems, it remains a practical solution for many small and growing businesses. Understanding how it works can help you decide if it fits your operational needs.

What Is a Periodic Inventory System?

A periodic inventory system is a method of tracking inventory where stock levels are updated at specific intervals rather than continuously. Businesses using this system perform physical counts of inventory on a scheduled basis, such as weekly, monthly, or annually, to determine the quantity of goods on hand.

Unlike real-time tracking systems, a periodic inventory system does not automatically update inventory records after every sale or purchase. Instead, changes are recorded at the end of each accounting period. This approach is commonly used by small businesses or companies with low inventory volumes due to its simplicity and lower cost.

How a Periodic Inventory System Works

A periodic inventory system works by relying on physical stock counts and periodic updates to determine inventory levels and cost of goods sold (COGS).

At the beginning of an accounting period, businesses record their opening inventory. Throughout the period, purchases are tracked, but sales are not directly deducted from inventory records. At the end of the period, a physical count is conducted to determine the remaining inventory.

The difference between the available inventory and the ending inventory is then used to calculate COGS. This method provides a snapshot of inventory rather than continuous visibility.

Periodic Inventory vs. Perpetual Inventory

The main difference between periodic and perpetual inventory systems lies in how inventory data is updated.

A periodic system updates inventory records only at the end of a set period, while a perpetual inventory system tracks inventory in real time using software and automation.

Periodic inventory is simpler and more cost-effective but lacks real-time visibility. On the other hand, perpetual inventory provides accurate, up-to-date information but requires more advanced systems and higher implementation costs.

Businesses with high transaction volumes or complex operations typically prefer perpetual systems, while smaller businesses may find periodic systems sufficient.

Types of Periodic Inventory Valuation Methods

Businesses using a periodic inventory system must choose a valuation method to determine the cost of inventory and cost of goods sold. Understanding these options helps businesses select the most suitable approach for their operations.

1. First In, First Out (FIFO)

FIFO assumes that the oldest inventory items are sold first. This method often reflects the natural flow of goods and is widely used in many industries. It typically results in lower COGS and higher profits during periods of rising prices.

2. Last In, First Out (LIFO)

LIFO assumes that the most recently purchased items are sold first. This method can lead to higher COGS and lower taxable income when prices are increasing. However, it is not permitted under some accounting standards in certain regions.

3. Weighted Average Cost

The weighted average cost method calculates the average cost of all inventory items available for sale during the period. This average cost is then applied to both COGS and ending inventory, smoothing out price fluctuations.

Key Components of a Periodic Inventory System

A periodic inventory system relies on several essential components to ensure accurate tracking and reporting. These elements work together to provide a complete picture of inventory movement and value at the end of each period.

1. Physical Stock Count

A physical stock count is essential in a periodic inventory system. It involves manually counting all inventory items at the end of a period to determine actual stock levels.

2. Cost of Goods Sold (COGS) Calculation

COGS is calculated at the end of the period using inventory and purchase data. It represents the cost of the goods that were sold during the period.

3. Opening and Closing Inventory Records

Opening inventory is the value of stock at the beginning of the period, while closing inventory is the value after the physical count. These figures are critical for accurate financial reporting.

