Cash flow management serves as the fundamental mechanism that keeps a company operational and capable of meeting its financial obligations. Consequently, many profitable businesses face sudden bankruptcy simply because they lack the liquid assets required to pay suppliers or employees on time.

This comprehensive guide explores practical strategies to optimize liquidity and protect your business against unforeseen economic challenges. We will examine the core concepts of financial tracking and provide actionable steps to optimize receivables and payables.

Key Takeaways

Understand the fundamental mechanics of tracking money moving in and out of your business, including how operating, investing, and financing activities impact real liquidity.

Discover why cashflow management is important for Australian businesses and for survival and growth in the Australian market, where strict tax deadlines, supplier terms, and economic shifts can quickly strain working capital.

Implement actionable steps to accelerate receivables, strategically manage payables, optimize inventory turnover, control operating expenses, build reserves, and leverage forecasting tools.

What is Cash Flow Management?

Cashflow management is the systematic process of tracking, analyzing, and optimizing the amount of money circulating in a business. It involves monitoring liquidity to ensure that an organization always has sufficient funds.

This practice goes beyond basic bookkeeping to provide a real-time picture of financial health. Additionally, effective management allows leaders to predict future financial states and make informed strategic decisions.

A common misconception among new business owners is confusing cash flow with profit. Profit includes accounts receivable, which, of course, you cannot use to pay your employees with. You can only pay them with actual cash sitting in your bank account.

Why Cash Flow Management Matters for Australian Businesses

Australian businesses face strict regulatory deadlines, including GST and Superannuation obligations enforced by the Australian Taxation Office. Missing these payments due to poor liquidity management can lead to penalties and legal issues, making strong cash reserves essential.

Australia’s geographic isolation increases supply chain costs and long inventory cycles. On the other hand, many companies must pay upfront for imported goods, tying up working capital for months. Accurate financial tracking helps businesses survive these extended cash conversion periods.

The economy is also sensitive to global commodity prices and interest rate changes set by the Reserve Bank of Australia. Higher interest rates raise borrowing costs, so businesses with solid liquidity are less reliant on debt and better protected from economic shocks.

Poor cash flow remains a major cause of business failure in Australia. Even profitable companies can collapse without enough operational cash. Effective management provides early warning of shortages, giving leaders time to cut costs, boost revenue, or secure funding before problems escalate.

Types of Cash Flow in a Business

Benefits of Cash Flow Management

Effective cash flow management doesn’t just prevent financial crises; it strengthens the foundation of the business, improves control over operations, and creates needed flexibility to grow.

- Ensures Operational Stability

Effective cash flow management ensures a business can pay employees, suppliers, rent, loans, and tax obligations. Consequently, this prevents disruptions, penalties, and reputational damage while maintaining smooth daily operations and stakeholder trust.

- Improves Financial Visibility and Decision-Making

- Reduces Dependence on External Debt

Businesses with strong liquidity rely less on overdrafts, emergency loans, or high-interest financing. Maintaining positive cash flow allows companies to fund operations internally, lowering borrowing costs and reducing exposure to interest rate increases or tightening credit conditions.

- Strengthens Business Resilience

A well-managed cash position serves as protection during economic downturns, seasonal fluctuations, or unexpected expenses. Companies with healthy reserves can absorb shocks without resorting to drastic cost-cutting or asset liquidation. This resilience increases long-term survival rates.

- Supports Sustainable Growth

Consistent positive operating cash flow provides the capital needed to reinvest in marketing, technology, talent, and expansion. Growth funded by strong liquidity is controlled and strategic, rather than reckless and dependent on unstable financing.