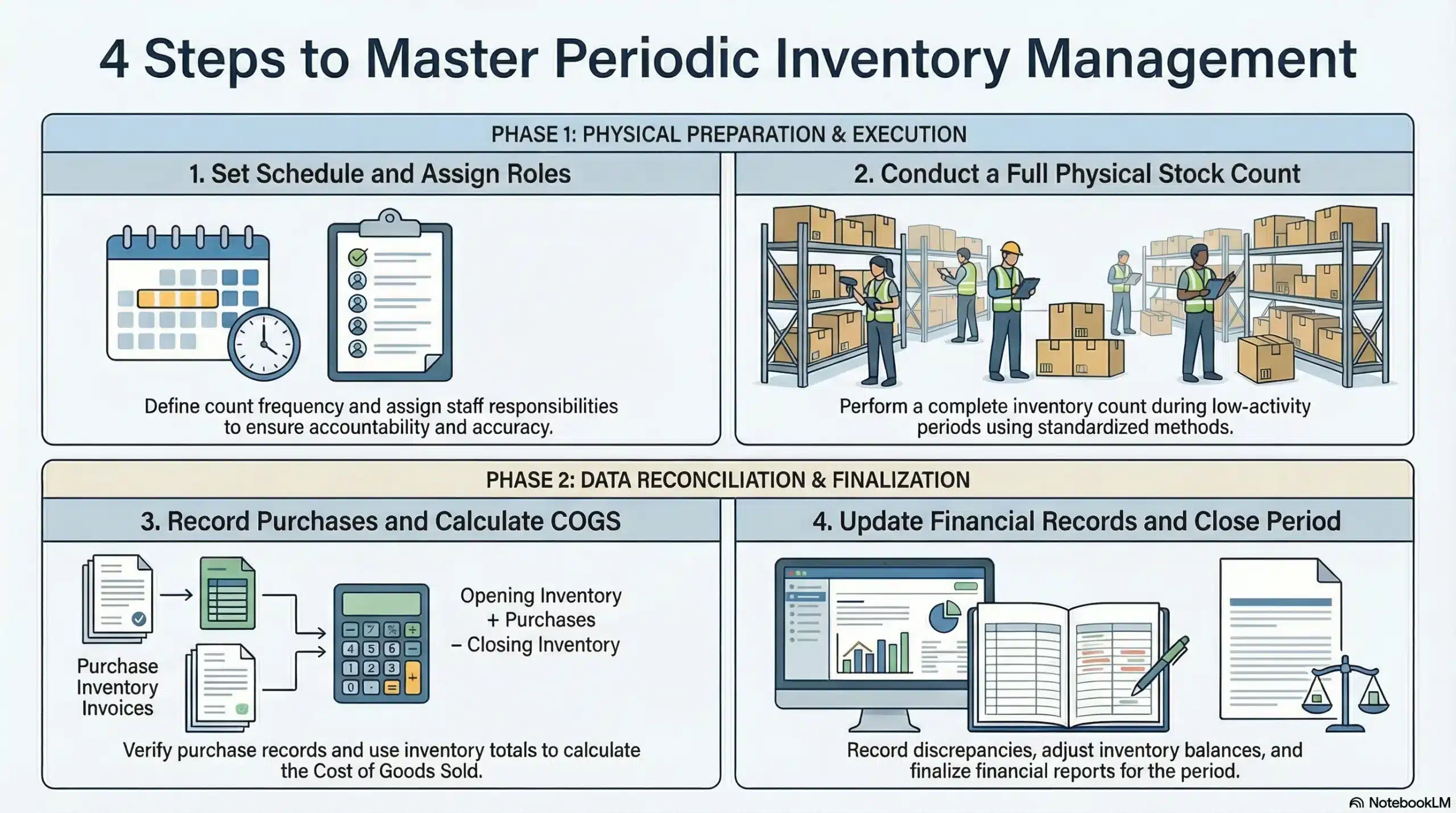

How to Run a Periodic Inventory System

Running a periodic inventory system requires a structured approach to ensure consistency and accuracy. Each step plays a critical role in maintaining reliable inventory records and financial data. Following a clear process helps minimize errors and improves overall efficiency.

Step 1 — Set a Count Schedule and Assign Responsibilities

Define how often inventory counts will be conducted based on your business needs, such as monthly or quarterly. Assign specific roles to staff, including counting and verification, to ensure accountability. A consistent schedule and clear responsibilities help maintain accuracy.

Step 2 — Conduct a Full Physical Stock Count

Perform a complete physical count of all inventory at the end of the period. Organize stock beforehand and use standardized methods to ensure accuracy. Conduct counts during low-activity periods to minimize disruptions and errors.

Step 3 — Record Purchases and Calculate COGS

Compile all purchase records for the period and verify their accuracy. Use this data along with beginning and ending inventory to calculate the cost of goods sold. This step is essential for accurate financial reporting.

Step 4 — Update Financial Records and Close the Period

Update inventory balances based on the physical count and record any discrepancies. Adjust financial records accordingly and finalize reports for the period. This ensures your accounts reflect the true value of inventory.