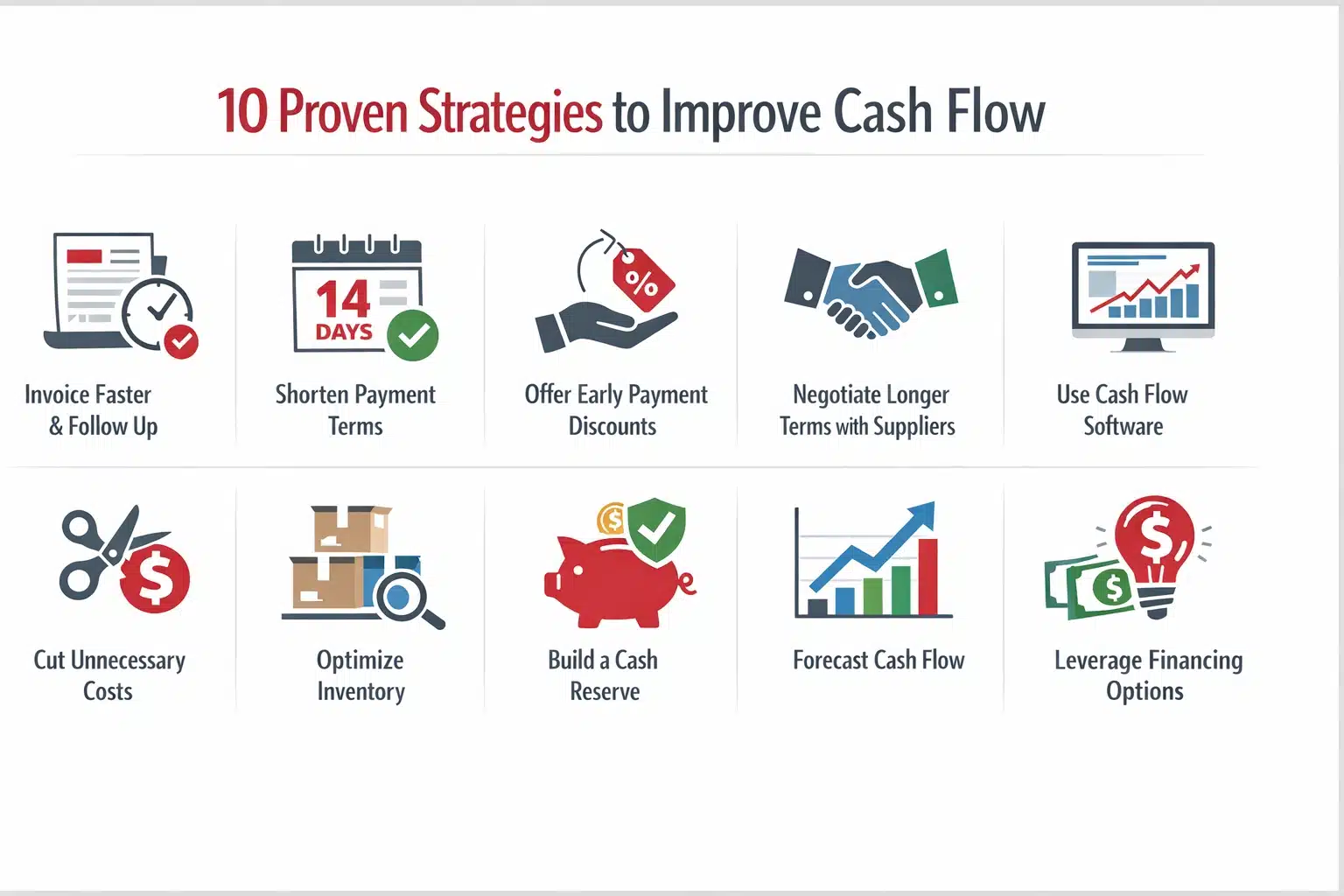

10 Proven Strategies to Improve Cash Flow

Improving liquidity requires coordinated action across all departments. The goal is to speed up cash inflows while carefully controlling outflows. A disciplined approach strengthens working capital and long-term stability.

1. Invoice Faster and Follow Up on Overdue Payments

The speed at which you issue invoices directly impacts the speed at which you get paid. Invoice payment delay artificially extends the cash conversion cycle and leaves capital trapped in the hands of customers. Invoicing should occur immediately upon the delivery of goods or the completion of a service.

Implementing a strict, immediate invoicing policy sets a professional tone and establishes clear expectations with clients. Delaying the invoice sends a subconscious message that payment is not urgent. You must train your sales and operational teams to trigger the billing process without hesitation.

Equally important is establishing a follow-up system for overdue accounts. Unpaid invoices are basically interest-free loans you provide to your clients at the expense of your liquidity. You should implement an automated reminder system that notifies customers a few days before the due date.

Professional, firm communication regarding outstanding debts commands respect and establishes boundaries. Sometimes, firing a chronically late-paying client is the best strategic decision for your overall cash flow.

2. Shorten Payment Terms

3. Offer Early Payment Discounts to Customers

Early payment discounts encourage clients to pay before the due date. A structure like “2/10 Net 30” offers a small discount for payment within 10 days instead of 30. This speeds up cash inflow while giving customers a clear incentive.

The discount must cost less than borrowing to cover shortfalls. It should be clearly displayed on invoices, showing the exact savings. Simplicity in payment processing increases participation.

It is important to monitor the usage of early payment discounts to ensure they are achieving the desired effect. Increase discounts during tight periods and scale back when cash flow is strong. This keeps the strategy flexible and controlled.

4. Negotiate Longer Payment Terms with Suppliers

While you want your customers to be the fastest, you should aim to pay your suppliers the slowest without incurring penalties. Negotiating extended payment with your vendors allows you hold cash for longer periods, which can be used to fund operations, marketing, or earn interest in a high-yield account.

All negotiated terms must be honored exactly to maintain trust. Pushing too far can damage supply reliability. You should approach negotiations strategically, perhaps offering to sign a longer-term supply contract in exchange for 45 or 60-day payment windows.

Evaluate supplier early payment discounts against your cost of capital. Sometimes paying early produces better financial returns. Each decision should be based on measurable financial benefit.

5. Advanced Software for Cash Flow Management

Manual tracking is slow and prone to error, which is why many companies adopt finance managing software for business to automate invoicing, reconciliation, and financial reporting in real time. These systems provide full visibility over cash inflows, outflows, and current liquidity at any moment.

Automation with a customizable finance solution also improves forecasting through dashboards and aging reports. Leaders gain immediate visibility into upcoming liabilities and projected inflows. Faster and more accurate information enables faster, more strategic decisions.

Granular analytics identify late-paying clients and seasonal trends. Data-driven insights allow proactive adjustments instead of reactive crisis management. Investing in financial automation technology yields a high return on investment through improved operational efficiency and tighter cash control.

6. Reduce Unnecessary Expenses and Audit Regularly

Over time, businesses tend to accumulate recurring expenses that no longer provide proportional value, draining their cash reserves. Implementing a strategy is a must to improve your financial position.

Renegotiate vendor contracts and explore cost alternatives. Convert fixed costs into variable ones when possible. Structural efficiency improves flexibility during downturns.

Avoid cutting revenue-generating investments such as effective marketing. The goal is to eliminate inefficiency, not weaken growth capacity. Smart cost control protects long-term performance.

7. Optimize Inventory to Free Up Tied-Up Capital

For product-based businesses, inventory often represents the largest drain on working capital. Excess stock locks up cash before revenue is realized. Optimizing your inventory management is essential for maintaining healthy liquidity.

Implementing a just-in-time inventory system minimizes the amount of stock held in warehouses. This approach relies on accurate demand forecasting and reliable supplier relationships to deliver goods exactly when they are needed for production or sale.. Operational coordination is critical.

You must regularly conduct inventory audits to identify slow-moving or obsolete stock. Discontinue product lines that sell very slowly, and instead, invest only in inventory that generates a rapid and reliable return. Efficient inventory turnover is a primary driver of strong operating cash flow.

8. Build a Cash Reserve

Economic downturns, sudden market shifts, and unexpected crises are inevitable realities of running a business. Maintaining three to six months of essential expenses provides financial stability and protects your company against unexpected crises, and reduces reliance on emergency borrowing.

Allocate profits consistently into a separate liquid account. Automate transfers to enforce discipline. Treat the reserve contribution as mandatory.

A strong reserve improves decision-making under pressure. Leaders avoid panic-driven choices and unfavorable agreements. Stability increases the strategic flexibility of your company in the long run.

9. Use Cash Flow Forecasting to Anticipate Shortfalls

Managing cash flow effectively is impossible if you are only looking in the rearview mirror. Historical financial statements tell you what happened, but forecasting tells you what is going to happen. It combines sales pipelines, payment patterns, payroll, and supplier obligations.

Early detection of projected deficits allows corrective action. Delaying non-essential spending or accelerating collections becomes possible. Prevention is more effective than crisis response.

Forecasting is not a set-and-forget exercise; it requires continuous updating and variance analysis, which is easier with a customizable finance solution that adapts to changing financial data. Regular reviews and comparisons with actual results improve accuracy and support disciplined financial management.

10. Leverage Financing Options Strategically

Conclusion

Cash flow management is not optional; it determines whether a business survives. Profit alone does not guarantee stability. Besides profit, liquidity, timing, and disciplined financial control define real strength.

By accelerating receivables, managing payables strategically, optimizing inventory, forecasting accurately, and using financing wisely, businesses maintain control over their financial future. Companies that master cash flow gain stability, flexibility, and long-term competitive advantage.

In the current business landscape, the use of software has become a major innovation that fuels competitive advantage for major players in the market. Hence, to help you find the best tools that can help your business in the long-term, you can request a no-cost consultation to explore the right financial tools and start upgrading your business even further.

Frequently Asked Question

Cash flow should be reviewed at least weekly, especially for small and medium-sized businesses. Companies with tight margins or rapid growth may require daily monitoring. Regular review prevents small gaps from turning into liquidity crises.

A common benchmark is a cash flow ratio (operating cash flow divided by current liabilities) above 1.0. This means the business generates enough cash from operations to cover short-term obligations. A ratio below 1.0 signals potential liquidity risk.

Yes. Rapid growth often increases expenses before revenue is collected. Businesses may need to hire staff, purchase inventory, or expand operations upfront, creating temporary cash shortages despite rising sales.