Periodic Inventory System Formula

The periodic inventory system uses a simple formula to calculate the cost of goods sold:

COGS = Beginning Inventory + Purchases − Ending Inventory

This formula captures the total cost of inventory available for sale and subtracts what remains at the end of the period. It provides a clear way to measure how much inventory has actually been used or sold.

For example, if a business starts with $5,000 in inventory, purchases $3,000 worth of goods, and ends with $4,000 in inventory, the COGS would be:

COGS = 5,000 + 3,000 − 4,000 = $4,000

This formula helps businesses determine how much inventory was sold during a specific period. It also plays a key role in calculating gross profit and evaluating overall business performance.

Periodic Inventory Across Industries

Different industries use periodic inventory systems depending on their operational needs.

Retail businesses with smaller product ranges often use periodic systems due to their simplicity. Manufacturing companies may use it for raw materials with less frequent turnover. Small businesses and startups also prefer periodic inventory because it requires minimal investment in technology.

However, businesses with high transaction volumes or complex supply chains typically shift to perpetual systems for better accuracy and control.

Advantages and Disadvantages of Periodic Inventory

The periodic inventory system offers several benefits. It is simple to implement, cost-effective, and does not require advanced software. This makes it ideal for small businesses or companies with limited resources.

However, it also has drawbacks. The lack of real-time data can make it difficult to track inventory accurately. Errors during physical counts can affect financial reporting, and discrepancies such as theft or damage may go unnoticed until the end of the period.

Common Periodic Inventory Mistakes to Avoid

One common mistake is conducting inventory counts too infrequently, which can lead to inaccurate records. Poor documentation during stock counts can also result in discrepancies.

Miscalculating COGS is another issue, often caused by incorrect inventory data. Additionally, ignoring differences between recorded and actual stock levels can create long-term financial inaccuracies.

Additionally, ignoring differences between recorded and actual stock levels can cause ongoing inaccuracies. Unresolved discrepancies may lead to financial losses over time. Regular reconciliation ensures inventory records remain reliable.

Best Practices for Managing Periodic Inventory

Managing a periodic inventory system effectively requires more than just counting stock at intervals. Businesses need consistent processes and disciplined execution to maintain accuracy over time.

1. Set a Consistent Count Frequency

Establish a regular schedule for inventory counts, such as weekly, monthly, or quarterly based on your business size and inventory turnover. Consistency helps maintain accurate records and makes it easier to spot discrepancies early.

2. Train Staff on Accurate Counting Procedures

Ensure employees are properly trained to count inventory and record data correctly. Provide clear guidelines on handling different types of stock, using counting tools, and documenting results. Well-trained staff can significantly reduce human errors and improve overall accuracy.

3. Reconcile Physical Counts with Purchase Records

Always compare physical inventory counts with purchase and sales records to identify discrepancies. This process helps detect issues such as missing stock, recording errors, or untracked movements. Regular reconciliation ensures your inventory data stays aligned with financial records.

4. Upgrade to an Inventory Management System When Ready

As a business grows, transitioning to a more advanced inventory management system can improve efficiency and provide real-time visibility. Automated systems reduce manual work, minimize errors, and streamline reporting.

Conclusion

The periodic inventory system offers a simple and cost-effective way for businesses to track inventory without relying on real-time technology. By using scheduled counts and straightforward calculations, it helps determine stock levels and cost of goods sold with minimal complexity.

While it may not provide continuous visibility, it remains a practical choice for small businesses or those with lower inventory volumes. With proper processes, regular counts, and accurate recordkeeping, businesses can maintain reliable inventory data and support better financial decisions.

Frequently Asked Question

A periodic inventory system is a method of tracking inventory where stock levels are updated at specific intervals through physical counts rather than in real time.

COGS is calculated using the formula: Beginning Inventory + Purchases − Ending Inventory.

A periodic system updates inventory at intervals, while a perpetual system tracks inventory continuously using real-time data and software.

It is best suited for small businesses or companies with low inventory volumes that do not require real-time tracking.

{kind=link}